Hastings District

Council

Hastings District

Council

Civic Administration Building

Lyndon Road East, Hastings

Phone: (06) 871

5000

Fax:

(06) 871 5100

WWW.hastingsdc.govt.nz

Open

A G E N D A

Council MEETING

|

Meeting Date:

|

Thursday,

21 February 2019

|

|

Time:

|

1.00pm

|

|

Venue:

|

Council

Chamber

Ground Floor

Civic

Administration Building

Lyndon Road

East

Hastings

|

|

Council Members

|

Chair: Mayor Hazlehurst

Councillors Barber, Dixon, Harvey, Heaps,

Kerr, Lawson, Lyons, Nixon, O’Keefe, Poulain, Redstone, Schollum,

Travers and Watkins

|

|

Officer

Responsible

|

Chief Executive – Mr N Bickle

|

|

Council

Secretary

|

Mrs C Hunt (Extn 5634)

|

HASTINGS DISTRICT COUNCIL

COUNCIL MEETING

Thursday, 21 February 2019

|

VENUE:

|

Council Chamber

Ground Floor

Civic Administration Building

Lyndon Road East

Hastings

|

|

TIME:

|

1.00pm

|

|

A G E N D A

|

1. Prayer

2. Apologies

& Leave of Absence

At the close of the agenda no

apologies had been received.

Leave of Absences had previously

been granted to Councillor Heaps and Councillor Kerr

3. Seal

Register

4. Conflict

of Interest

Members need to be vigilant to stand

aside from decision-making when a conflict arises between their role as a

Member of the Council and any private or other external interest they might

have. This note is provided as a reminder to Members to scan the agenda

and assess their own private interests and identify where they may have a

pecuniary or other conflict of interest, or where there may be perceptions of

conflict of interest.

If a Member feels they do

have a conflict of interest, they should publicly declare that at the start of

the relevant item of business and withdraw from participating in the

meeting. If a Member thinks they may have a conflict of interest,

they can seek advice from the General Counsel or the Democratic Support Manager

(preferably before the meeting).

It is noted that while Members can

seek advice and discuss these matters, the final decision as to whether a

conflict exists rests with the member.

5. Confirmation

of Minutes

Minutes of the

Council Meeting held Thursday 31 January 2019 including minutes while the

public were excluded.

(Previously circulated)

6. Hawke's Bay Arts

Festival - 2018 Festival Report, and proposed 2019 Festival Scope and Budget 5

7. Transfer of Local

Purpose Reserve (Utility), State Highway 50, Maraekakaho 7

8. Draft Annual Plan

and budget for the 2019/20 financial year - Chief Financial Officer overview,

work programme, budget and related information. 13

9. Hawke's Bay

Disaster Relief Trust 19

10. Car Parking Lot 3, 303 Queen

Street East (Opera House Car Park) 23

11. Cemeteries and Crematorium -

Fees & Charges 31

12. Clifton to Tangoio Coastal

Hazards Strategy Joint Committee Minutes 49

13. Variation 6 to the Proposed

District Plan - Heritage Section Amendments 57

14. Monthly Financial Report -

January 2019 65

15. Health & Safety Quarterly

Report 75

16. Requests Received under the

Local Government Official Information and Meetings Act (LGOIMA) Monthly Update 95

17. Updated 2019 Meeting Schedule

Changes 99

18. Additional

Business Items

19. Extraordinary

Business Items

20. Recommendation

to Exclude the Public from Item 21 103

21. Plaza Redevelopment

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Group Manager: Community Facilities

& Programmes

Alison

Banks

SUBJECT: Hawke's

Bay Arts Festival - 2018 Festival Report, and proposed 2019 Festival Scope and

Budget

1.0 SUMMARY

1.1 The purpose of this report is to update and

inform the Council about the outcome of the 2018 Hawke’s Bay Arts

Festival, and the proposed scope and budget for a 2019 Hawke’s Bay Arts

Festival.

1.1 Arts

Inc Heretaunga will present the information related to the purpose of this

report.

1.2 This

report concludes by recommending that Council considers the information

provided by Arts Inc and provides feedback on next steps for the 2019

Hawke’s Bay Arts Festival in the context of scope and budget for the 2019

Hawke’s Bay Arts Festival.

|

2.0 RECOMMENDATIONS AND

REASONS

A) That

the report of the Group Manager: Community Facilities & Programmes

titled “Hawke's Bay Arts Festival - 2018 Festival Report, and

proposed 2019 Festival Scope and Budget” dated 21/02/2019

be received.

B) This report concludes by recommending that Council receives the

information provided by Arts Inc and provides feedback on the Hawke’s

Bay Arts Festival in the context of scope and budget for the 2019

Hawke’s Bay Arts Festival.

With the reasons for this decision

being that the objective of the decision will contribute to meeting the

current and future needs of communities for local public services in a way

that is most cost-effective for households and business.

|

Attachments:

There are no

attachments for this report.

REPORT TO: Council

MEETING DATE: Thursday 21 February

2019

FROM: Senior Projects Engineer

Steve

Cave

SUBJECT: Transfer

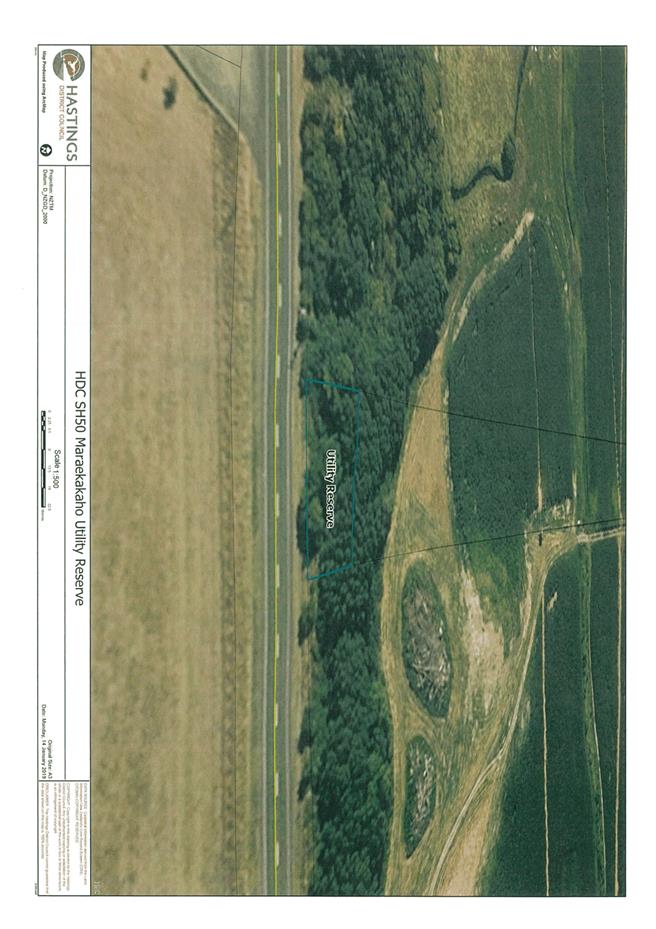

of Local Purpose Reserve (Utility), State Highway 50, Maraekakaho

1.0 SUMMARY

1.1 The

purpose of this report is to obtain a decision from Council authorising the Chief

Executive to take all steps necessary to transfer a Council-owned Local Purpose

Reserve (Utility), hereon referred to as “the Reserve”, of 556m2,

described as Lot 4 DP 11536, on State Highway 50 in Maraekakaho, to Hawke’s

Bay Regional Council (HBRC) for a public work, being Soil Conservation and

Rivers Control purposes.

1.2 This

report was left to lie on the table at 31 January 2019 Council meeting pending

the expiration of the appeal period of a Hearings Commissioner Decision on an

application from Russell Roads Ltd for a land use consent for a river gravel

processing plant near Maraekakaho, which ends on 21 February 2019.

1.3 This

request arises from an approach to Hastings District Council (HDC) from HBRC

regarding the need to secure long-term river management access to the Ngaruroro

River in the Maraekakaho area.

1.4 This

report concludes by identifying this particular section of land as being

surplus to HDC requirements and recommending that the Chief Executive be

authorised to take all practical steps necessary to transfer the Reserve to

HBRC for Soil Conservation and Rivers Control purposes for a fair and

reasonable price based on the 2016 rating valuation for this land of $25,000.

2.0 BACKGROUND

2.1 HBRC

has management and control responsibilities for rivers within the Hawke’s

Bay region which includes the Ngaruroro River. The Hawke’s Bay Regional

Resource Management Plan, (HBRRMP), along with Local Government Act and Soil

Conservation and Rivers Control Act provides the legislative context for this

responsibility. The HBRRMP Plan Objective OBJ45 is ‘The maintenance

or enhancement of the natural and physical resources, and use and values, of

the beds of rivers and lakes within the region as a whole.’

2.2 The

management and control of the three main Heretaunga Plains Rivers (Ngaruroro,

Tutaekuri and Tukituki) form part of the Heretaunga Plains Flood Control

Scheme. Activities including maintenance of river edge protection and berm

maintenance, channel maintenance activities such as beach raking and shingle

extraction, along with spraying and mowing activities are undertaken. These

activities ensure a consistent level of service is maintained for the Scheme.

2.3 Access

to these rivers for river management and control purposes are provided for at

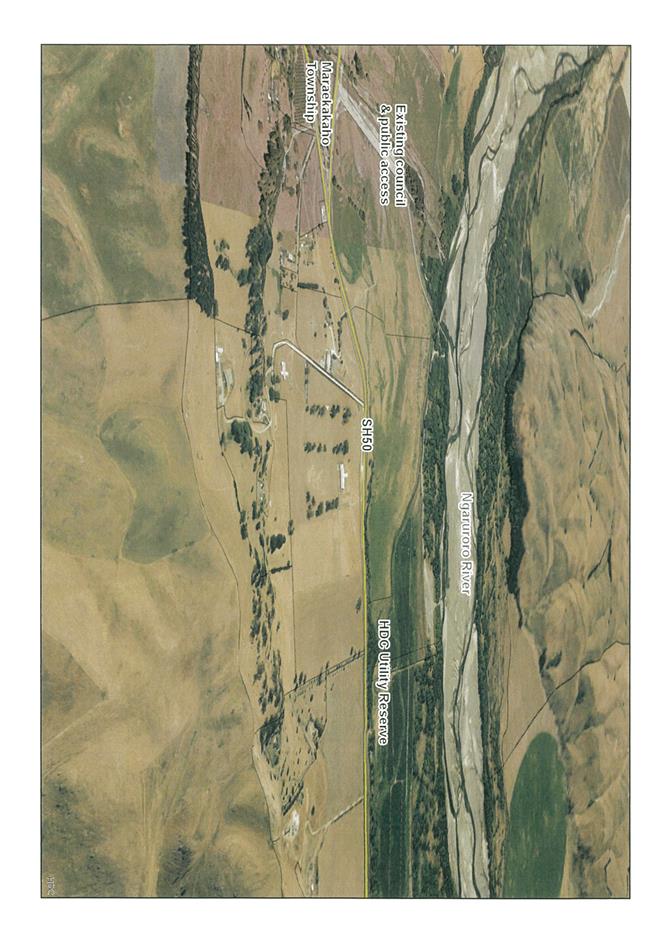

strategic locations and this includes an access to the Ngaruroro River at

Maraekakaho.

