Hastings District

Council

Hastings District

Council

Civic Administration Building

Lyndon Road East, Hastings

Phone: (06) 871

5000

Fax:

(06) 871 5100

WWW.hastingsdc.govt.nz

Open

A G E N D A

Risk and Audit Subcommittee MEETING

|

Meeting Date:

|

Monday, 2

July 2018

|

|

Time:

|

10.00am

|

|

Venue:

|

Landmarks

Room

Ground Floor

Civic

Administration Building

Lyndon Road

East

Hastings

|

|

Subcommittee Members

|

Chair: Mr J

Nichols

Ex Officio: Mayor Hazlehurst

Deputy Mayor Kerr (Deputy Chair)

Councillors

Nixon and Travers

(Quorum=3)

|

|

Officer

Responsible

|

Chief Financial Officer, Bruce Allan

|

|

Committee

Secretary

|

Christine Hilton (Ext 5633)

|

Risk and Audit Subcommittee – Terms of Reference

A subcommittee of

the Finance and Monitoring Committee

Fields of

Activity

The Risk and Audit Subcommittee is responsible for

assisting Council in its general overview of financial management, risk

management and internal control systems that provide:

·

Effective management of

potential risks, opportunities and adverse effects; and

·

Reasonable assurance as to

the integrity and reliability of the financial reporting of Council; and

·

Monitoring of the Council’s

requirements under the Treasury Policy

Membership

Chairman

appointed by the Council

The Mayor

Deputy Mayor

2

Councillors

An

independent member appointed by the Council.

Quorum – 3 members

DELEGATED

POWERS

Authority to consider and make recommendations on all matters detailed

in the Fields of Activity and such other matters referred to it by the Council

or the Finance and Monitoring Committee

The

subcommittee reports to the Finance and Monitoring Committee.

HASTINGS DISTRICT COUNCIL

Risk and Audit Subcommittee MEETING

Monday, 2 July 2018

|

VENUE:

|

Landmarks Room

Ground Floor

Civic Administration Building

Lyndon Road East

Hastings

|

|

TIME:

|

10.00am

|

|

A G E N D A

|

1. Apologies

At the close of the agenda no

apologies had been received.

At the close of the agenda no

requests for leave of absence had been received.

2. Conflict

of Interest

Members need to be vigilant to

stand aside from decision-making when a conflict arises between their role as a

Member of the Council and any private or other external interest they might

have. This note is provided as a reminder to Members to scan the agenda

and assess their own private interests and identify where they may have a

pecuniary or other conflict of interest, or where there may be perceptions of

conflict of interest.

If a Member feels they do

have a conflict of interest, they should publicly declare that at the start of

the relevant item of business and withdraw from participating in the

meeting. If a Member thinks they may have a conflict of interest,

they can seek advice from the General Counsel or the Democratic Support Manager

(preferably before the meeting).

It is noted that while Members can

seek advice and discuss these matters, the final decision as to whether a

conflict exists rests with the member.

3. Confirmation

of Minutes

Minutes of the

Risk and Audit Subcommittee Meeting held Tuesday 1 May 2018.

(Previously circulated)

4. 2017/18 Annual Report Update

and Audit Plan 5

5. Enterprise Risk Management

Update June 2018 23

6. General Update Report and

Status of Actions 63

7. Additional

Business Items

8. Extraordinary

Business Items

9. Recommendation

to Exclude the Public from Items 10, 11 and 12 69

10. 2018/19 Insurance Renewal Programme

11. Internal Audit

12. IT Audit Plan & Control Review

REPORT TO: Risk

and Audit Subcommittee

MEETING DATE: Monday 2 July 2018

FROM: Chief Financial Officer

Bruce Allan

Financial Controller

Aaron

Wilson

SUBJECT: 2017/18

Annual Report Update and Audit Plan

1.0 SUMMARY

1.1 The purpose of this report is to update the Subcommittee about

progress being made on year-end issues.

1.2 The Council is

required to give effect to the purpose of local government as prescribed by

Section 10 of the Local Government Act 2002. That purpose is to meet the current and future needs of communities

for good quality local infrastructure, local public services, and performance

of regulatory functions in a way that is most cost–effective for

households and businesses. Good quality means infrastructure, services and

performance that are efficient and effective and appropriate to present and

anticipated future circumstances.