2.4 As

part of a suite of river management activities HBRC administers shingle extraction

activities at various locations on the Ngaruroro River, including the Maraekakaho

area.

2.5 Current

access to the Ngaruroro at Maraekakaho is from Kereru Road through an unsealed

legal road approximately 675 metres long. This access is also used by the general

public to access the Ngaruroro River. There is a further 1.1 kilometre section

of river access from the legal road to the river, which also crosses a section

of private land.

2.6 HBRC

desires a separate vehicular access to the Ngaruroro River for river management

purposes from State Highway 50. The objectives of the new access are to

separate these activities from the general public access to the Ngaruroro River

off Kereru Rd and to provide a more direct route to SH50 than the existing

alignment of 1.775 kilometres.

2.7 While

HBRC has been negotiating with a private landowner in this area to acquire a

Right of Way easement for access, this proposal with HDC provides for more long

term certainty and security for access for river management activities and

provides separation from the publically accessible areas of the river.

Discussions have been held with the adjoining landowner to this proposal who

has indicated support for the proposed initiative.

2.8 HBRC has

identified an alignment that accomplishes their objectives (see attached).

This proposed route passes through the Hastings District Council owned Reserve to

access SH50.

2.9 The Reserve

has an area of 556 square metres (0.0556 hectares) and is legally described as

Lot 4 DP 11536. The Reserve, originally classified as a “Utility

Reserve”, was vested in the Hawke’s Bay County Council on the

deposit of DP 11536 in April 1967. The Reserve was reclassified as a Local

Purpose Reserve through the enactment of the Reserves Act 1977. Reasons for the

original “Utility Reserve” status for local authority activities

are unknown.

2.10 The last rating

valuation for the Reserve is dated 1 August 2016 and the capital value was

assessed at $25,000.00.

2.11 HBRC has advised HDC

that they would like to obtain this Council owned reserve, for a public work

(in terms of the Public Works Act 1981) being the legal and physical access to and

from the Ngaruroro River.

2.12 With this access and

ownership over the Reserve (including the inherent accretion claim rights), HBRC

could construct a straight-line access from State Highway 50 to the Ngaruroro

River, including the shingle extraction site currently used by Russell Roads

Ltd.

2.13 The new access would

meet HBRC objectives by:

· being separate from the general public Ngaruroro River access off

Kereru Rd,

· being located on publicly owned land,

· having a straight alignment, and

· having a length of 470 lineal metres, compared with the existing 1,775

lineal metres access.

3.0 CURRENT

SITUATION

3.1 The Reserve is an

unused section of land physically indistinguishable from the adjoining land

which is covered in willow trees and owned by HDC.

3.2 The

proposal to transfer the Reserve to HBRC has been reviewed by relevant HDC staff

including the HDC Parks and Property Manager and General Counsel. Council has

no current or foreseeable future use for the Utility Reserve and no

complications are expected through transferral of the Utility Reserve to HBRC.

4.0 OPTIONS

4.1 The

three options available are:

4.2 Option

A – Do nothing.

4.3 Option

B – Sell the land to HBRC.

4.4 Option

C – Grant a Right of Way Easement to HBRC.

5.0 SIGNIFICANCE

AND ENGAGEMENT

5.1 The

Public Works Act 1981 have provisions that allow sale and transfer of land to

another Crown or Territorial Local Authority.

5.2 Under

the Public Works Act 1981 the offer-back provisions of section 40 of the Public

Works Act do not apply if the property is required by a Crown or Territorial

Local Authority for another public work.

6.0 ASSESSMENT

OF OPTIONS (INCLUDING FINANCIAL IMPLICATIONS)

6.1 Option

A – Do nothing.

6.2 If

Council does nothing, access for river management activities, including shingle

extraction, will continue to be carried out through the existing access from

Kereru Road, which is also used for public access to the river. Competing

demands and compatibility issues are ongoing in this area. River maintenance

activities, including shingle extraction, are necessary in this area as part of

maintaining the Heretaunga Plains Flood Control Scheme.

6.3 Option

B – Sell the land to HBRC for a fair and reasonable price using the 2016

rating valuation of $25,000 as the basis for price negotiations and on the

understanding that HBRC will cover all reasonable legal and survey costs to

facilitate the transaction.

6.4 This

will allow HBRC to construct a new access with no private landowner interests

and continue to provide their obligation of river control to ensure scheme and

flood control standards are maintained. The proposed access is 1.2

km’s from the existing Kereru Road access.

6.5 Option

C – Grant a Right of Way Easement to HBRC.

6.6 The

benefits are the same as Option B, with an increased set up cost, and a much

smaller compensation settlement. In terms of Public Works Act 1981

principles, Council should dispose of land it no longer requires for a public

work.

7.0 PREFERRED

OPTION/S AND REASONS

7.1 Option

B. Sell the land to HBRC.

7.2 As

Council doesn’t require the land (the Reserve) for any public purpose it can

be sold and transferred to another administering body. There is no reason for

Council to hold land for which it has no purpose. The land will assist HBRC to

fulfil its obligations under the LGA, RMA and Soil Conservation and Rivers

Control act to maintain and enhance rivers within the region.

7.3 HBRC

have confirmed that the land is required for another public work and agree to

the proposal to sell and transfer the land via the Public Works Act for a fair

and reasonable price based on the 2016 rating valuation of $25,000.

|

8.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Senior Projects Engineer titled “Transfer

of Local Purpose Reserve (Utility), State Highway 50, Maraekakaho”

which was left to lie on the table on 31 January 2019 now be uplifted and

received.

B) That

the Chief Executive be authorised to take all practical steps necessary to

transfer the Reserve to Hawke’s Bay Regional Council for a fair and reasonable price based on the 2016 rating valuation

for this land of $25,000.

With the reasons for this decision

being that the objective of the decision will contribute to meeting the

current and future needs of communities for good quality local infrastructure

and performance of regulatory functions by:

· enabling

Hawke’s Bay Regional Council to fulfil its obligations under their

Regional Resource Management Plan to maintain and enhance rivers within the

region, promoting sustainable use of land and water resources and providing

for community resilience to hazards and shocks.

|

Attachments:

|

1

|

Utility Reserve Maraekakaho Plan

|

53943#0029

|

|

|

Utility Reserve Maraekakaho Plan

|

Attachment 1

|

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Strategy Manager

Lex Verhoeven

Chief Financial Officer

Bruce

Allan

SUBJECT: Draft

Annual Plan and budget for the 2019/20 financial year - Chief Financial Officer

overview, work programme, budget and related information.

1.0 SUMMARY

1.1 The

purpose of this report is to obtain decisions from the Council on the key

matters and budget considerations for incorporation in the 2019/20 Annual Plan.

1.2 This

issue arises from the legislative requirement to produce an Annual

Plan. Changes to the Local Government Act 2002 create flexibility

as to whether a Council needs to consult with its community on an Annual Plan

and that is an option open to Council given that there are no significant or

material differences from the Long Term Plan for the 2019/20 financial year.

1.3 It is

the officers understanding however that elected members would expect the

community to be updated on Council’s plans for the coming year, and that

the opportunity for new initiatives to be brought to Council is made

available. The Annual Plan process is also proposed to be used to

undertake the legally required consultation to set-up a Council Controlled

Organisation (for the establishment of a Regional Disaster Relief Fund) Trust.

The Council is required

to give effect to the purpose of local government as prescribed by Section 10

of the Local Government Act 2002. That purpose is to meet the current and

future needs of communities for good quality local infrastructure, local public

services, and performance of regulatory functions in a way that is most

cost–effective for households and businesses. Good quality means

infrastructure, services and performance that are efficient and effective and

appropriate to present and anticipated future circumstances.

1.4 The

objective of this decision relates to numerous service delivery, decision

making, financial management and consultative provisions within the Local

Government Act 2002.

1.5 This

report concludes by recommending that the decisions made by Council at its

meeting dated 21 February 2019 are incorporated within the 2019/20 Draft Annual

Plan and form the basis of the Annual Plan Consultation Document.

1.6 This

report is supplemented by supporting financial information.

2.0 FOCUS

OF THIS BUDGET PROCESS

2.1 The

2019/20 draft Annual Plan process involves the further refinement of the annual

budget contained for that year within the Council’s Long Term Plan (Year

2 of the LTP). It is an opportunity to fine tune budget allocations and

priorities and to consider new proposals and contextual factors which may have

emerged since the LTP was adopted in 2018.

2.2 The

key initiatives signed off by Council that comprised Year Two of the Long Term

Plan remain in the 2019/20 budget. These priority areas will compliment

continued delivery of existing or improved levels of service across the wide

range of Council activities.

3.0 THE

BUDGET IN BRIEF

3.1 As

noted above, the starting point for the Annual Plan is year two of the Long

Term Plan which outlined a forecast base rates requirement increase of 2.1%

plus $100 extra for the water levy, totalling 5.3% including the water levy.

3.2 The

proposed base rate requirement increase has been set at 2.8% plus $95 extra for

the water levy, totalling 5.6% including the water levy as outlined

below. In the rural area (Rating Area Two) the impact of budget

efficiencies has enabled the proposed rate requirement to be set below the LTP

forecast. Those rural properties which are connected to Council water

supplies will also incur the $95 increase in the targeted water rate.

|

|

Total Increase

|

Rating Area One

|

Rating Area Two

|

|

LTP Forecast YR2 – including water levy

|

5.3%

|

5.7%

|

3.2%

|

|

2019/20

increase - including water levy

|

5.6%

|

6.1%

|

2.8%

|

3.3 While

this draft budget prepared for Council consideration is set in line with the

Long Term Plan forecast, but has had to accommodate ongoing cost pressures

arising from increased service level demands in the sustained period of growth

the district is experiencing. This growth is also reflected in the updated cost

inflation index (LGCI – explained below) of an approximate upward

movement of 1% over baseline costs forecast in the LTP.

Budget Context

3.4 In

line with the approach taken during previous annual planning processes, staff

have taken the opportunity to further refine financial forecasts and look at

baseline expenditure.

3.5 Hastings

District Council (along with all other local authorities) is required to use an

appropriate inflation index within its budgets from Year 2 through to Year 10

of its Long Term Plan. The Local Government Cost Index (LGCI) has been

specifically prepared for this purpose by the Bureau of Economic Research

(BERL) for the local government sector. This was developed a number of

years ago and is updated annually to keep abreast of economic changes and

data. It is the standard that the Auditor General expects to be used in

the development of a Council’s LTP.

3.6 It

was also developed to recognise that the actual “basket of goods” a

local authority purchases (i.e. pipes in the ground, bitumen on the road etc)

representing the LGCI is somewhat different to the basket of goods a household

purchases, commonly measured by the consumer price index (CPI).

3.7 The

latest release of the index from BERL shows upward cost pressure on

Council’s base costs as at June 2019 with an approximate upward movement

of 1.0%. This period of growth is forecast to be sustained through

2019/20. The Council budget has taken account of this, but more importantly has

also been based on an on the ground analysis of the costs likely to face the

Council. Where an inflation adjustment has not been needed to meet

projected actual programme or project costs, this has been deleted from the

draft budget. Staff have “interrogated” each budget item

against need and actual spend.

The Process

3.8 Given

the context for the budget above, in developing the draft Annual Plan and

budget, the starting point used was the non-inflation adjusted Year Two budget

within the Long Term Plan.

3.9 The

objective of using the non-inflated budget was to attempt to deliver works and

services for the 2019/20 year without assuming the need for inflationary (LGCI)

allowances where possible to drive efficiencies. Provision for cost

increases have been made where considered necessary. (This is a similar

process to that undertaken in recent annual planning processes).

3.10 In general, fees and

charges remain unchanged aside from inflation adjustments.

3.11 Overall Budget

Outcome - Essentially the additional costs detailed below (personnel,

insurance, drinking water, kerbside recycling and information technology along

with a number of smaller changes) have been able to be funded from savings

(budget efficiencies and rating base growth), along with refinement of the

targeted rates which fund some of these activities. As a result the

overall Annual Plan rate increase has been set at 5.6% compared to 5.3%

forecast in the LTP.

3.12 The budget reductions

made are part of the ongoing efficiency programme. In a number of key

activities however, the inflated LTP figures reflect the best forecast of

forward expenditure as researched by BERL. This is particularly the case

in large expenditure areas covered by our maintenance contracts (which include

industry cost indices). In these cases inflation adjustments have been

included in the budget.

3.13 The forecast debt

position as at 30 June 2019 is circa $122 million depending on the timing of

some projects, compared with the LTP forecast of $125m. This shows that

the substantive LTP capital development programme is on track, however this

allows for little headroom in terms of borrowing savings being able to be

applied within the Council’s budget.

Budget Pressures on Council

Salary and Wages

3.14 The Council payroll

budget for 2019/20 is substantially on target with the Year Two LTP forecast. The

budget reflects last years negotiated salary and wage adjustment plus some

minor positional changes. Council’s staffing compliment has been

adjusted in recent years to reflect various Council decisions relating to

service delivery. This year sees some additional capacity to drive

initiatives within the adopted Waste Minimisation and Management Plan,

succession planning in the building inspection function, an elevated focus on

risk management, capacity to drive development projects, a parks contract

position identified through the parks review and provision to address strategic

water considerations coming from the TANK process.

3.15 Water Supply

Management – The Council will be aware that the approach to water

supply management has changed dramatically, and Council has received regular

updates on this programme of work. This comprehensive programme is

fundamentally in line with that contained in the LTP with some further

refinements to some operating costs.

3.16 Kerbside Recycling

– The budget increase for kerbside recycling is directly

attributed to market changes in the recycling of plastics and the transition

into a new collection/processing contract for the last two months of the

financial year. Historically all plastics collected at the kerb were

exported to overseas markets, however those markets no longer exist. Only

certain high value plastics can now be sold locally and internationally.

Additional sorting and disposal costs are likely to be incurred by Council as a

result. These extra costs can be minimised to a certain extent if the

range of plastics collected at the kerb is restricted to high value plastic

items only. A decision on this is still to be made by Council.

3.17 Insurance –

The latest revaluation of Council assets along with adjustments being made in

the insurance industry to risk exposure, has seen some increase in material

damage insurance. The Risk and Audit Subcommittee provides oversight on behalf

of Council on insurance matters and is kept abreast of industry and market

changes.

3.18 Information

Technology – Further to a review undertaken (in conjunction with the

development of Council’s Information Technology Strategy) which recommended

a small step up in investment in some areas, some additional licensing and

software/hardware maintenance items have been budgeted reflecting

Council’s focus on service delivery to our community and the IT solutions

assisting to deliver this .

New

Budget items

3.19 Given the Long Term

Plans focus on some significant capital investments in the early years

(predominantly safe drinking water $47.5m) no new initiatives have been

included in the plan presented for 2019/20. This recognises that

significant rate increases are already forecast for the next two years, at

which time the Council’s Financial Strategy contains some capacity for

new initiatives.

3.20 It is however the

Council’s judgement as to the priorities for expenditure, recognising

that our context constantly changes, therefore a number of items will be

workshopped with Council prior to the meeting where officers are seeking

direction.

Below

the Line Items include:

§ HB Arts Festival

§ NZTA Footpath Subsidy and TEFAR

(accelerated financial assistance)

Other Annual Plan Matters

3.21 Regional Disaster

Relief Fund Trust– Discussions have

been held across various regional agencies (including CEG and with Regional Mayors/Chair) for the need

for a Regional Disaster Relief Fund Trust. These groups have provided

support for such an arrangement where in the event of a regional disaster Council

would have a vehicle to receive financial contributions from around the country

including central government and a mechanism for those funds to be distributed.

3.22 The mock-up of the

consultation document as outlined in section 3.27 contains the proposed wording

to give effect to the creation of the Trust for its stated purpose. A

separate paper on the agenda provides an overview of this proposal.

Compliance with Council’s Financial Strategy

3.23 In accordance with

Section 95 of the Local Government Act 2002, the Council must prepare and adopt

an annual plan. The purpose of the Annual Plan is to:

§ Set out

the proposed annual budget and funding impact statement;

§ Identify

any variations from the financial statements and funding impact statement

included in the LTP;

§ Support

the long term plan in providing integrated decision making and coordination of

resources;

§ Contribute

to the accountability to the community;

§ Extend

the opportunity for participation by the public in the decision making

processes relating to the costs and funding of activities.

3.24 Another key

requirement is to report on compliance against Council’s Financial

Strategy contained within the Long Term Plan. The draft Annual Plan will

outline Council compliance against the key fiscal parameters, all of which are

well within policy limits.

3.25 A key parameter is the

annual rates increase which is defined within the Financial Strategy as (LGCI +

4.0%), which translates to 6.3% for the 2019/20 financial year. The

proposed Annual Plan rates increase is within this level, and provides some

modest headroom for Council deliberation if required.

3.26 A further key

parameter is the Balanced Budget Benchmark, which is a measure that annual

operating revenue is set at a level to fund annual operating expenses.

The Council budget complies with this fiscal measure in 2019/20.

Annual

Plan Documentation and Engagement

3.27 A mock-up of the

Consultation Document will be circulated to Councillors. As outlined

earlier in section 1.3 the document for the community is more an informative

update document as opposed to a consultative one, with the exception of the

proposed formation of a Council Controlled Organisation.

3.28 No additional

community engagement has been planned (pending Council confirmation), as no new

issues are being presented to the community.

|

4.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Strategy Manager titled “Draft Annual

Plan and budget for the 2019/20 financial year - Chief Financial Officer

overview, work programme, budget and related information.” dated

21/02/2019 be received.

B) That the Council resolves in terms of section 82(3) of the Local

Government Act 2002, that the principles set out in that section have been

observed in such a manner that the Hastings District Council considers, in

its discretion, is appropriate for the decisions made during the course of

this meeting.

C) That the Draft 2019/20 Annual Plan be prepared on the basis of

this report and supporting documentation including decisions made at this

meeting, and that the Draft Annual Plan and Consultation Document be reported

back for Council adoption on 28 March 2019.

|

Attachments:

There are no

attachments for this report.

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Chief Financial Officer

Bruce

Allan

SUBJECT: Hawke's

Bay Disaster Relief Trust

1.0 SUMMARY

1.1 The

purpose of this report is to obtain a decision from the Council on a proposal

to establish a Hawke’s Bay Disaster Relief Trust and to consult on its

establishment through the 2019/20 Annual Plan.

1.2 This

proposal arises from discussions held with the Group Manager/Group Controller

for Hawkes Bay Civil Defence Emergency Management Group, the CEG and the

Regional Advisor from the Ministry of Civil Defence and Emergency Management.

1.3 The

Council is required to give effect to the purpose of local government as prescribed

by Section 10 of the Local Government Act 2002. That purpose is to meet the

current and future needs of communities for good quality local infrastructure,

local public services, and performance of regulatory functions in a way that is

most cost–effective for households and businesses. Good quality means

infrastructure, services and performance that are efficient and effective and

appropriate to present and anticipated future circumstances.

1.4 The

objective of this decision relevant to the purpose of Local Government is to

enable local public services to be delivered in an effective and efficient way

in the event of a major disaster.

1.5 This

report concludes by recommending that the proposal to establish the Hawkes Bay

Disaster Relief Trust be included in the 2019/20 Annual Plan.

2.0 BACKGROUND

Hawke’s Bay is

currently lacking a vehicle to receive funds in the event of a major disaster.

3.0 CURRENT

SITUATION

3.1 The

Hawke’s Bay Civil Defence Emergency Management (CDEM) Group is a

collective of the five Hawke’s Bay local authorities required under the

CDEM Act 2002 to govern and manage CDEM within the region. The Group is

governed by a joint committee consisting of the Mayors and the Chairperson of

the regional council.

3.2 The

approved CDEM Group Plan 2014-19 has an objective seeking to establish a

Hawke’s Bay Disaster Relief Fund with the objective of collecting and

distributing donations made by the public and organisations to assist people

affected by a civil defence emergency in Hawke’s Bay. Establishing

the fund will enable the mechanisms to be put in place before a disaster occurs

to immediately seek and administer donations as a charity. This will

allow for donated funds to be distributed as quickly as possible to those most

in need.

3.3 Any collected

funds that would be placed in the fund are not Council funds, nor are they

funds that would otherwise be coming to the Council. The fund will need

to be administered by a Trust.

3.4 As

the Trustees will need to be appointed by the Hawke’s Bay Councils, it is

necessary to establish a Council Controlled Organisation (CCO) under the Local

Government Act to form and administer the fund. This would trigger the

consultation provisions under the Local Government Act. It is therefore

requested the Council include the intention to establish a CCO for the purposes

outlined above in the draft 2019/20 Annual Plan being released for

consultation.

3.5 The

local authorities of the region have undertaken to consult with their

communities in a similar approach to that outlined here for Hastings District

to complete the processes required to establish the Trust.

4.0 OPTIONS

4.1 The

options are either to approve or not approve the formation of the Trust.