1.3 This report

concludes by recommending that the report be received

2.0 CURRENT SITUATION

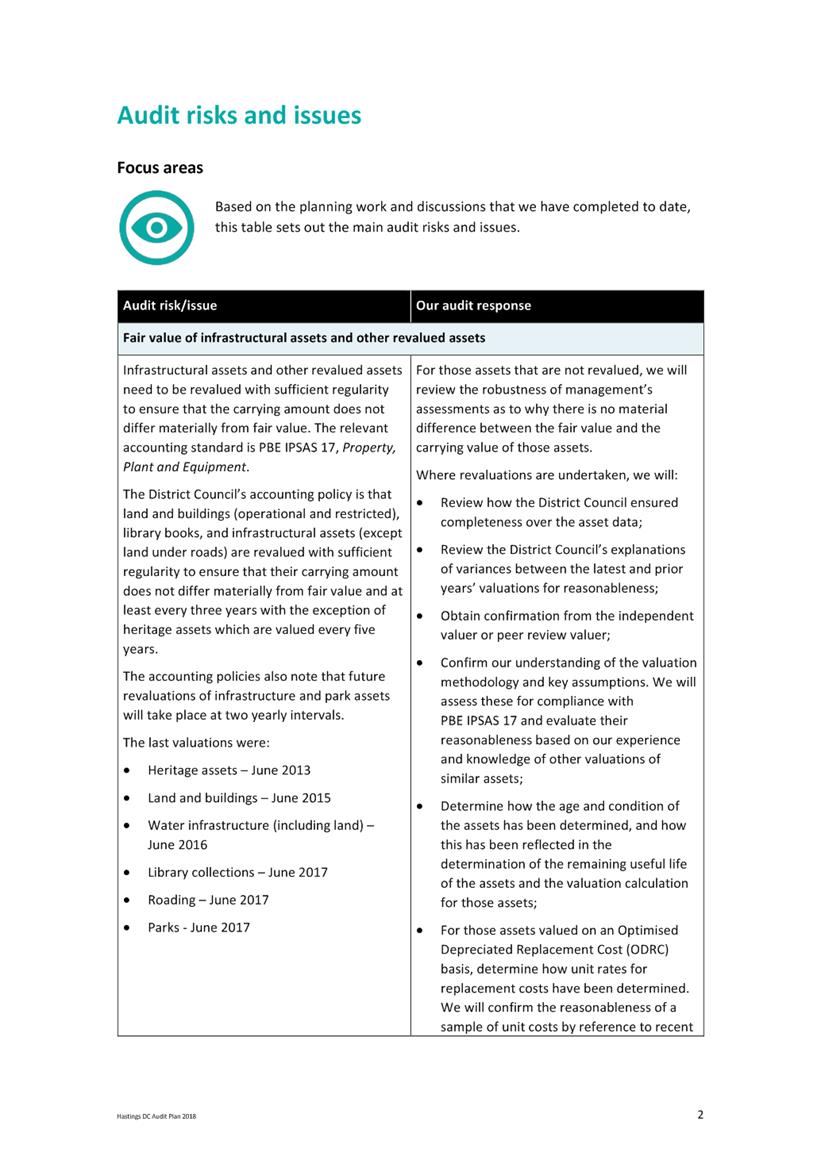

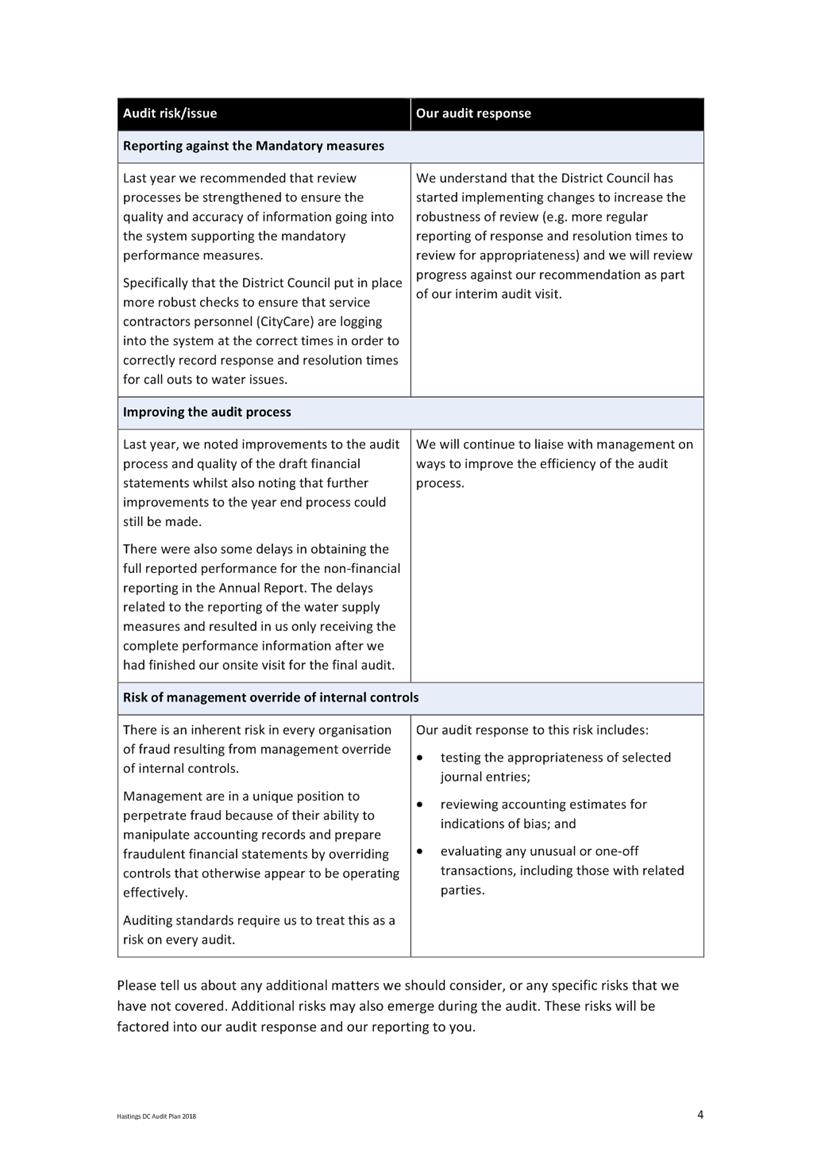

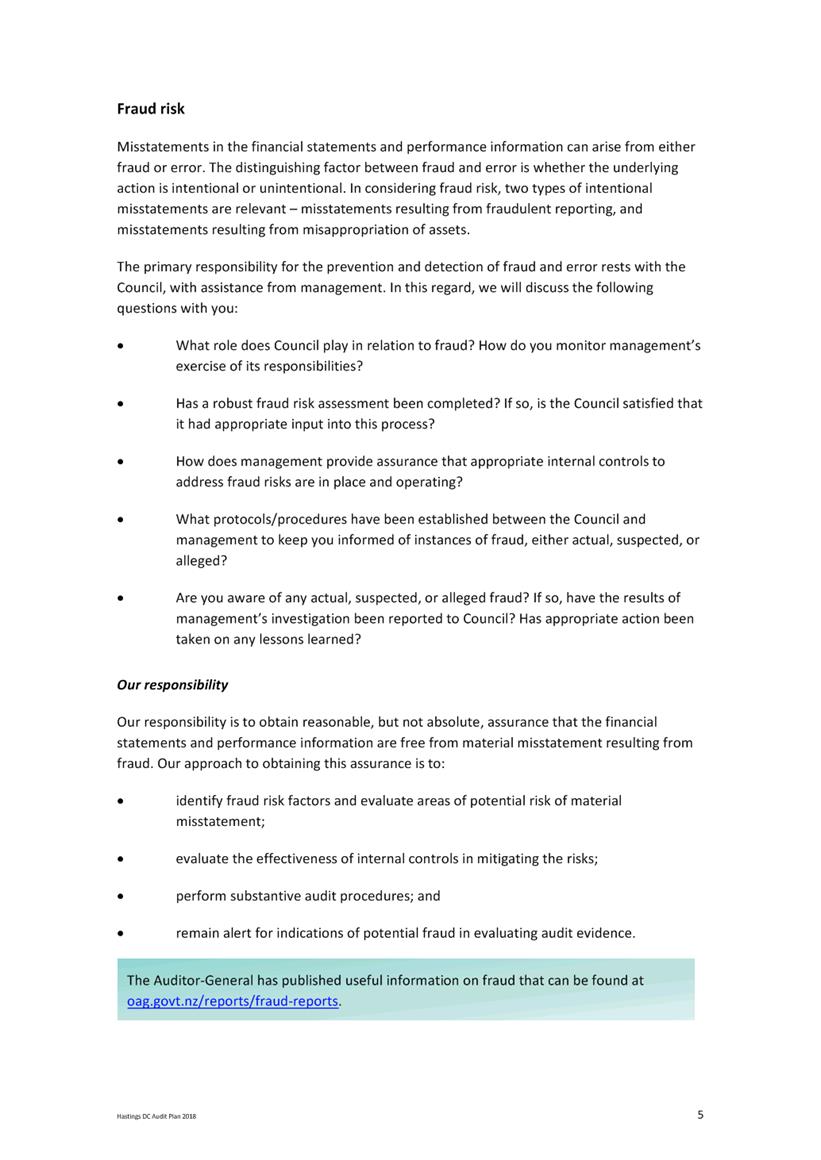

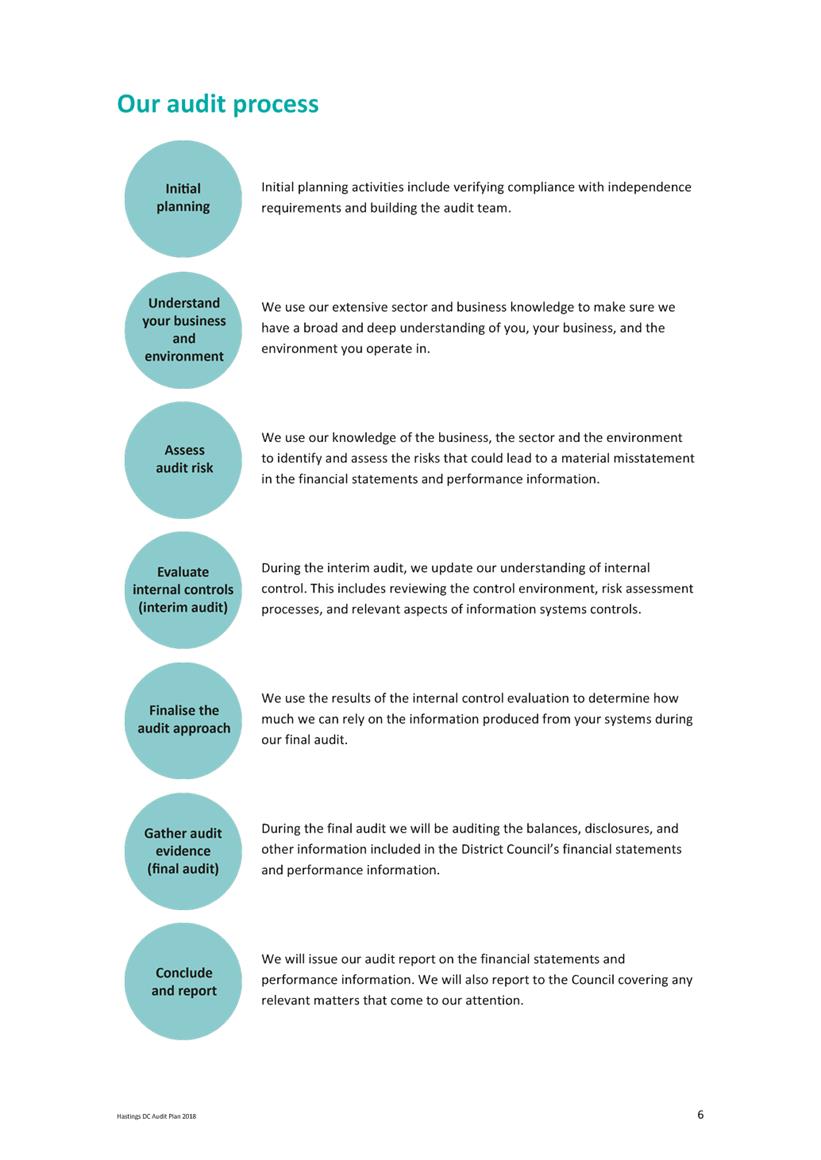

2.1 2018 Audit Plan

2.2 Audit NZ have

issued their 2018 Audit Plan and is attached as Attachment 1. The plan

sets out the arrangements for this year’s audit and includes a summary of

business risks and issues that they have identified and how they intend to

respond to these during the audit. These business issues include:

· Fair value of infrastructural assets and other revalued assets

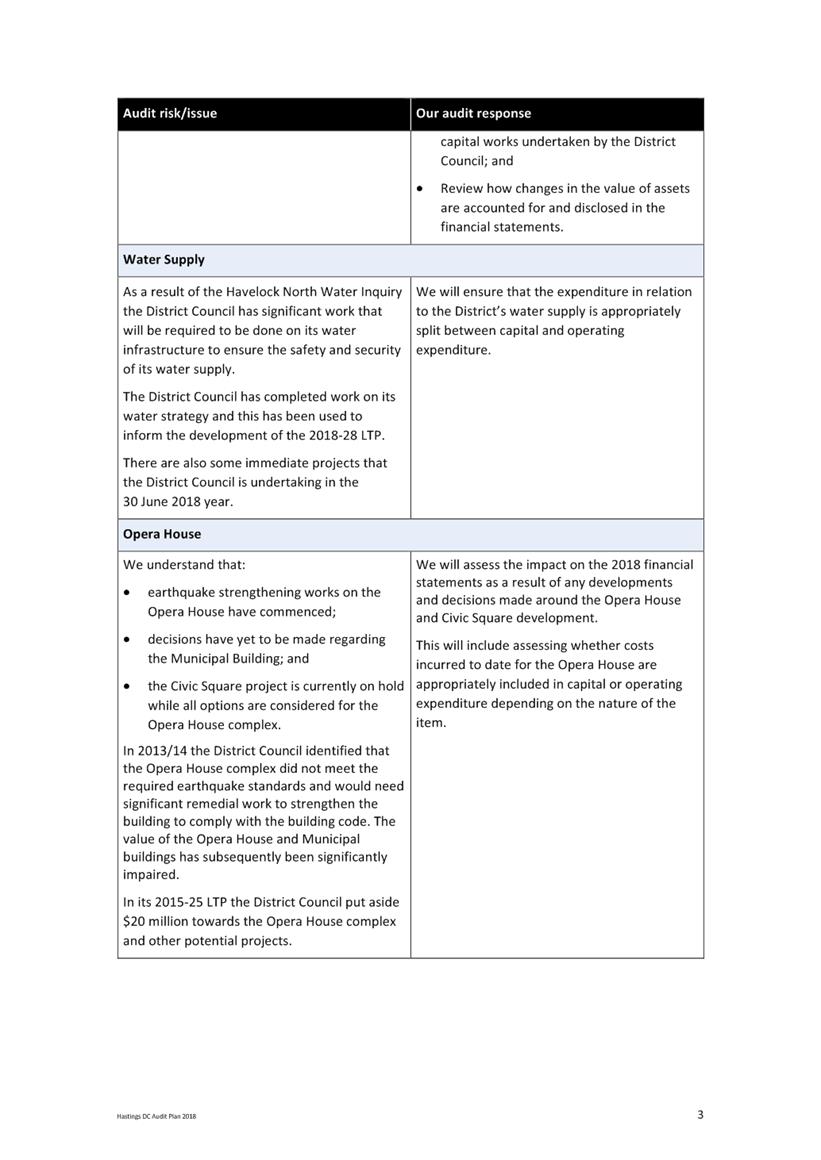

· Water Supply

· Opera House

· Reporting against mandatory measures

· Improving the Audit Process

· Risk of Management override of internal controls

2.3 Mr Stephen Lucy,

Audit New Zealand Audit Director is unable to attend this meeting.

2018 Annual Report

2.4 Staff have

completed the annual year end timetable for the 2018 year end. The timetable is

inclusive of all the processes and requirements of the production of the Annual

Report and requires a high degree of coordination across Council. The

Local Government Act stipulates that the Annual Report must be adopted by

Council by 31st October each year, this year the date set down for

Council approval is 25th October. Other key dates for the audit

process and outlined in the 2018 Audit Plan are:

Draft

financial statements available for audit 31

August

Final

Audit begins – audit on-site 3

September

Final financial statements available 21

September

Full Annual report available for Audit 1

October

Summary Annual Report available for Audit 1

October

2.5 Improvements have

been made to reporting processes and systems over the past few years and

Officers are confident of providing Audit with completed draft financial

statements for audit on August 31st prior to them arriving on-site. The

Finance team has its full complement of accounting resources this year which

should make the year end process more manageable than last year.

2.6 Every year there

are revaluations of various classes of assets that are performed on a rotating

basis on a set schedule. This year it is the Heritage and Cultural, Water

infrastructure, along with Land and Buildings assets that will be revalued. The

Land and Buildings revaluation is a significant piece of work and is well

underway with the final valuation expected from Valuation Plus by 30th June.

2.7 There are no

significant changes to Public Benefit Entity (PBE) reporting standards that are

likely to materially affect the 2017 /18 Annual Report.

2.8 At this stage of

the Annual Report process Officers are not aware of any additional issues that

may give rise to technical discussions with Audit and judgements that will be

required by Officers.

2.9 With the next

Risk & Audit Subcommittee meeting scheduled for September 4th, Officers

will be working to have some preliminary financial statements available for the

subcommittee to review. Obviously at this time anything presented will be

unaudited and subject to change.

3.0 SIGNIFICANCE AND ENGAGEMENT

3.1 The matters

within this report do not trigger the thresholds within Council’s

significance and engagement policy.

|

4.0 RECOMMENDATIONS AND REASONS

A) That the

report of the Chief Financial Officer titled “2017/18

Annual Report Update and Audit Plan” dated 2/07/2018

be received.

|

Attachments:

|

1

|

Audit Plan for the year ending 30 June 2018

|

FIN-07-01-18-401

|

|

|

Audit Plan for the year ending 30 June

2018

|

Attachment 1

|

REPORT TO: Risk

and Audit Subcommittee

MEETING DATE: Monday 2 July 2018

FROM: Risk and Corporate Services Manager

Regan Smith

District Customer Services Manager

Greg

Brittin

SUBJECT: Enterprise

Risk Management Update June 2018

1.0 SUMMARY

1.1 The purpose of

this report is to update the Subcommittee on Enterprise

Risk Management activities and to present Bow Tie analysis for the following strategic

risks; Loss of key staff, Officer error/omission, Failure to meet regulatory

requirements, Legislative change, Facility failure and Failure to achieve

business as usual performance.

1.2 This issue arises

from adoption of the Strategic Risk Register by Council.

The Council is

required to give effect to the purpose of local government as prescribed by

Section 10 of the Local Government Act 2002. That purpose is to meet the

current and future needs of communities for good quality local infrastructure,

local public services, and performance of regulatory functions in a way that is

most cost–effective for households and businesses. Good quality means

infrastructure, services and performance that are efficient and effective and

appropriate to present and anticipated future circumstances.

1.3 This report

concludes by recommending that the report be received.