5.0 SIGNIFICANCE

AND ENGAGEMENT

5.1 The

Local Government Act provides the guidance as to the steps that are required to

form a Council Controlled Organisation. The approach recommended within

the report will satisfy those requirements.

6.0 ASSESSMENT

OF OPTIONS (INCLUDING FINANCIAL IMPLICATIONS)

6.1 To

not approve the formation of the Trust will mean that Hastings District will

not be supporting an objective of the CDEM Group Plan, and will mean that

Hawkes Bay will continue to lack a vehicle to receive funds in the event of a

major disaster.

6.2 Approving

the proposal to form the Trust and to include this for consultation within the

2019/20 Annual Plan will enable the statutory processes to be completed to

establish the Trust and to obtain the benefits from having it in place.

7.0 PREFERRED

OPTION/S AND REASONS

7.1 The

preferred option is to include the proposal to establish the Trust within the

2019/20 Annual Plan for consultation. There are no financial implications

from this proposal.

|

8.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Chief Financial Officer

titled “Hawke's

Bay Disaster Relief Trust” dated 21/02/2019 be received.

B) That the Council include the proposal to form the establishment of

the Hawkes Bay Disaster Relief Trust within its 2019/20 Annual Plan to fulfil

the statutory requirements in creating a Council Controlled Organisation.

With the reasons for this decision

being that the objective of the decision will contribute to meeting the

current and future needs of communities for local public services in the

event of a major disaster.

|

Attachments:

There are no

attachments for this report.

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Community Safety Manager

John

Payne

SUBJECT: Car

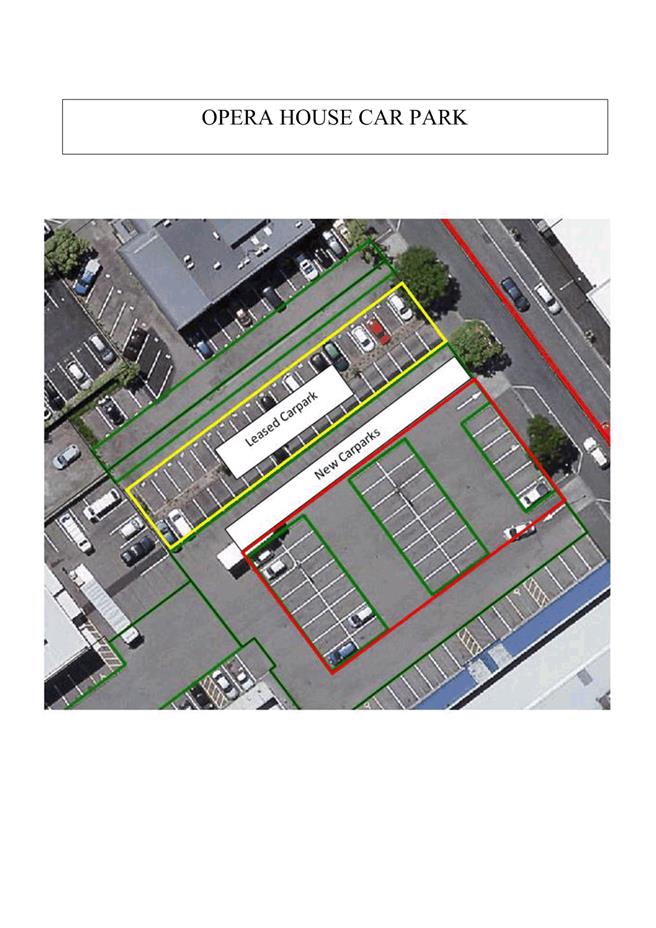

Parking Lot 3, 303 Queen Street East (Opera House Car Park)

1.0 SUMMARY

1.1 The

purpose of this report is to obtain a decision from Council on an additional parking

control in the District.

1.2 This

proposal arises as a result of the purchase of a new parking area.

1.3 Council

is required to give effect to the purpose of local government as prescribed by

Section 10 of the Local Government Act 2002. That purpose is to meet the

current and future needs of communities for good quality local infrastructure,

local public services, and performance of regulatory functions in a way that is

most cost–effective for households and businesses. Good quality means

infrastructure, services and performance that are efficient and effective and

appropriate to present and anticipated future circumstances.

1.4 The

objective of this decision relevant to the purpose of Local Government is the

provision of quality infrastructure and local public service.

1.5 This

report concludes by recommending that a 180 minute time limit be established in

the new Opera House Carpark

2.0 BACKGROUND

2.1 The

Hastings City Centre strategy (‘the Strategy”), Hastings City

Centre Parking Strategy and Vibrancy Plan have the common vision of making

Hastings City a more vibrant centre that people want to spend time in. Significant work has been undertaken to identify a suitable retail

spine of linked carpark sites, which included the creation

of new pedestrian laneways and linkages in the 100 – 300 East blocks. The

laneways are specific objectives of the above strategies.

2.2 With

the increase in use and opportunities for retail and commercial activity it has

been identified that parking will be an issue and on the current footprint

there is no space allocated or deem appropriate to dedicate to parking for

larger shows or events.

2.3 Following

the purchase of the car park area in the old Briscoes site (300 block East),

parking controls are being sought.

2.4 Pursuant

to a Hastings District Council Bylaw, the parking controls need to be formally

passed by resolution before any enforcement monitoring can be undertaken.

2.5 The

following information provides the background and current situation relevant to

the control being proposed.

3.0 CURRENT

SITUATION

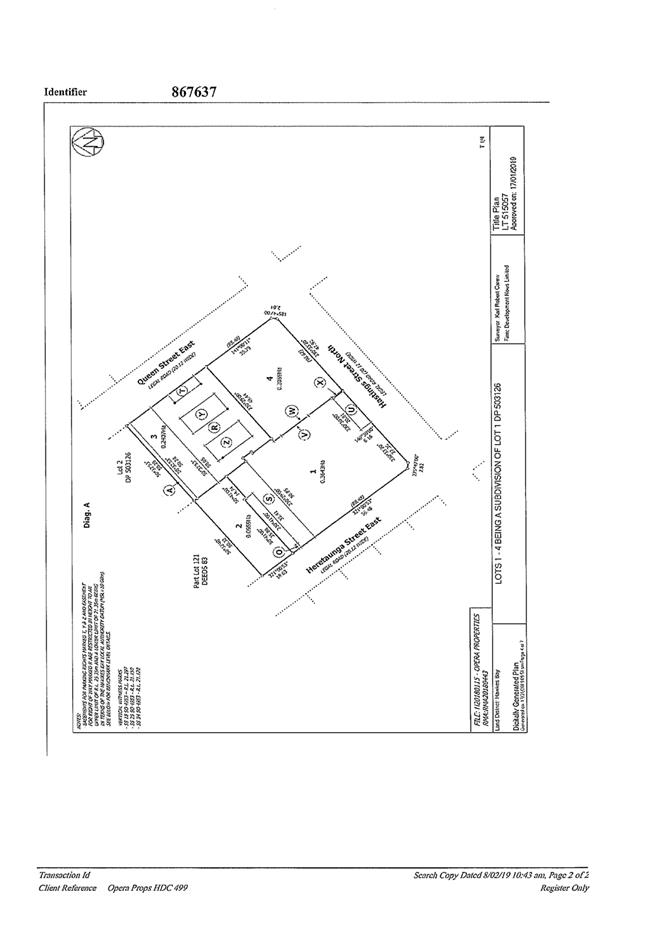

3.1 Hastings

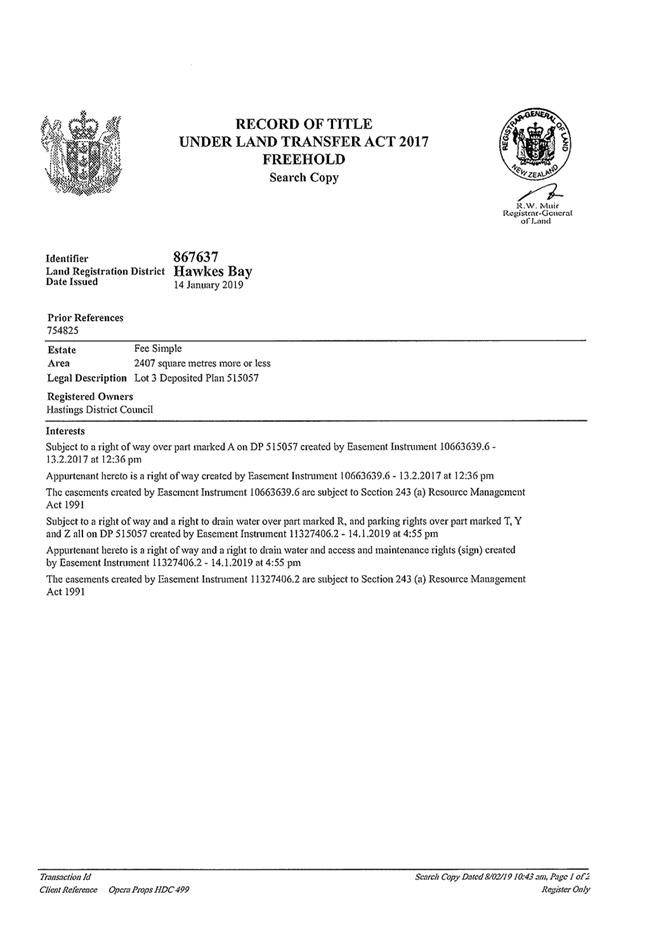

District Council has completed the subdivision to create the new Opera House

carpark as shown on the attached plan Attachment

1. We have received

confirmation from Bannister von Dadelszen that Lot 3 is now registered in the

Council’s name and this is confirmed as Attachment

2 showing HDC as the owner.

3.2 As

part of the negotiation to acquire Lot 3 as a carpark that would be available

to users of the Municipal Building and the Opera House it was agreed that the

only controls that would be put in place would be time limits. The

neighbouring properties who have rights to use parts of Lot 3 for up to 180

minutes (3 hours). Therefore it is logical from a consistency point of

view and avoid problematical enforcement that we use 180 minute stay period for

all carparks other than those leased carparks.

3.3 To

enable enforcement of any parking restriction being time limited, Council needs

to pass a resolution subject to its Consolidated Bylaws. This is the

primary purpose of this report.

4.0 OPTIONS

4.1 This is

a relatively simple matter and the available choices are limited due to the

need to be consistent with the agreements reached prior to the purchase of Lot

3.

4.2 The

options available to Council are to:

Option 1

Approve the change

being proposed - 38 carparks (as indicated in the red area of the attached map)

be allocated a 180 minute time limit, with no charge.

Advantages:

This

is in line with the rights to use parts of Lot 3 by neighbours for up to 180

minutes.

Disadvantages:

Surrounding

on-street controls are 120 minutes. This may encourage motorists to park

in the 180 area to avoid having to move as frequently.

Option 2

Have

no controls and allow parking to be self- regulated.

Advantages:

No

enforcement would be required.

Disadvantages:

People

working in the area would likely use the site for all day parking creating no

traffic turn over.

Option 3

Introduce

parking payment machines and charge for parking.

Advantages:

This

would generate revenue.

Disadvantages:

This

would be contrary to the conditions of sale. There would be capital

expenditure to purchase and install parking machines.

5.0 SIGNIFICANCE

AND ENGAGEMENT

5.1 The

matters in this report are not significant in terms of Council’s

Significance Policy. However through engagement with the property owners

and tenants through their agents, it has been expressed clearly that existing

time limits of 180 minutes be retained which would give daytime users more than

adequate time to attend the gym or use the retail facilities on site.

Obviously with the majority of shows and productions at the Opera House being

in the evening, the proposed time limits will also work well with these group

of users. This will avoid conflict of patrons using the New World

carpark.

6.0 PREFERRED

OPTION/S AND REASONS

6.1 Considering the advantages and

disadvantages in the options outlined above it is considered the best option

which meets Council’s needs for the Opera House is the 180 minute time

limit as outlined below.

· This will encourage 3 hourly traffic turn over.

· This allows Council to meet the right-of-way obligations under the

purchase agreement.

· This will help provide ready parking for patrons attending events at

the Opera House.

6.2 Therefore

it is recommended that Council pursue Option 1.

|

7.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Community Safety Manager titled “Car

Parking Lot 3, 303 Queen Street East (Opera House Car Park)”

dated 21/02/2019 be received.

B) That pursuant to Clause 5.3.1(a)(i) of Chapter 5 (Parking and

Traffic) of the Hastings District Consolidated Bylaw 2016, that 38 carpark

spaces in the Opera House Carpark, at Lot 3 303 Queen Street West, as set out

in the map attached to the report in Attachment A be resolved to have a 180

minute time limit.

With the reasons for this decision

being that the objective of the decision will contribute to performance of

regulatory functions in a way that is efficient and effective and appropriate

to present and future circumstances by:

· providing

parking spaces in relevant places within the district that are safe and

readily available to motorists.

|

Attachments:

|

1

|

Regulatory Operations - Parking - Car parks -

Parking Controls - Opera House Carpark - P180 Time Limit

|

REG-22-03-12-19-449

|

|

|

2

|

Post Registration Search - 303 Queen Street East

|

CG-14-1-01157

|

|

|

Regulatory Operations - Parking - Car

parks - Parking Controls - Opera House Carpark - P180 Time Limit

|

Attachment 1

|

|

Post Registration Search - 303 Queen Street East

|

Attachment 2

|

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Cemetery Manager

Isak

Bester

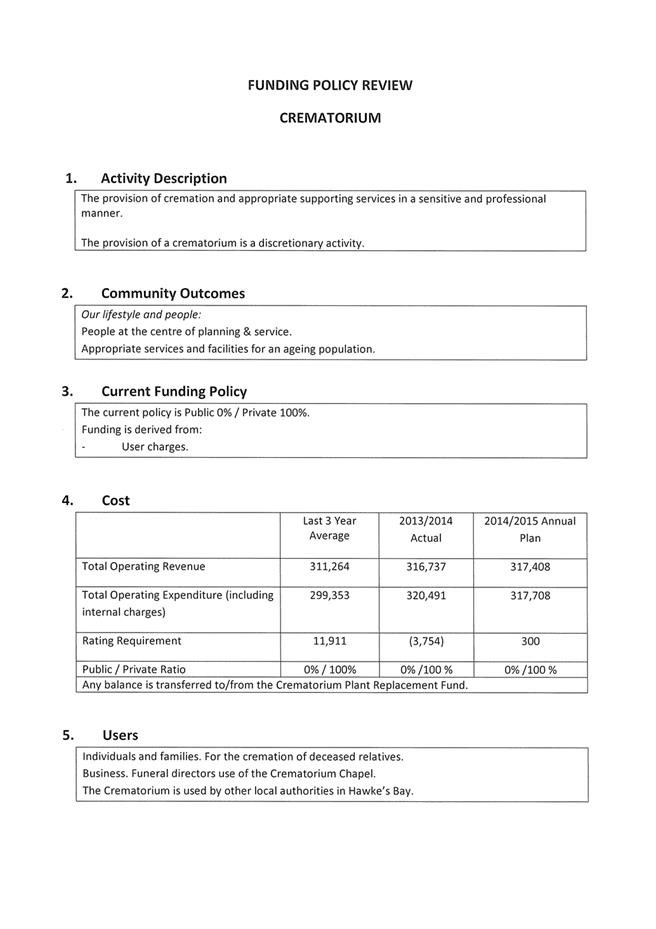

SUBJECT: Cemeteries

and Crematorium - Fees & Charges

1.0 SUMMARY

1.1 The

purpose of this report is to obtain a decision from Council on Fees and Charges

at the Hastings District Council Cemeteries & Crematorium.

1.2 This

proposal arises from the increased costs to operate the Cemeteries and

Crematorium due to the following factors:

· Increase in utilities, maintenance and operating costs.

· Incurred costs in operating a larger chapel.

1.3 There

are other areas that will also have an impact on the management of the

Cemeteries and Crematorium such as:

· Costs towards the development and maintenance of the approved new

extension to Mangaroa cemetery.

· Not allowing pre-purchasing of plots due to limited space in

cemeteries.

· Not charging any fee for stillborn burial and ash interment plots.

· Cremation of oversize caskets takes up to twice as long as that of a

standard casket.

· No call out fee after hours for same day bookings.

· Costs associated with regular air discharge testing regulations.

1.4 The

Council is required to give effect to the purpose of local government as

prescribed by Section 10 of the Local Government Act 2002. That purpose is to

meet the current and future needs of communities for good quality local

infrastructure, local public services, and performance of regulatory functions

in a way that is most cost–effective for households and businesses. Good

quality means infrastructure, services and performance that are efficient and

effective and appropriate to present and anticipated future circumstances.

1.5 The

objective of this decision relevant to the purpose of Local Government is to

provide quality local public services and facilities in relation to cemeteries

and crematoria for the Hawke’s Bay region that is accessible when needed,

whilst lowering the impact on the ratepayer and remaining in step with similar

facilities. The proposed changes to fees is due to the increase in utility,

maintenance and operating costs. We are now also required to pay additional

costs in air discharge testing due to new consent conditions. The proposed fees

and charges have been compared to nine other local authorities across New

Zealand. Bench marking of 4 other Councils is shown in 2.2 of this report.

1.6 It is

also important to note that there has not been any increases in fees and

charges since 2012.