2.0 BACKGROUND

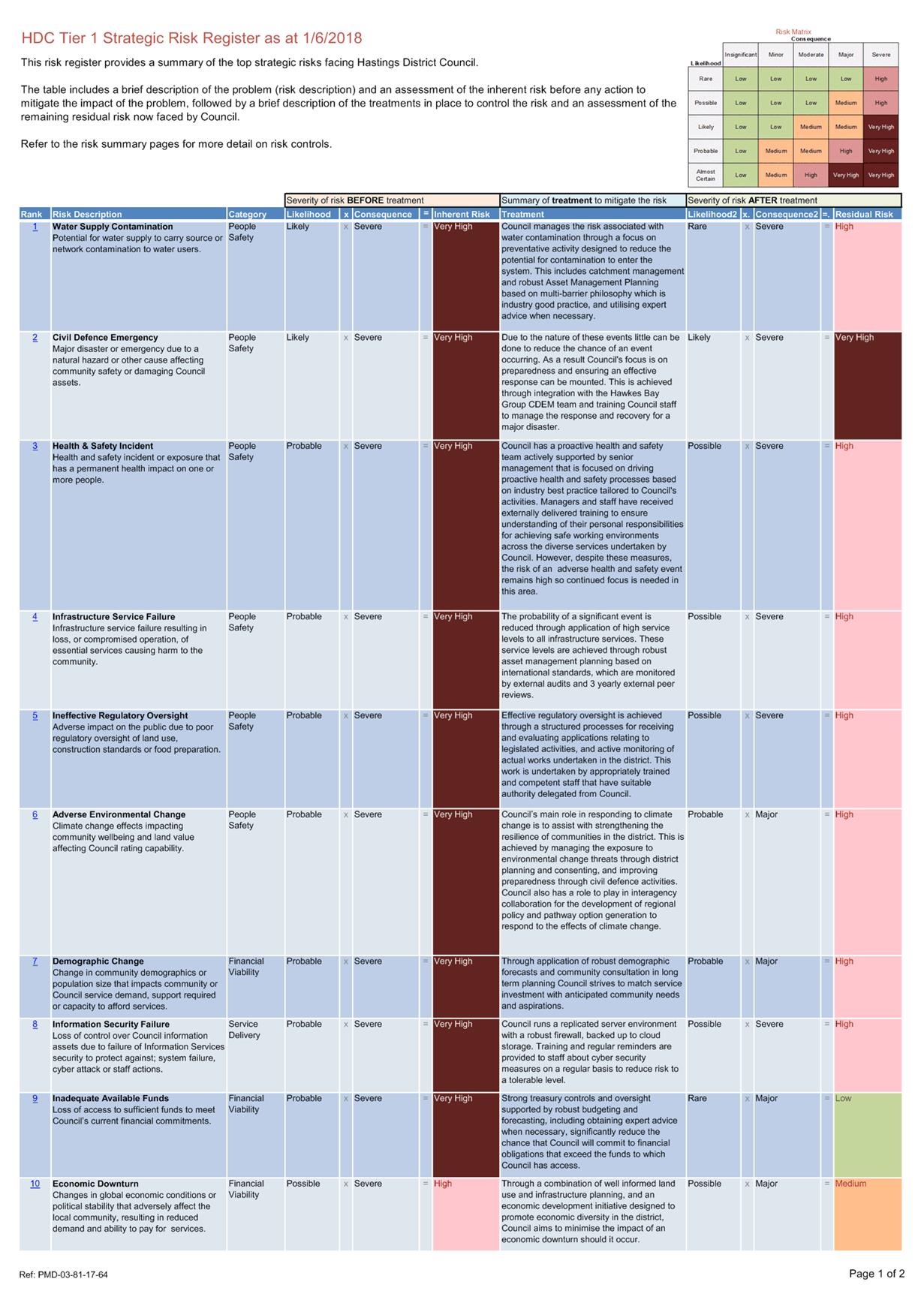

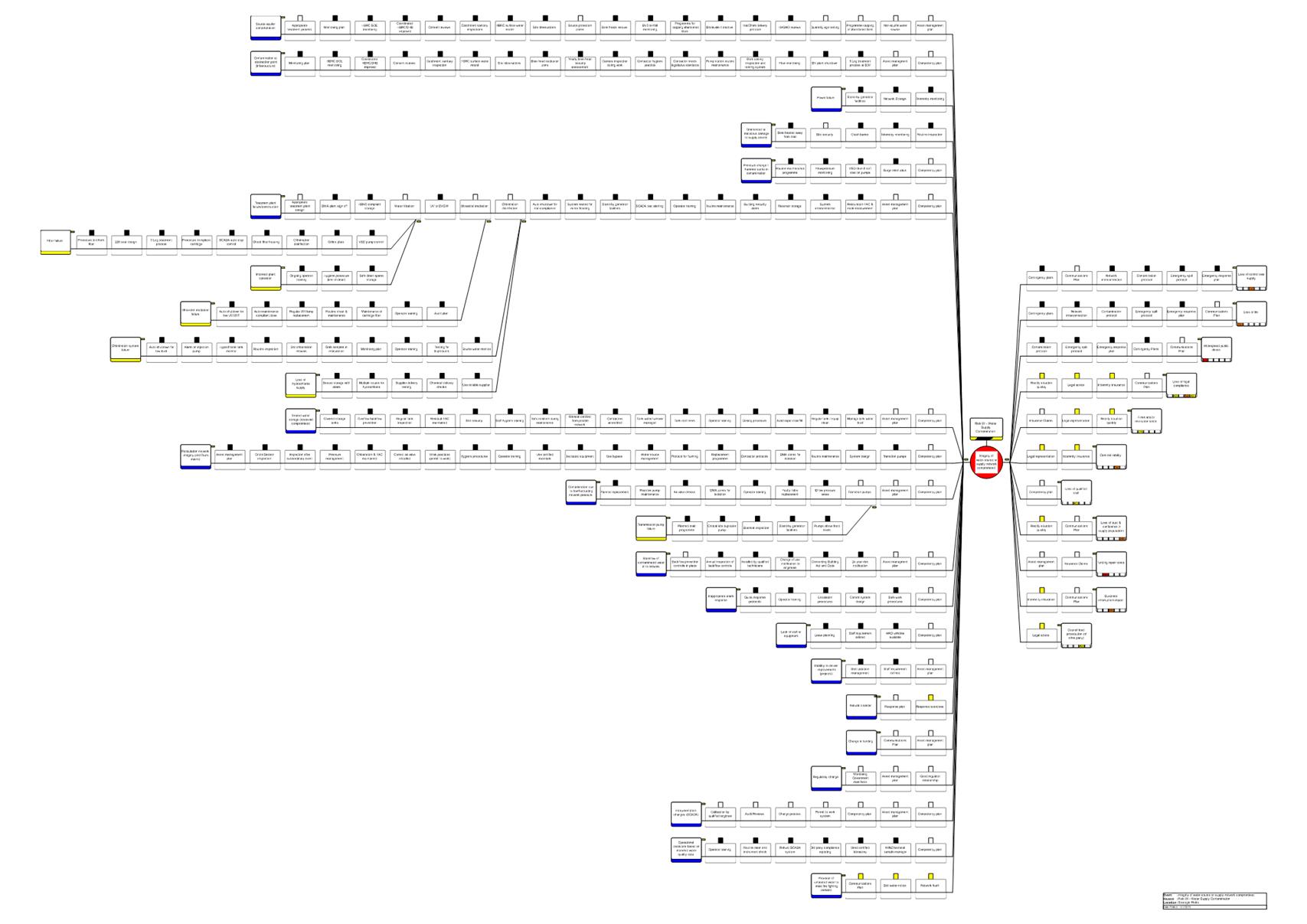

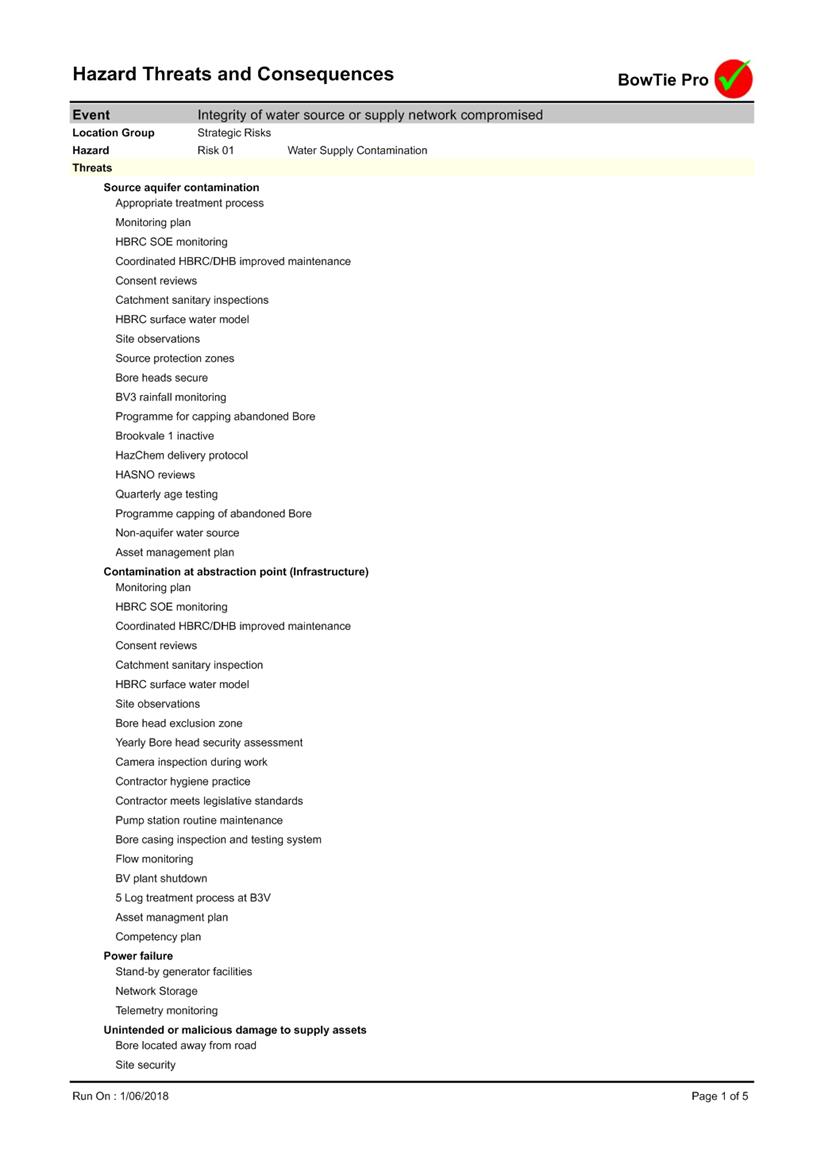

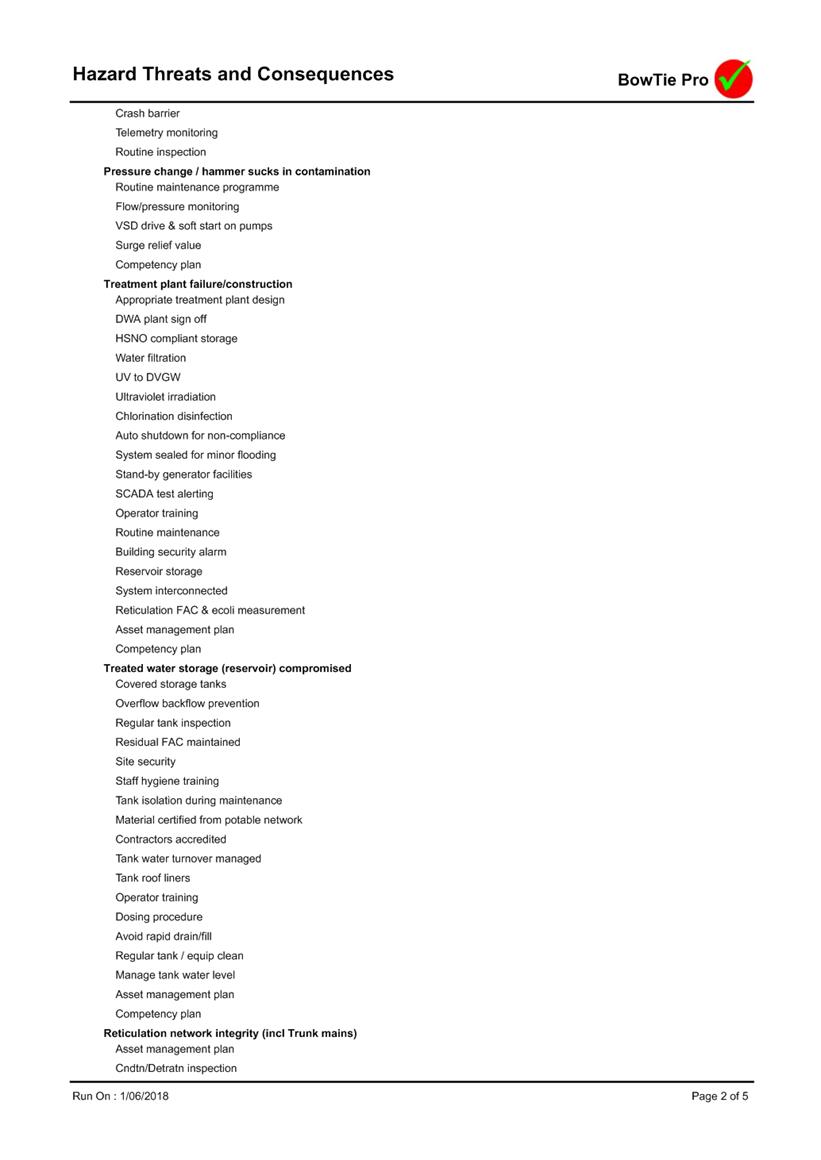

2.1 Council has adopted the Bow Tie risk assessment method to analyse the

strategic risks adopted by Council on 31 July 2017.

2.2 The Bow Tie risk assessment method was selected by Council as it is

an effective tool to demonstrate causal relationships

in complex systems. A Bowtie diagram does two things. First of all, it gives a

visual summary of all plausible accident scenarios that could exist around a

certain Hazard. Secondly, by identifying control measures the Bow Tie displays

what the organisation does to control those scenarios.

2.3 Bow Tie analysis of strategic risks and associated threats,

consequences and control barriers, have been completed and reported to the

Subcommittee for the following risks:

· Civil Defence Emergency (Risk #2).

· Health & Safety Incident (Risk #3).

· Infrastructure Service Failure (Risk #4)

· Ineffective Regulatory Oversight (Risk #5)

· Adverse Environmental Change (Risk #6)

· Demographic Change (Risk #7)

· Information Security Failure (Risk #8)

· Inadequate Available Funds (Risk #9)

· Economic Downturn (Risk #10)

· Biosecurity Failure (previously Risk #11) addressed within response

to Economic Downturn.

· Procurement Failure (Risk #12)

· Corruption and Fraud Incident (Risk #13)

· Business Interruption (Risk #14)

3.0 CURRENT SITUATION

3.1 Initial Bow Tie risk

analysis have been completed for the following strategic risks. Note; the Bow

Tie diagrams are included for reference to show the scale of work. It is not

intended that these be read as presented. The content of the analysis is

summarised in the One Page summaries.

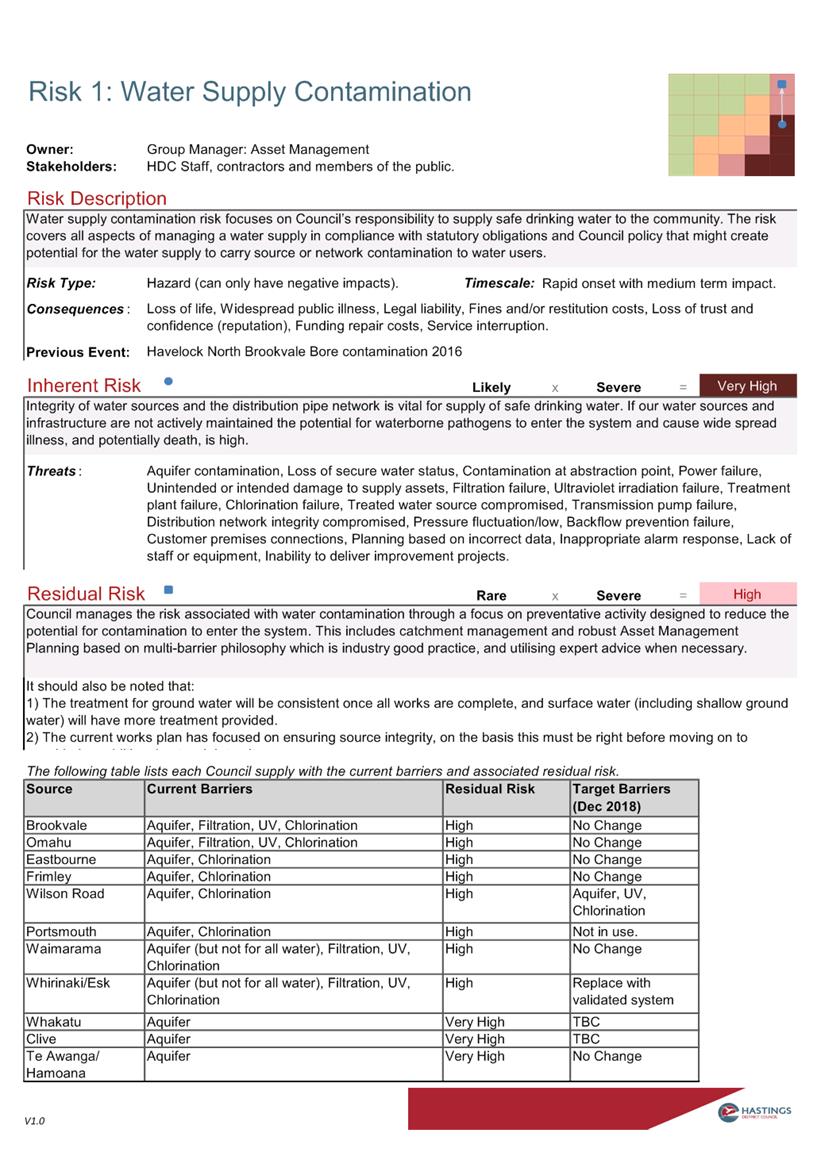

3.1.1 Water contamination

(Risk #1) – updated: Water supply contamination risk focuses on

Council’s responsibility to supply safe drinking water to the community.

The risk covers all aspects of managing a water supply in compliance with

statutory obligations and Council policy that might create potential for the

water supply to carry source or network contamination to water users.

3.1.2 Risk assessment: The

Water Contamination bow tie diagram (attached) was created from the detailed

risk registers contained in the Water Safety Plans (WSP). This bow tie

illustrates the complexity of the system and the extensive preventative

controls in place. This process has validated the integrity of the WSP risk

registers and identified potential areas for further improvement, particularly

with regard to consequence mitigation controls.