1.7 This

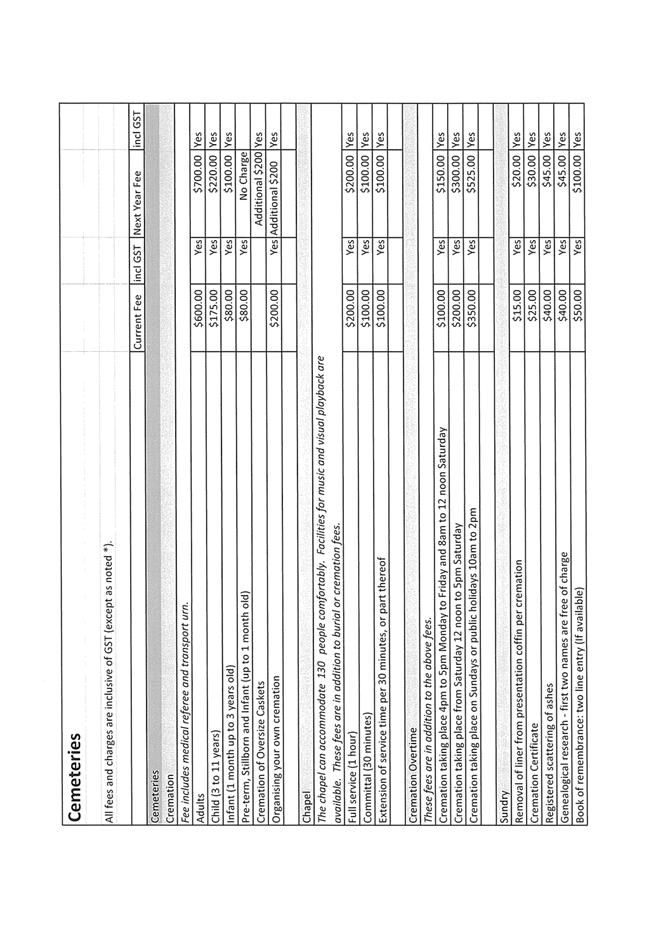

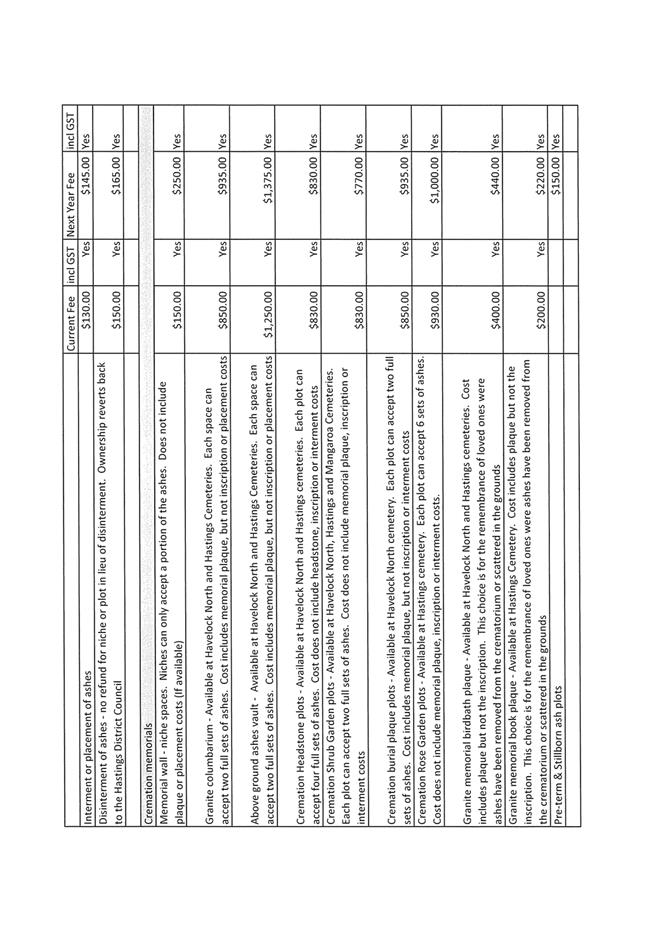

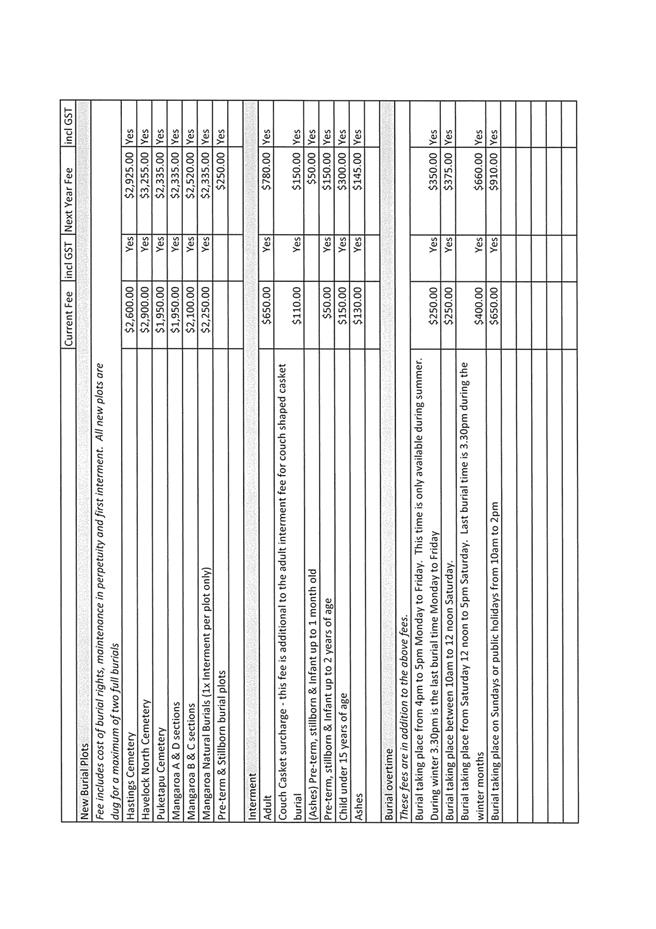

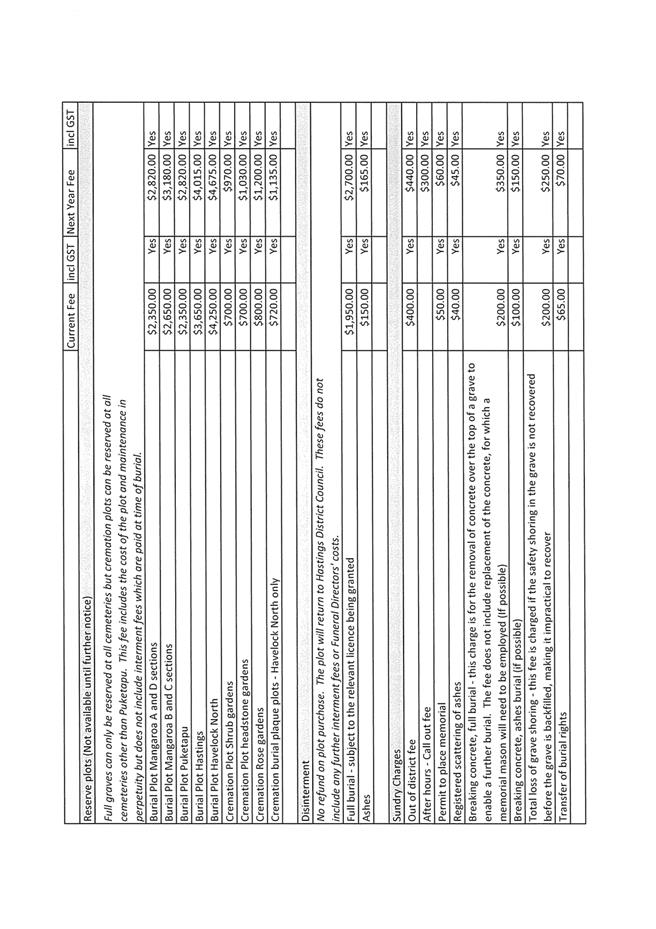

report concludes by recommending that the Cemeteries and Crematorium fees and

charges be increased as detailed in (Attachment 1) to this report and

that new fees as proposed in (Table 1) of the report be implemented.

2.0 BACKGROUND

2.1 Fees

and charges for Hastings District Council Cemeteries were last reviewed and

adjusted in the 2011/12 financial year.

2.2 In

comparison to cemetery and crematoria fees of other Local Authorities, Hastings

District Councils are between the lower and mid-range of the scale as can be

seen in the table below.

|

|

Wanganui

|

New

Plymouth

|

Dunedin

|

Palmerston

North

|

Hastings

District Council

|

|

Burial

plots incl. Interment fee

|

$2419

|

$5462

|

$4735

|

$4773

|

$2387 (Avg. across 4 cemeteries)

|

|

Ash

plots

|

$761

|

$1620

|

$921

|

$841

|

$830

|

|

Cremations

|

$682

|

$761

|

$943

|

$578

|

$600

|

2.3 Major

components of the Cemetery price list are plot purchases, maintenance in

perpetuity and interment fees.

2.4 Council

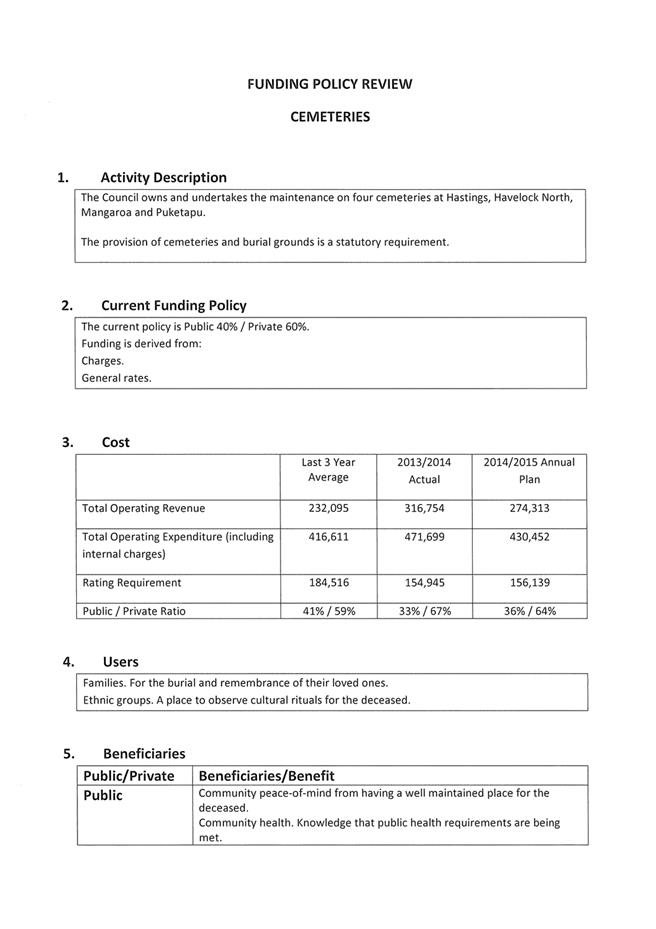

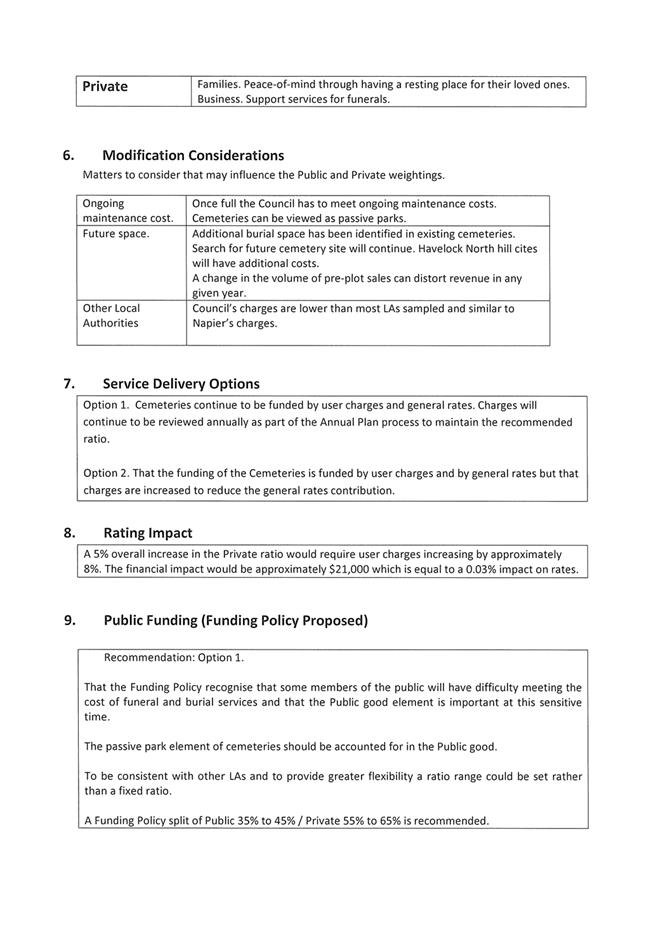

funding policy for cemeteries (Attachment 2) is to recover most of the operational

costs excluding depreciation from those benefiting from the provision of burial

and ash plots. The current target is 65% cost recovery. At present cemeteries

are tracking at 54% and revenue needed to get into policy parameters is

approximately $33,068. The balance of funds comes from general rates and funds

the park like environment provided by cemeteries.

2.5 Council

policy for the crematorium (Attachment 3) is that full cost recovery (100%) is

made from the direct beneficiaries of the service through fees and charges. At

present the crematorium is tracking at 97% and revenue needed to bring us in

line with policy parameters is $6,537.

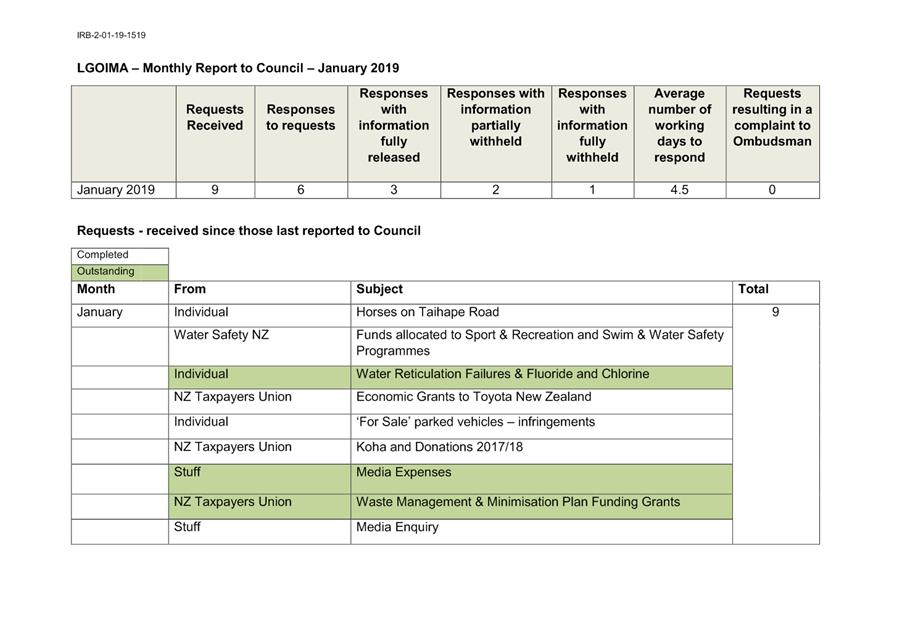

2.6 In

August 2017 pre-purchasing of burial and ash plots was put on hold due to

limited space in cemeteries. This caused a drop in revenue over the last

financial year and will have an impact on the next financial year as well.