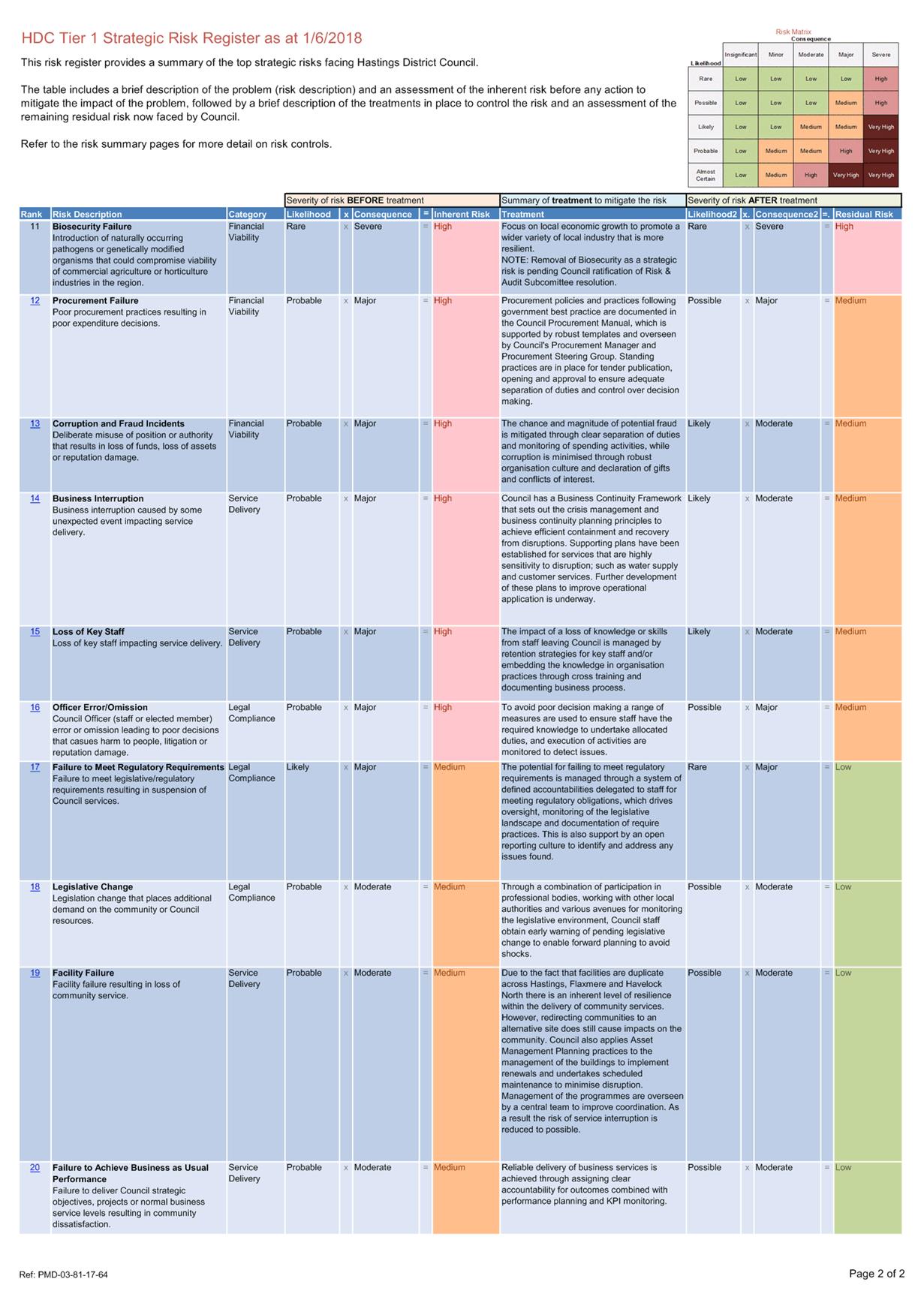

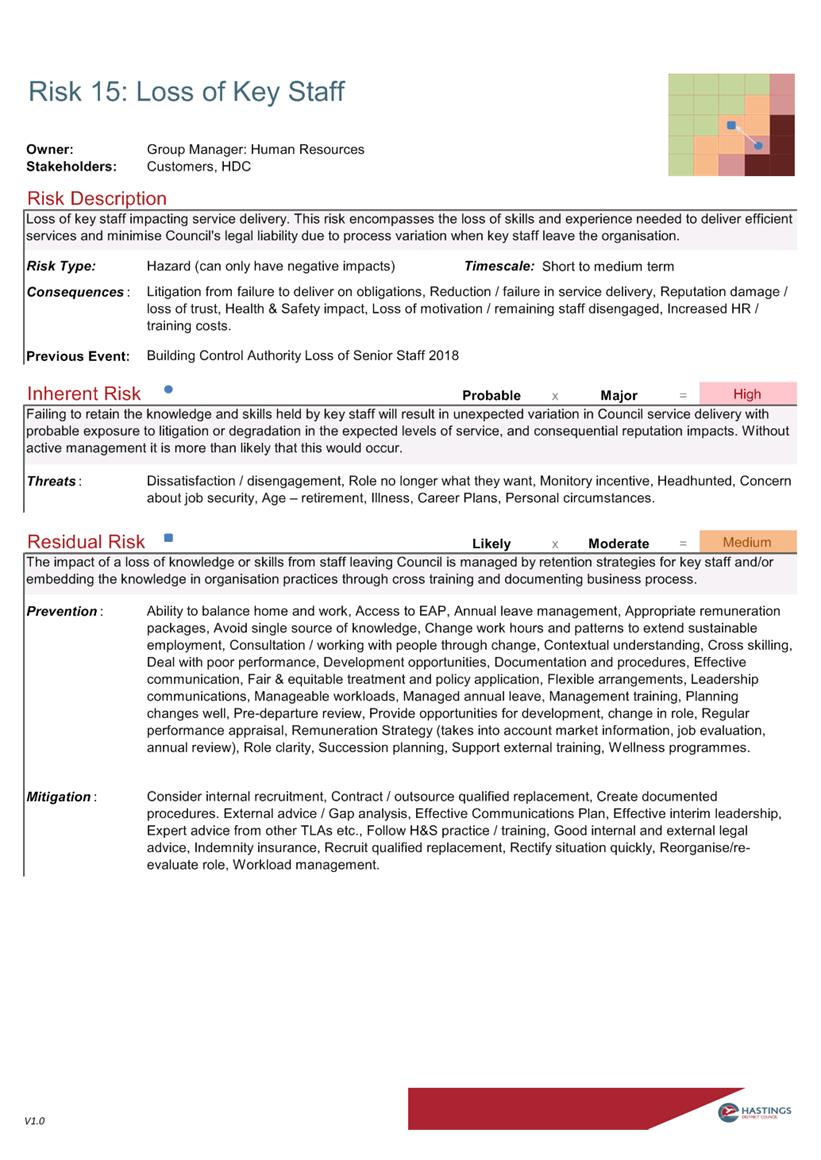

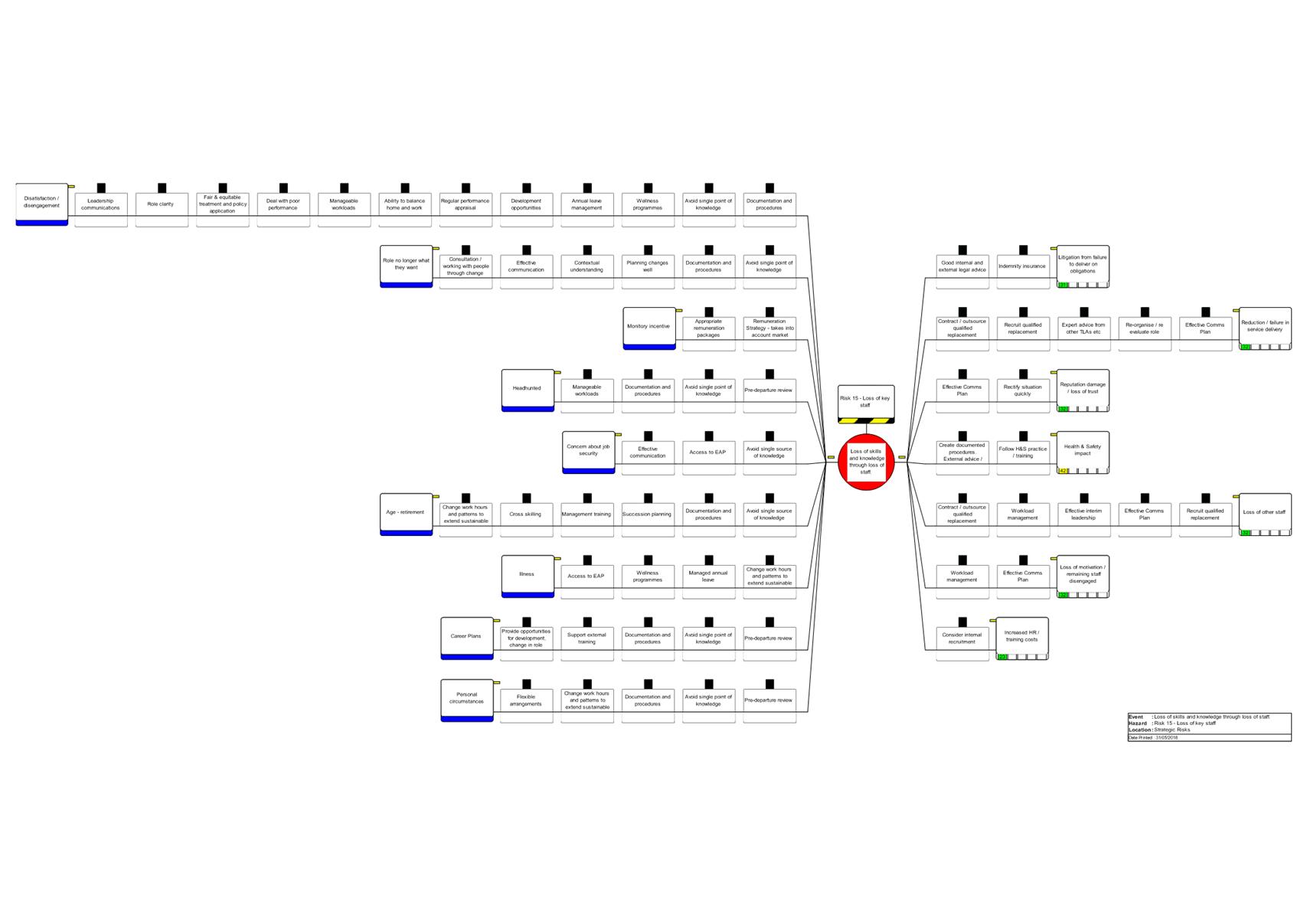

3.1.3 Loss of key staff (Risk

#15): Loss of key staff impacting service delivery. This risk encompasses

the loss of skills and experience needed to deliver efficient services and

minimise Council's legal liability due to process variation when key staff

leave the organisation.

3.1.4 Risk assessment: The

impact of a loss of knowledge or skills from staff leaving Council is managed

by retention strategies for key staff and/or embedding the knowledge in

organisation practices through cross training and documenting business process.

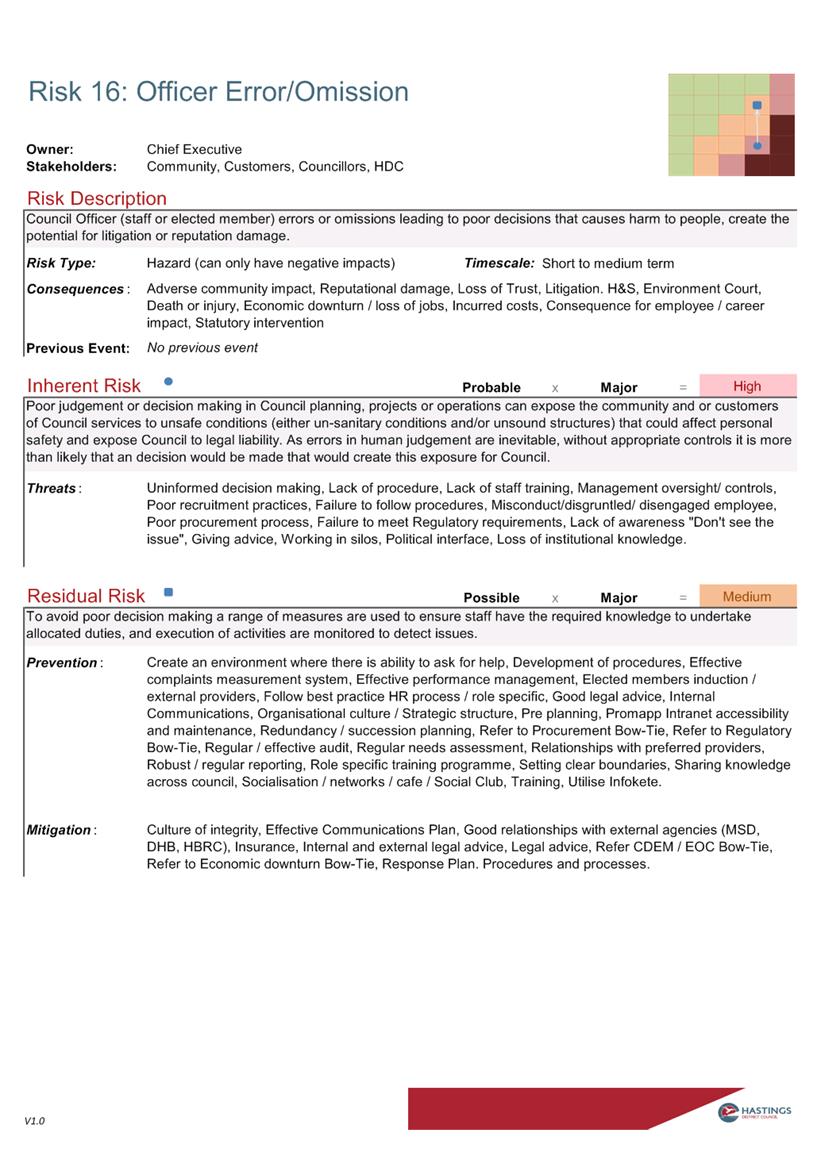

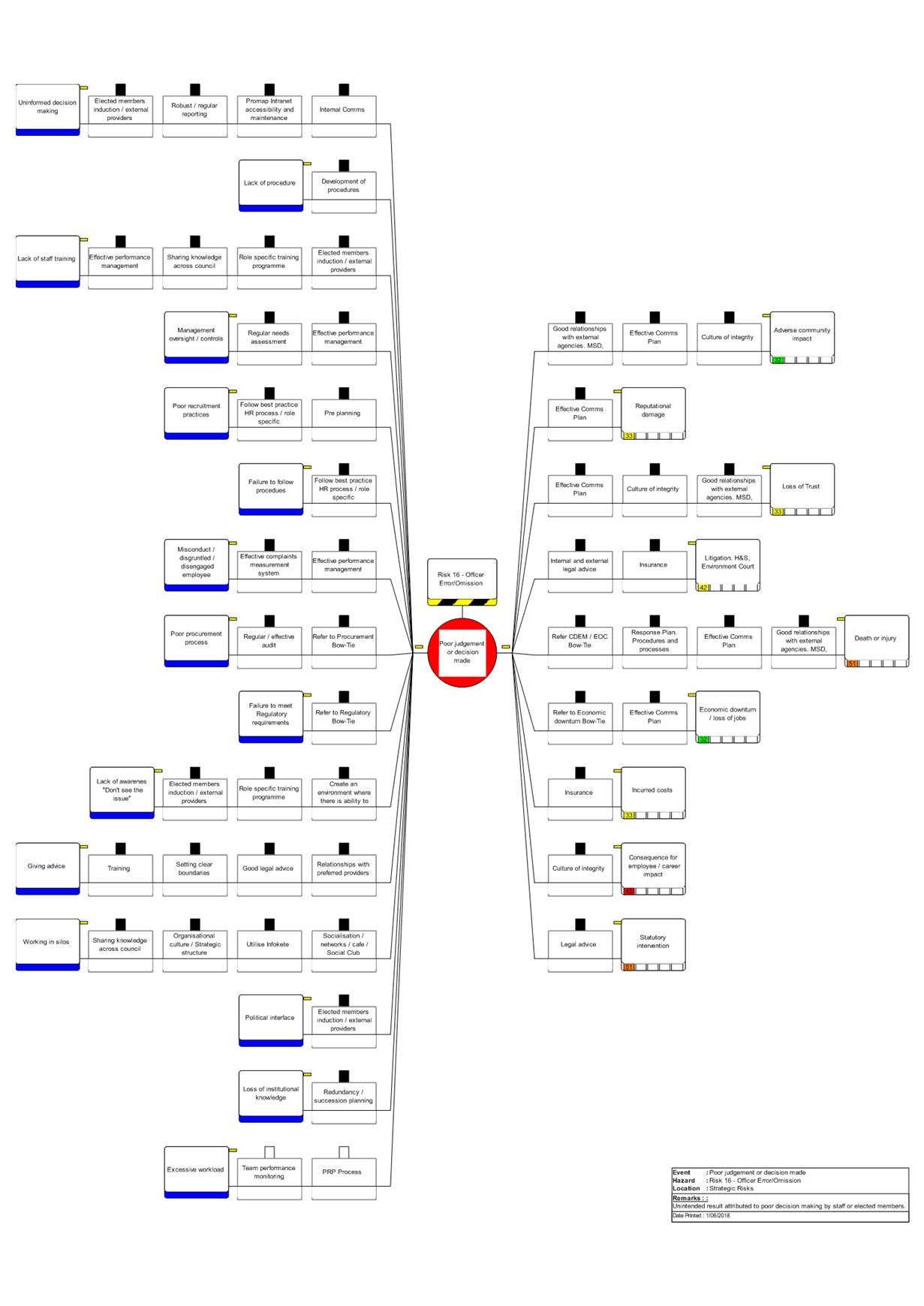

3.1.5 Officer error/omission

(Risk #16): Council Officer (staff or elected member) errors or omissions

leading to poor decisions that causes harm to people, create the potential for

litigation or reputation damage.

3.1.6 It should be noted that the

title of risk 16 was changed from Office Negligence to Officer Error/Omission

during the bow tie risk analysis workshop. This change was made as it allowed a

wider range issues to be taken in to account and avoided concerns regarding the

legal interpretation associated with the term negligence.

3.1.7 Risk assessment: To

avoid poor decision making a range of measures are used to ensure staff have

the required knowledge to undertake allocated duties, as well as monitoring the

execution of activities to detect variation.

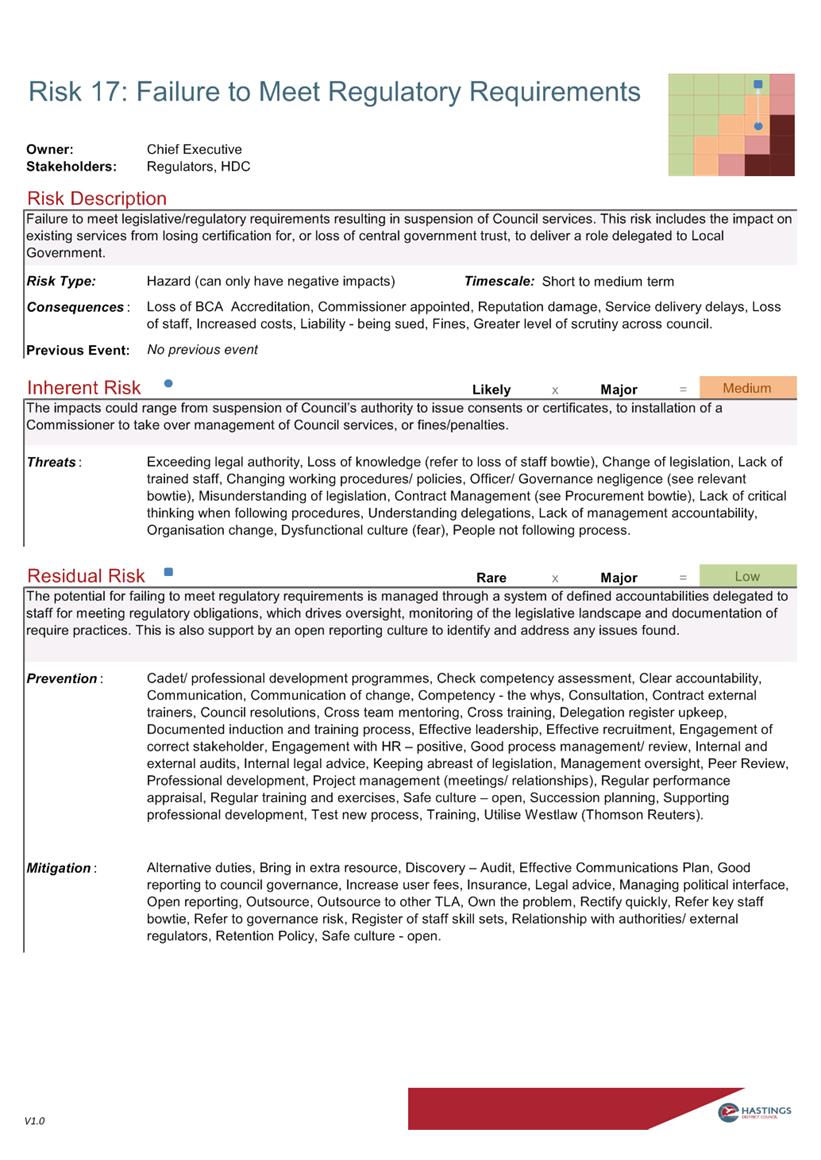

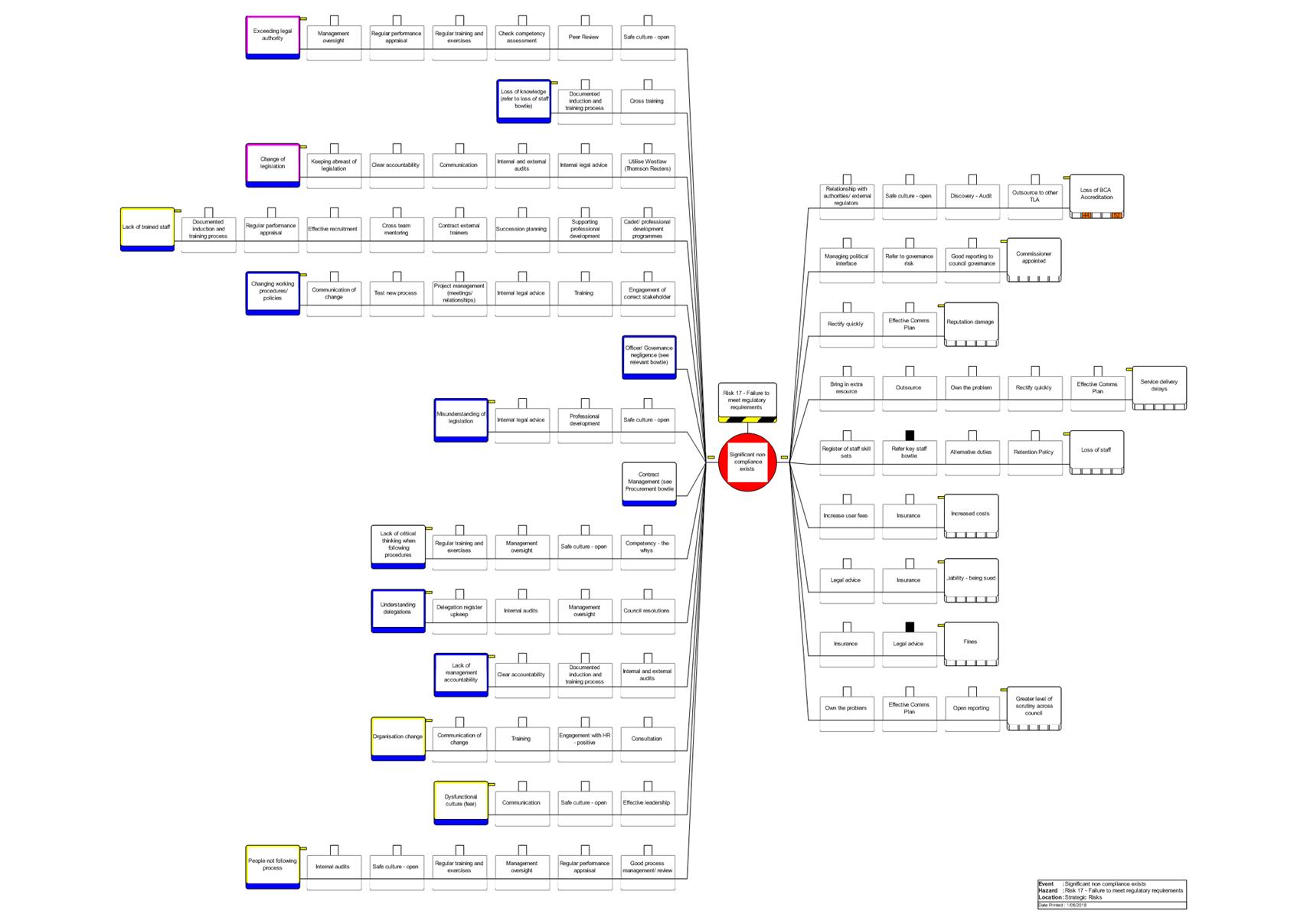

3.1.8 Failure to meet

regulatory requirements (Risk #17): Failure to meet legislative/regulatory

requirements resulting in suspension of Council services. This risk includes

the impact on existing services from losing certification for, or loss of

central government trust, to deliver a role delegated to Local Government.

3.1.9 Risk assessment: The

potential for failing to meet regulatory requirements is managed through a

system of defined accountabilities delegated to staff for meeting regulatory

obligations, which drives oversight, monitoring of the legislative landscape

and documentation of require practices. This is also support by an open

reporting culture to identify and address any issues found.

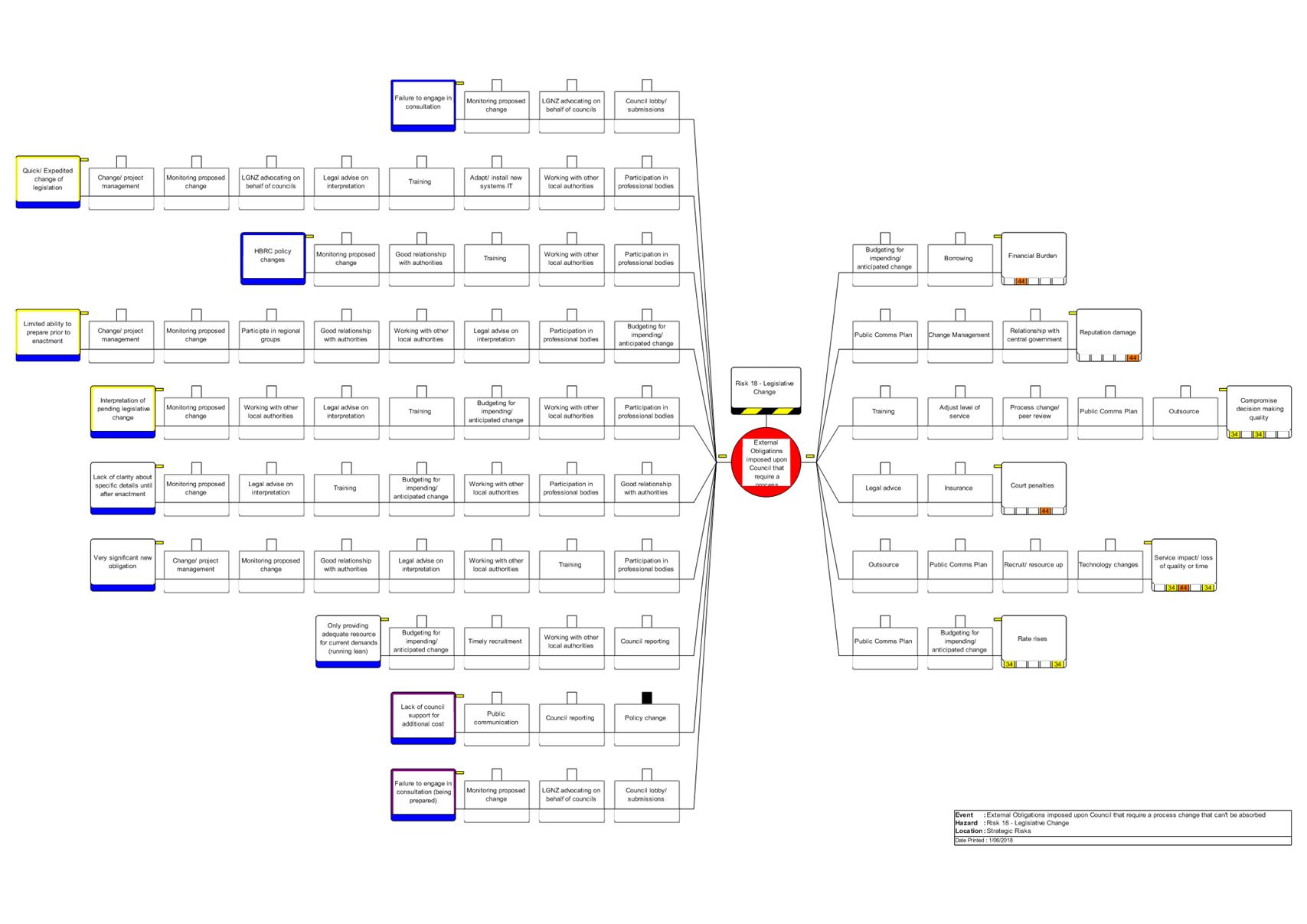

3.1.10 Legislative change (Risk #18): Legislation

change that places additional demand on the community or Council resources.

Legislative change risk covers the impacts of Central Government implementing

new or amended legislation that increases community or Local Government

responsibilities, or increases compliance obligations with which the community

or Council much comply. Note: This differs from “ability to meet

regulatory requirements” in that it refers to new obligations, rather

than ability to continue deliver an existing role.

3.1.11 Risk assessment: Through a

combination of participation in professional bodies, working with other local

authorities and various avenues for monitoring the legislative environment,

Council staff obtain early warning of pending legislative change to enable

forward planning to avoid shocks.