2.7 During

the cemeteries and crematorium workshop in July 2018, Council was in favour of

implementing fees regarding burial plots for pre-term and stillborn babies, while

cremations for pre-term, stillborn and infants up to 1 month old be delivered

free of charge. (Table 1 – shown in 4.2 of this report).

The past 12 months we

dealt with 8 body burials and 12 cremations regarding pre-term and stillborn

infants.

2.8 Projections

for the 2019/20 financial year will see burial numbers at a level comparable

with 2017/18 and cremation numbers at slightly increased levels.

3.0 CURRENT

SITUATION

3.1 The

costs for providing burial and cremation services as well as the maintenance of

facilities, machinery and equipment increases yearly and the current fees and

charges are not sufficient to recoup costs, especially with new developments at

Mangaroa cemetery looming and the additional testing that is required regarding

air discharge under the new cremator consent conditions.

3.2 HDC

fees and charges for Cemetery and Crematorium services are below average when

compared nationally as can be seen in the table below.

|

|

Average

fees of the 4 cemeteries compared

|

Hastings

District Council Cemeteries fees

|

|

Burial

plots incl. interment

|

$4347

|

$2387

|

|

Ash

plots

|

$1035

|

$830

|

|

Cremations

|

$741

|

$600

|

3.3 During

their last meeting on the 5th of December 2018, the Hawke’s

Bay Crematorium Committee requested officers to investigate the implementation

of a relevant charge for cremating oversize caskets. A standard cremation takes

on average 02h30 to complete. An oversize cremation takes between 04h30 up to

05h30 to complete.

3.4 After

hour call outs for arranging urgent burials and cremations are on the increase.

HDC pays staff overtime for these call outs. There is no charge in place to

recoup the costs.

4.0 OPTIONS

4.1 Retain

fees and charges at their current level.

4.2 Raise

fees and charges for services as per (Attachment 1) and implement new

charges as proposed in (Table 1)

Table 1

(Proposed new charges

regarding burials and cremations – Pre-term, stillborn and babies up to 1

month old + Oversize Cremation Caskets & After hours call out fee).

|

Cemetery Area

|

Plot Price

|

Interment Fee

|

Maintenance Fee

|

Total Cost

|

|

Ash plot

|

$100

|

$25

|

$50

|

$175

|

|

Body plot

|

$200

|

$50

|

$50

|

$300

|

|

Stillborn Cremation

|

|

|

|

NO CHARGE

|

|

Oversize Cremation Caskets

|

|

|

|

Additional fee $200

|

|

After hours - Call Out Fee

|

|

|

|

$300

|

5.0 SIGNIFICANCE

AND ENGAGEMENT

5.1 In

accordance with Council’s Policy on Determining Significance this matter

has been assessed as being of low significance.

5.2 The

fees and charges schedule is ordinarily set by Council resolution, with the

charges taking effect from the start of the financial year.

5.3 Given

the magnitude of change proposed for some of the fees (particularly the

following: plot purchase fees for Mangaroa cemetery, disinterment fee, overtime

fees and the breaking of concrete fees), it is recommended that the fees and

charges as set out in (Attachment 1) are incorporated within the Council

fees and charges section of the Draft Annual Plan to enable community views to

be sought prior to ratifying the plan in June 2019.

5.4 Research

on fees and charges has taken place through the perusal of nine other Council

websites. Recommended adjustments are in line with fees charged by various

Councils nationally.

5.5 Council

fees and charges regarding cemeteries was last increased in 2012.

5.6 Introducing

new prices around stillborn burial and cremation plots and discontinuing with

cremation charges for this group were discussed during the Cemeteries and

Crematorium Workshop with Council on 12 July 2018. (See Table 1 above)

5.7 At

the last meeting of the Hawke’s Bay Crematorium Committee on 5 December

2018, the Committee tasked officers to investigate the implementation of an

additional charge for cremating oversize caskets. Oversize caskets takes up

to twice as long to complete compared to a standard casket cremation but is

charged at the same rate currently.

6.0 ASSESSMENT

OF OPTIONS (INCLUDING FINANCIAL IMPLICATIONS)

6.1 Retaining

the fees and charges at their current level would not address the issue of

declining cost recovery levels.

6.2 Increasing

the fees and charges (Attachment 1) as well as implementing proposed new

fees (Table 1) would address cost recovery levels and lessen the burden

on the ratepayer.

7.0 PREFERRED

OPTION/S AND REASONS

7.1 To increase

the relevant fees and charges for Cemetery and Crematorium services as per Attachment

1. The charges as outlined in Table 1 are incorporated in Attachment 1 of

this report.

|

8.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Cemetery Manager titled “Cemeteries and

Crematorium - Fees & Charges” dated 21/02/2019

be received.

B) That

Council approve the new schedule of Cemetery and Crematorium fees and charges

set out in Attachment 1 to take effect from 1 July 2019.

With the

reasons for this decision being that the objective of the decision will

contribute to meeting the current and future needs of communities for good

quality local infrastructure and local public services in regards to

cemeteries and crematoria.

|

Attachments:

|

1

|

Fees and Charges 2019

|

CG-14-73-00042

|

|

|

2

|

Cemeteries Funding Policy Review

|

CG-14-1-01159

|

|

|

3

|

Crematorium Funding Policy Review

|

CG-14-1-01160

|

|

|

Fees and Charges 2019

|

Attachment 1

|

|

Cemeteries Funding Policy Review

|

Attachment 2

|

|

Crematorium Funding Policy Review

|

Attachment 3

|

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Principal Advisor: District

Development

Mark

Clews

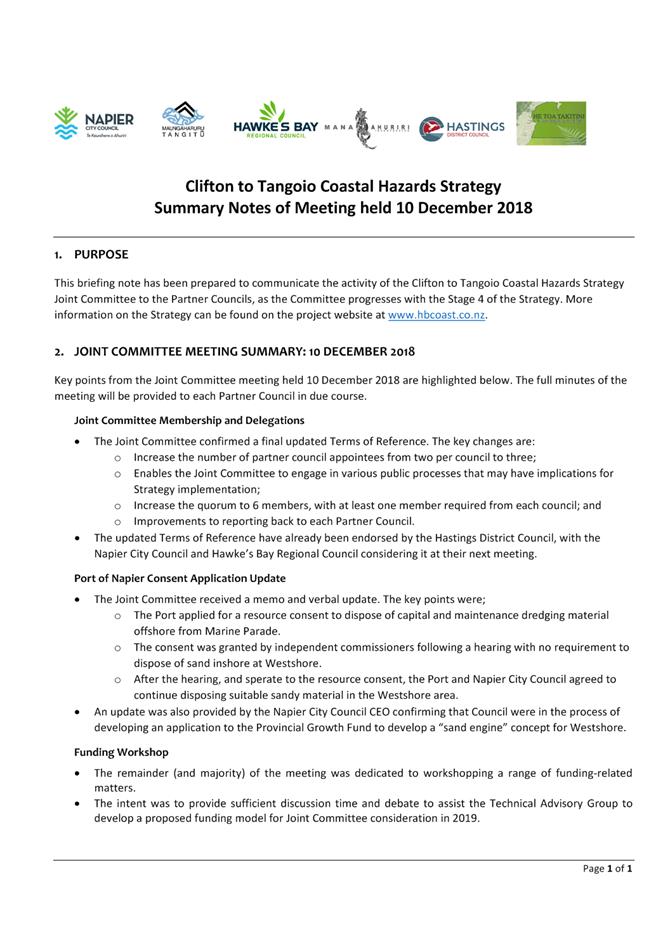

SUBJECT: Clifton

to Tangoio Coastal Hazards Strategy Joint Committee Minutes

1.0 SUMMARY

1.1 The

purpose of this report is to provide an update on for the Clifton to Tangoio

Coastal Hazard Strategy Joint Committee.

1.2 Attached

are the minutes of the meeting held on 10 December 2018 (Attachment 1)

1.3 As

required by the revised terms of reference endorsed by Council on 20 November

2018, summary notes from that meeting are also attached, and the

Council’s representative on the Technical Advisor Group will be in

attendance to help answer any questions that may arise.

|

2.0 RECOMMENDATIONS

AND REASONS

A) That the

report of the Principal Advisor: District Development titled “Clifton

to Tangoio Coastal Hazards Strategy Joint Committee Minutes”

dated 21/02/2019 be received.

B) That officers

assist Council in preparing a remit to Local Government New Zealand seeking

central government funding support for climate change and sea level rise

adaptation.

C) That a Council

workshop be held after 28 March 2019 to discuss the funding policy for the

Coastal Strategy.

|

Attachments:

|

1

|

Minutes of Joint Committee meeting 10 December 2018

|

STR-14-07-19-580

|

|

|

2

|

Summary notes from 10 December 2018

|

STR-14-07-19-579

|

|

|

Minutes of Joint Committee meeting 10

December 2018

|

Attachment 1

|

|

Summary notes from 10 December 2018

|

Attachment 2

|

REPORT TO: Council

MEETING DATE: Thursday 21 February

2019

FROM: Senior Environmental Planner

(Policy)

Anna

Summerfield

SUBJECT: Variation

6 to the Proposed District Plan - Heritage Section Amendments

1.0 SUMMARY

1.1 The purpose of this report is to inform and update the Council on

the status of the Resource Management Act 1991 process that relates to

Variation 6 to the Proposed District Plan – Heritage Section Amendments. The

report also seeks a decision from Council to adopt Variation 6 without

amendment.

1.2 The

purpose of Variation 6 to the Proposed District Plan is to correct an

inconsistency in the activity status of internal alterations to heritage

buildings within the Te Mata Special Character Zone and to identify a new

Heritage Building (Vidal House at 291 Te Mata Road) within the Te Mata Special

Character Zone (Appendix 49 of the Proposed Plan).

1.3 This

matter arises from a request from Mr and Mrs Bradshaw of 291 Te Mata Road,

Havelock North to identify the residential dwelling on their property as a

heritage building and list this building for protection under the Proposed

District Plan provisions.

1.4 The

Strategy, Planning and Partnerships Committee of Council considered this matter

on the 15th November 2018 and resolved to publicly notify this

Variation to the Proposed District Plan in order to install these changes into

the Proposed District Plan.