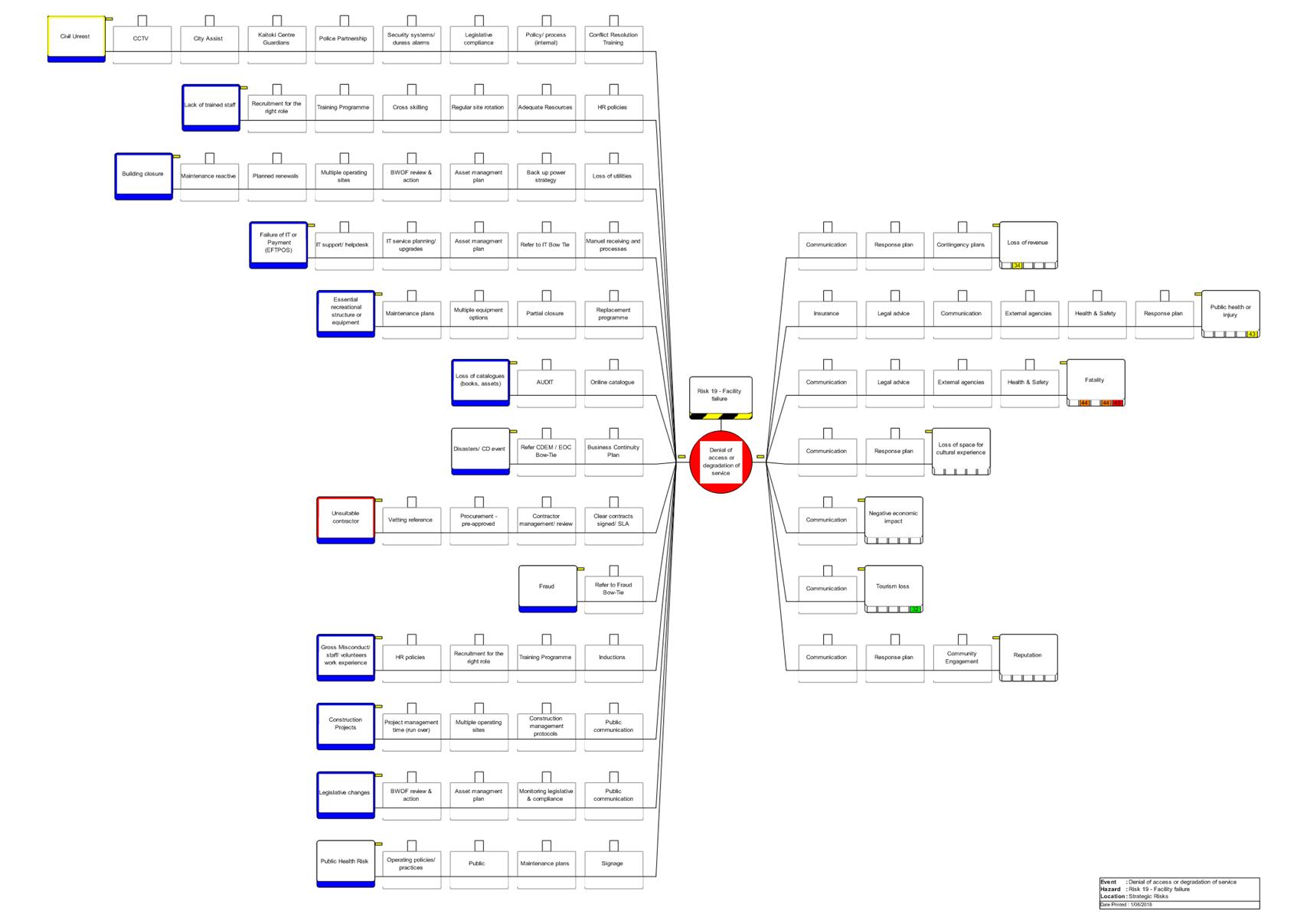

3.1.12 Facility failure (Risk #19): Facility

failure resulting in loss of community service. Facility failure risk covers a

loss or degradation in service to the community from failure of community

facing activities such as libraries, community centres, swimming pools, sport

centres and cemeteries. Failures might be caused by problems with the physical

buildings or assets, information technology system or personnel.

3.1.13 Risk assessment: Due to the

fact that facilities are duplicate across Hastings, Flaxmere and Havelock North

there is an inherent level of resilience within the delivery of community

services. However, redirecting communities to an alternative site does still

cause impacts on the community. Council also applies Asset Management Planning

practices to the management of the buildings to implement renewals and

undertakes scheduled maintenance to minimise disruption. Management of the

programmes are overseen by a central team to improve coordination. As a result

the risk of service interruption is reduced to possible.

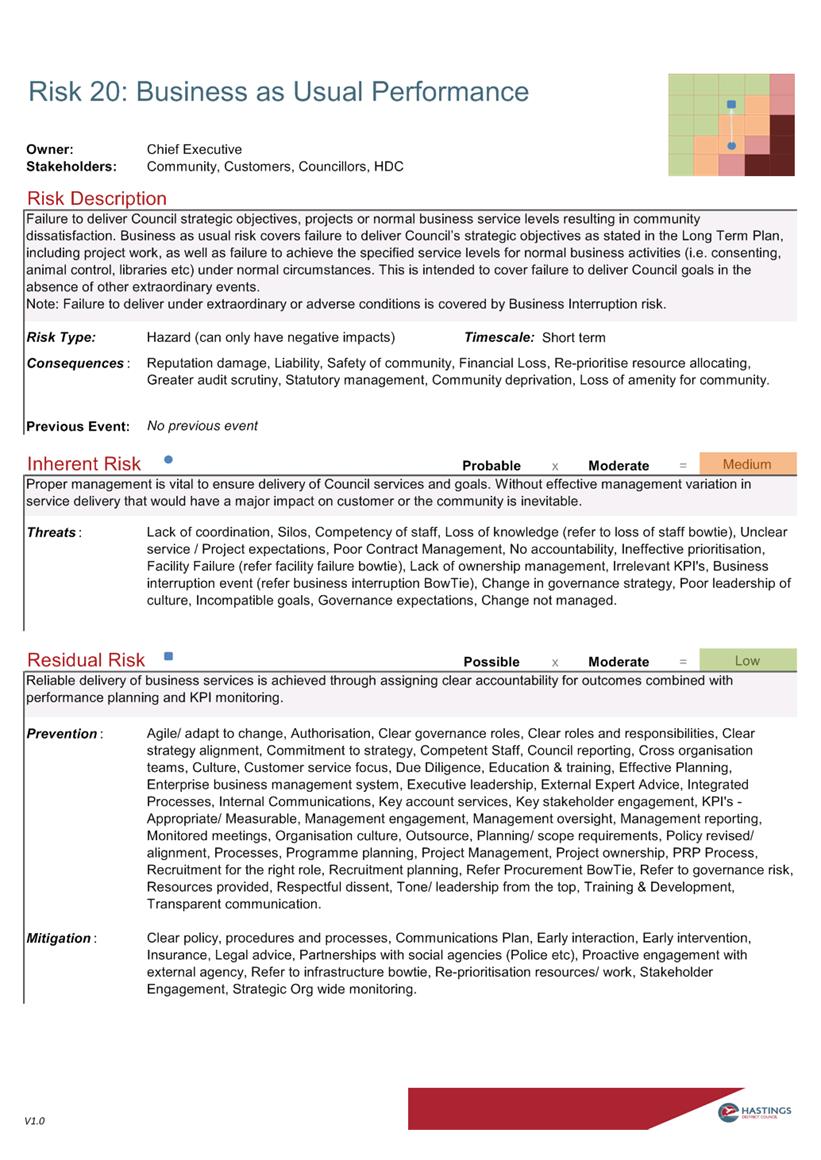

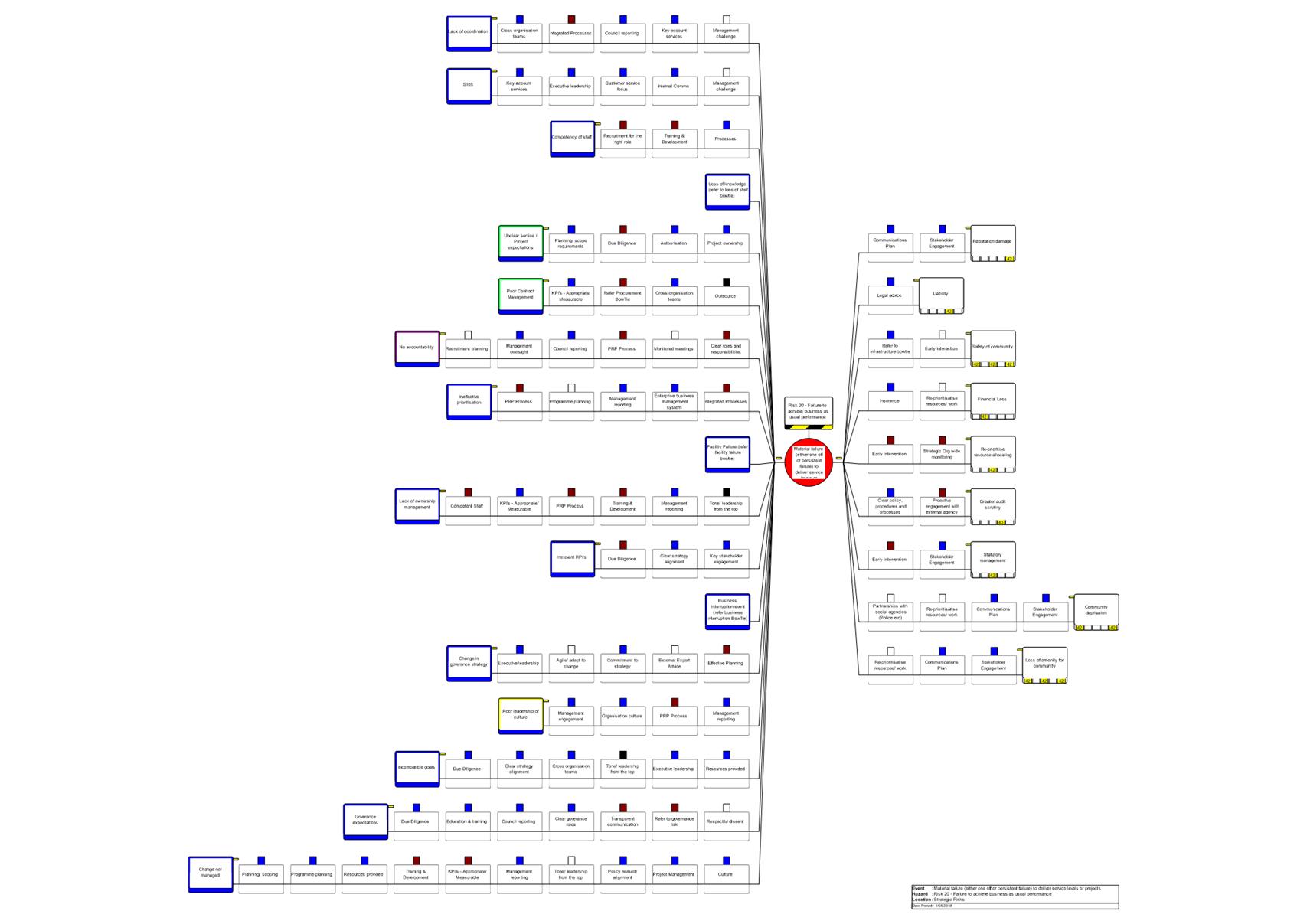

3.1.14 Failure to achieve business as

usual performance (Risk #20): Failure to deliver Council strategic

objectives, projects or normal business service levels resulting in community

dissatisfaction. Business as usual risk covers failure to deliver

Council’s strategic objectives as stated in the Long Term Plan, including

project work, as well as failure to achieve the specified service levels for

normal business activities (i.e. consenting, animal control, libraries etc)

under normal circumstances. This is intended to cover failure to deliver

Council goals in the absence of other extraordinary events. Note: Failure to

deliver under extraordinary or adverse conditions is covered by Business

Interruption risk.

3.1.15 Risk assessment: Reliable

delivery of business services is achieved through assigning clear

accountability for outcomes combined with performance planning and KPI

monitoring.

3.2 As a result of

discussion during the Council workshop in May 2018 work is underway on defining

Governance risk and associated mitigations. An update will be reported to Risk

and Audit at the next meeting.

4.0 SIGNIFICANCE AND ENGAGEMENT

4.1 While

consideration of risk is significant to efficient and effective operation of

Council, changes to the risk register are not significant in terms of Council’s

Significance and Engagement Policy and no consultation is required.

5.0 NEXT STEPS

5.1 The annual review

of the Risk Management Framework is due, and will be reported at the next

meeting.

5.2 The risk

management rollout project effort will now be directed toward developing:

5.2.1 A risk based audit

programme to provide assurance that strategic risk critical controls are

providing the intended level of mitigation, and

5.2.2 An internal training and

awareness campaign to ensure risk management is considered in operational

decision making.

|

6.0 RECOMMENDATIONS

AND REASONS

A) That the

report of the Risk and Corporate Services Manager titled “Enterprise

Risk Management Update June 2018” dated 2/07/2018

be received.

With the reasons for this decision

being that the objective of the decision will contribute to meeting the

current and future needs of communities for good quality local

infrastructure, local public services and performance of regulatory functions

in a way that is most cost-effective for households and business by:

i) Validating that risks in core business processes are effectively

managed.

|

Attachments:

|

1

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Register for

Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-138

|

|

|

2

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Summary Water

Contamination for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-139

|

|

|

3

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie Water

Contamination for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-140

|

|

|

4

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Control List

Water Contamination for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-141

|

|

|

5

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Summary Loss

of Key Staff for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-142

|

|

|

6

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie Loss

of Key Staff for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-143

|

|

|

7

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Summary

Officer Error or Omission for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-144

|

|

|

8

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie

Officer Error or Omission for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-145

|

|

|

9

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Summary

Failure to Meet Regulatory Requirements for Risk and Audit Subcommittee 2

July 2018

|

PMD-03-81-18-146

|

|

|

10

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie

Failure to Meet Regulatory Requirements for Risk and Audit Subcommittee 2

July 2018

|

PMD-03-81-18-147

|

|

|

11

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Summary

Legislative Change for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-148

|

|

|

12

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie

Legislative Change for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-149

|

|

|

13

|

Policies, Procedures, Delgtns, Warrants & Manuals

- Manuals - Risk Management - Governance Strategic Risk Summary Facility

Failure for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-150

|

|

|

14

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie

Facility Failure for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-151

|

|

|

15

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Summary

Business as Usual Failure for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-152

|

|

|

16

|

Policies, Procedures, Delgtns, Warrants &

Manuals - Manuals - Risk Management - Governance Strategic Risk Bow Tie

Business as Usual Failure for Risk and Audit Subcommittee 2 July 2018

|

PMD-03-81-18-153

|

|

|

Policies, Procedures, Delgtns,

Warrants & Manuals - Manuals - Risk Management - Governance Strategic

Risk Register for Risk and Audit Subcommittee 2 July 2018

|

Attachment 1

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Water

Contamination for Risk and Audit Subcommittee 2 July 2018

|

Attachment 2

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Water

Contamination for Risk and Audit Subcommittee 2 July 2018

|

Attachment 3

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Control List Water

Contamination for Risk and Audit Subcommittee 2 July 2018

|

Attachment 4

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Loss of Key

Staff for Risk and Audit Subcommittee 2 July 2018

|

Attachment 5

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Loss of Key

Staff for Risk and Audit Subcommittee 2 July 2018

|

Attachment 6

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Officer Error

or Omission for Risk and Audit Subcommittee 2 July 2018

|

Attachment 7

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Officer Error

or Omission for Risk and Audit Subcommittee 2 July 2018

|

Attachment 8

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Failure to Meet

Regulatory Requirements for Risk and Audit Subcommittee 2 July 2018

|

Attachment 9

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Failure to Meet

Regulatory Requirements for Risk and Audit Subcommittee 2 July 2018

|

Attachment 10

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Legislative

Change for Risk and Audit Subcommittee 2 July 2018

|

Attachment 11

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Legislative

Change for Risk and Audit Subcommittee 2 July 2018

|

Attachment 12

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Facility

Failure for Risk and Audit Subcommittee 2 July 2018

|

Attachment 13

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Facility

Failure for Risk and Audit Subcommittee 2 July 2018

|

Attachment 14

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Summary Business as

Usual Failure for Risk and Audit Subcommittee 2 July 2018

|

Attachment 15

|

|

Policies, Procedures, Delgtns, Warrants & Manuals -

Manuals - Risk Management - Governance Strategic Risk Bow Tie Business as

Usual Failure for Risk and Audit Subcommittee 2 July 2018

|

Attachment 16

|

REPORT TO: Risk

and Audit Subcommittee

MEETING DATE: Monday 2 July 2018

FROM: Manager Strategic Finance

Brent Chamberlain

Chief Financial Officer

Bruce

Allan

SUBJECT: General

Update Report and Status of Actions

1.0 SUMMARY

1.1 The

purpose of this report is to update the Subcommittee on various matters

including actions raised at previous meetings.

1.2 The

Council is required to give

effect to the purpose of local government as prescribed by Section 10 of the

Local Government Act 2002. That purpose is to meet the current and future needs

of communities for good quality local infrastructure, local public services,

and performance of regulatory functions in a way that is most

cost–effective for households and businesses. Good quality means infrastructure,

services and performance that are efficient and effective and appropriate to

present and anticipated future circumstances.

1.3 This

report concludes by recommending that the report titled “General Update

Report and Status of Actions” from the Manager Strategic Finance be

received.

2.0 BACKGROUND

2.1 The

Audit & Risk Subcommittee members requested that officer’s report

back at each meeting with progress that has been made on actions that have

arisen from the Audit & Risk Subcommittee meetings. Attached as Attachment

1 is the Audit & Risk Subcommittee Action Schedule as at 30 June 2018.

3.0 CURRENT

SITUATION

3.1 Tech

One Upgrade

3.1.1 Significant

technology upgrades to core council systems is noted as a key operational risk

to the organisation and hence the following brief update to the Subcommittee.

3.1.2 Stage

1 of the upgrade to the Technology One Finance Module is well under way and the

different packets of work are transitioning from the test environment to live

with relative smoothness.

3.1.3 Stage

2 (Procure to Pay) is also progressing with a recent trip to the Hawke’s

Bay DHB and Wellington City Council to see their Technology One based

Electronic Purchase Order systems in action and to pick up any learnings they

have on this module through their own implementations. This current stage is

all about mitigating implementation risks through thorough planning.

Council’s Strategic Projects team will be utilised to manage these system

improvement projects.

3.2 New

Zealand Transport Agency Audit

3.2.1 Every

two years the New Zealand Transport Agency (NZTA) undertake an audit of Council

with the objective of providing assurance that NZTA’s investment in

HDC’s land transport programme is being well managed and delivering value

for money. The most recent audit was undertaken in April 2018 and the following

comments were made in the executive summary of that report:

“Hastings

District Council has a well-managed land transport programme that will be

improved by accurately accounting for the cost of overheads associated with

in-house professional services and completing documentation for road safety

audits.

Council is mostly

complying with the Transport Agency’s approved procurement

procedures. However for five older contracts no late tender policy was in

place. This is a Transport Agency requirement and has now been addressed.

Claims for funding

assistance from the Transport Agency for the two financial years to 30 June

2017 were successfully reconciled to Council’s general ledger records.

Effective processes

were evident for monitoring and managing the delivery of professional services

and physical works contracts including regular site inspections.

Road safety audits

for improvement projects are being commissioned from independent

providers. However, there was incomplete documentation showing how

Council is addressing the resulting recommendations from these audits.

Council needs to

review the components and individual costs associated with each component that

go into making up the cost multiplier and adjust it if required.”

3.2.2 This

is a good outcome from this review. The relationship we have with NZTA is

extremely important and it is critical that NZTA has confidence in HDC and that

our processes and systems have credibility.

3.3 Treasury

Update

3.3.1 In

lieu of a formal quarterly treasury update, given this meeting is outside of

the normal quarterly cycle, the following is a high level update on Treasury

activity.

3.3.2 The

table below shows Council is compliant with its Treasury Policy as at 30th

June 2018:

|

Measure

|

Compliance

|

Actual

|

Min

|

Max

|

|

Liquidity

|

ü

|

113%

|

110%

|

170%

|

|

Fixed debt

|

ü

|

73%

|

55%

|

95%

|

|

Funding profile:

0 – 3 years

3 – 5 years

5 years +

|

ü

ü

ü

|

48%

23%

29%

|

10%

20%

10%

|

50%

60%

60%

|

|

Net Debt as % Equity

Net Debt as % Income

Net Interest as % Income

Net Interest as % Rates

|

ü

ü

ü

ü

|

4%

64%

3%

5%

|

0%

0%

0%

0%

|

20%

150%

15%

20%

|

3.3.3 A

further $7m has been borrowed from Local Government Funding Agency (LGFA) since

the 1st May 2018 meeting to fund the current capital spend program.

3.3.4 No

further interest rate swap transactions have been entered into.

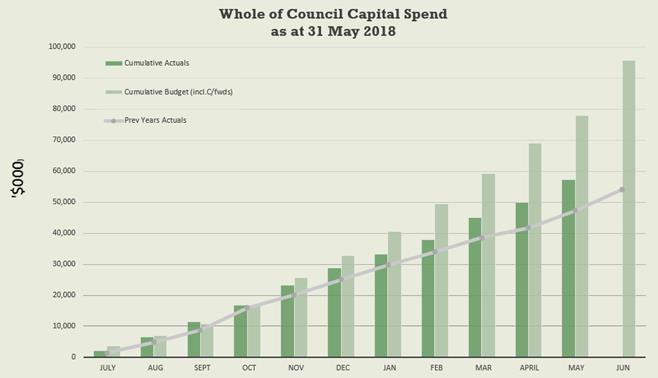

3.3.5 Below

is an update of how the Council is tracking with its capital spend program for

the year:

3.3.6 Below is a forecast of Council’s debt

requirements going forward, and the interest rate swap cover that Council has

in place.

Note

the delayed peak of $153m year 6, and the longer tail of debt than presented

for LTP purposes. This reflects the reality (as shown in 3.2.3) that capital

projects typically take longer than expected which delays the expenditure and

associated debt.

4.0 SIGNIFICANCE

AND ENGAGEMENT

This report does

not trigger Council’s Significance and Engagement Policy and no

consultation is required.

|

5.0 RECOMMENDATIONS

AND REASONS

That the report of the Manager Strategic Finance titled “General

Update Report and Status of Actions” dated 2/07/2018

be received.

|

Attachments:

|

1

|

Action Sheet 2 July 2018

|

CG-14-102

|

|

|

Action Sheet 2 July 2018

|

Attachment 1

|

|

TRIM File No. CG-14-25-00047

|

HASTINGS DISTRICT COUNCIL

Risk and Audit Subcommittee MEETING

Monday, 2 July 2018

RECOMMENDATION TO EXCLUDE THE PUBLIC

SECTION 48, LOCAL GOVERNMENT OFFICIAL INFORMATION AND

MEETINGS ACT 1987

THAT the public now be excluded from the

following part of the meeting, namely:

10 2018/19

Insurance Renewal Programme

11 Internal

Audit

12 IT

Audit Plan & Control Review

The general subject of the matter to be

considered while the public is excluded, the reason for passing this Resolution

in relation to the matter and the specific grounds under Section 48 (1) of the

Local Government Official Information and Meetings Act 1987 for the passing of

this Resolution is as follows:

|

GENERAL SUBJECT OF EACH MATTER TO BE CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION IN RELATION TO

EACH MATTER, AND

PARTICULAR INTERESTS PROTECTED

|

GROUND(S) UNDER SECTION 48(1) FOR THE PASSING OF EACH

RESOLUTION

|

|

|

|

|

|

10 2018/19

Insurance Renewal Programme

|

Section 7 (2)

(h)

The withholding

of the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

Commercial

Sensitivity.

|

Section

48(1)(a)(i)

Where the Local

Authority is named or specified in the First Schedule to this Act under

Section 6 or 7 (except Section 7(2)(f)(i)) of this Act.

|

|

11 Internal

Audit

|

Section 7 (2)

(h)

The withholding

of the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

The Internal

Audit includes the review of commercial arrangements as part of the audit

process.

|

Section

48(1)(a)(i)

Where the Local

Authority is named or specified in the First Schedule to this Act under

Section 6 or 7 (except Section 7(2)(f)(i)) of this Act.

|

|

12 IT

Audit Plan & Control Review

|

Section 7 (2)

(h)

The withholding

of the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

The internal

audit includes the review of commercial arrangements as part of the audit

process.

|

Section

48(1)(a)(i)

Where the Local

Authority is named or specified in the First Schedule to this Act under

Section 6 or 7 (except Section 7(2)(f)(i)) of this Act.

|