1.5 Council

is required to give effect to the purpose of local

government as prescribed by Section 10 of the Local Government Act 2002. That

purpose is to meet the current and future needs of communities for good quality

local infrastructure, local public services, and performance of regulatory

functions in a way that is most cost–effective for households and

businesses. Good quality means infrastructure, services and performance that

are efficient and effective and appropriate to present and anticipated future

circumstances.

1.6 The

objective of this decision relevant to the purpose of Local Government is:

Regulatory

functions which help to prevent harm and help create a safe and healthy

environment for people, which promote the best use of natural resources and

which are responsive to community needs.

1.7 This report

concludes by informing the Council that the submissions and further submissions

process for Variation 6 to the Proposed District Plan – Heritage Section

Amendments have now closed. One submission in support was received from

Heritage New Zealand Pouhere Taonga (HNZPT) and no further submissions have

been received. Therefore, in this case, there is no need to hold a hearing on

this matter. As a result, the amendments to the District Plan outlined in

Variation 6, as notified, can be adopted without amendment following the

acceptance by Council of the submission of HNZPT.

2.0 BACKGROUND

2.1 Vidal House (291 Te Mata Road) has been

requested to be included in Appendix 49 Heritage Buildings within the Te Mata

Special Character Zone by current owners Mr W and Mrs J Bradshaw.

Accompanying this request is a heritage assessment report prepared by Graham

Linwood (Architect) and reviewed by Chris Cochrane (Conservation

Architect). This report confirms that Vidal House meets the criteria for

inclusion as a heritage item in the District Plan for its architectural, social

and historical value. The listing of Vidal House is also supported by Heritage

New Zealand.

2.2 The request by Mr and Mrs Bradshaw has arisen out

of the resolution to an appeal to the Proposed District Plan by the Bradshaws

in relation to the provisions of the Te Mata Special Character Zone (which is

the zone in which the house and land at 291 Te Mata Road is located).

2.3 As part of the resolution of this Appeal, the

provisions of the Te Mata Special Character Zone were amended by consent order

dated 12 December 2016. In summary the changes that were made to the

Proposed District Plan as a result of this consent order sought to allow

commercial activities to be established within Heritage buildings and for these

to be exempt from any commercial activity threshold or cumulative site

threshold limits. The rules also state that where a site is occupied by a

heritage building used for commercial purposes and has a minimum area of 5000m2,

one residential building shall be allowed per site.

2.4 In

considering the above request officers became aware of the current non –

complying activity status of internal alterations (including internal safety

alterations) to heritage buildings within the Te Mata Special Character Zone

(Appendix 49). Further evaluation and assessment resulted in the

conclusion that this activity status was not intentional and warranted

correction. Therefore this matter is also included in within

proposed Variation 6.

3.0 CURRENT

SITUATION

3.1 Variation 6 was publicly notified on 22nd November 2018

with submissions closing on 19th December 2018. An

advertisement was placed in the public notices column of the Hawkes Bay Today

advising that submissions were now open on this Variation to the Proposed

District Plan. As part of the public notification process, letters were

sent to all property owners immediately adjoining 291 Te Mata Road as well as

all of the owners of heritage buildings within the Te Mata Special Character

Zone. These letters advised of the notification of the variation and

where information could be obtained and submissions lodged.

3.2 The Variation 6 documents and submission forms were made available

via the ‘my voice my choice’ website, the Hastings District Council

website (District Plan Variations page) and were available at the Customer

Service Centre and in the Hastings, Havelock North and Flaxmere libraries.

3.3 In total only one submission was received to the Variation.

This submission was in support of the Variation from Heritage New Zealand

Pouhere Taonga (HNZPT) and is attached for your reference.

3.4 In their submission HNZPT outlines that their organisation “supports

items being added to Heritage Schedules where they have been assessed as being

significant to the district and merit inclusion on a heritage schedule in the

District Plan”. Therefore HNZPT states that “consistent

with this approach HNZPT supports the proposed addition of Vidal House to

Appendix 49 – Heritage Buildings, Te Mata Special Character Zone, as this

recognises the significance of this heritage building to the District”.

3.5 HNZPT

also supports the provision for internal alterations to heritage buildings

identified in Appendix 49 as a permitted activity as this would have the same

activity status as internal alterations of Category II Heritage items which are

listed in Appendix 48. HNZPT states in their submission that they “support

this approach given it would achieve consistency with the permitted activity

status for Category II buildings, and moreover with the overall policy

direction and rules framework which is based on relative significance”.

3.6 A

summary of the submissions received on Variation 6 was publicly notified on 19th

January 2019 with the advice that further submissions in support of, or

opposition to these original submissions could be made by 1 February

2019. Again this information was placed in the Hawkes Bay Today, on the

‘my voice my choice’ and Hastings District Council websites and in

the Customer Services Centre, and Hastings, Havelock North and Flaxmere

libraries. Furthermore letters outlining this information were again sent

to those persons that were directly notified of Variation 6 originally.

3.7 No

further submissions have been received in respect of Variation 6 –

Heritage Section Amendments.

3.8 Therefore

given that the only submission received to this Variation is in complete

support of the amendments to the Proposed District Plan outlined in the

variation, it is not necessary to hold a hearing on this matter.

3.9 As

such the amendments to Section 18.1 and Appendix 49 of the Proposed District

Plan and Planning Maps 13, 47, 106 and 107 can be adopted by Council without

amendment.

3.10 Council

officers will ensure that EPlan, and any relevant Planning, GIS or LIM maps are

updated accordingly and will convey to the submitter, HNZPT, that a hearing is

not needed and that the changes outlined in Variation 6, as notified, can now

be adopted without amendment.

|

4.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Senior Environmental Planner (Policy) titled “Variation

6 to the Proposed District Plan - Heritage Section Amendments”

dated 21/02/2019 be received.

B) That

the submission from Heritage New Zealand Pouhere Taonga supporting

the listing of Vidal House (291 Te Mata Road) as a heritage

item and making provision for internal alterations to heritage

buildings in Appendix 49 as a

permitted activity in the Proposed District

Plan, be accepted through the adoption

of Variation 6 without

amendment.

C) That

the decision and notification process set down under the First Schedule

to the Resource Management Act 1991 be undertaken for Variation

6.

With the reason for this decision

being that the objective of the decision will contribute to meeting the

current and future needs of communities for performance of regulatory

functions in a way that is most cost-effective for households and business by:

i) The adoption of variation 6 without amendment will provide for the

sustainable management of the physical resources of the district.

ii) Amending the Proposed District Plan accordingly without the need

to hold a hearing on the matters outlined in Variation 6 – Heritage

Section Amendments.

|

Attachments:

|

1

|

HNZPT submission - Variation 6 to Hastings Proposed

District Plan

|

ENV-9-19-8-19-20

|

|

|

HNZPT submission - Variation 6 to

Hastings Proposed District Plan

|

Attachment 1

|

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Chief Financial Officer

Bruce

Allan

SUBJECT: Monthly

Financial Report - January 2019

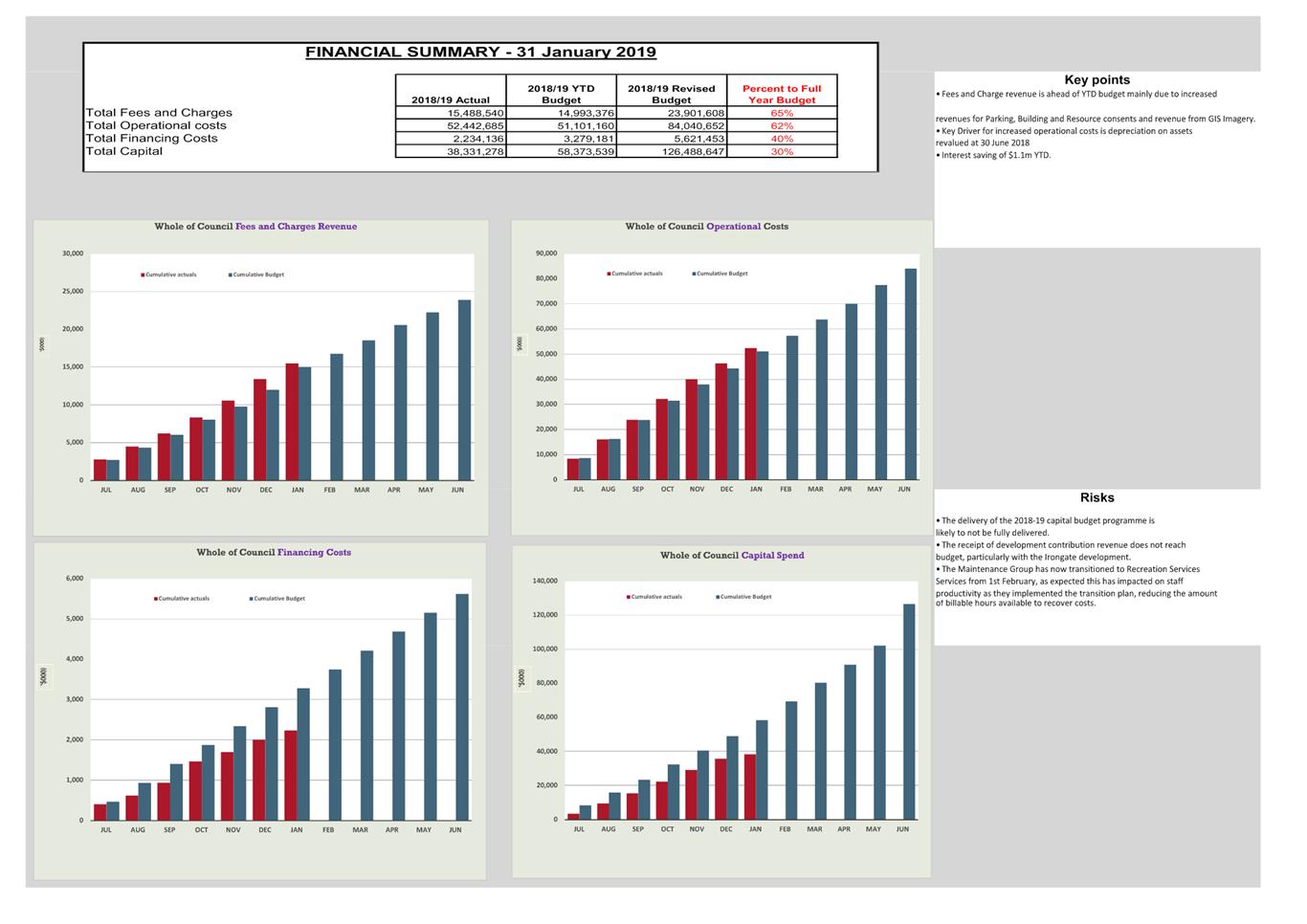

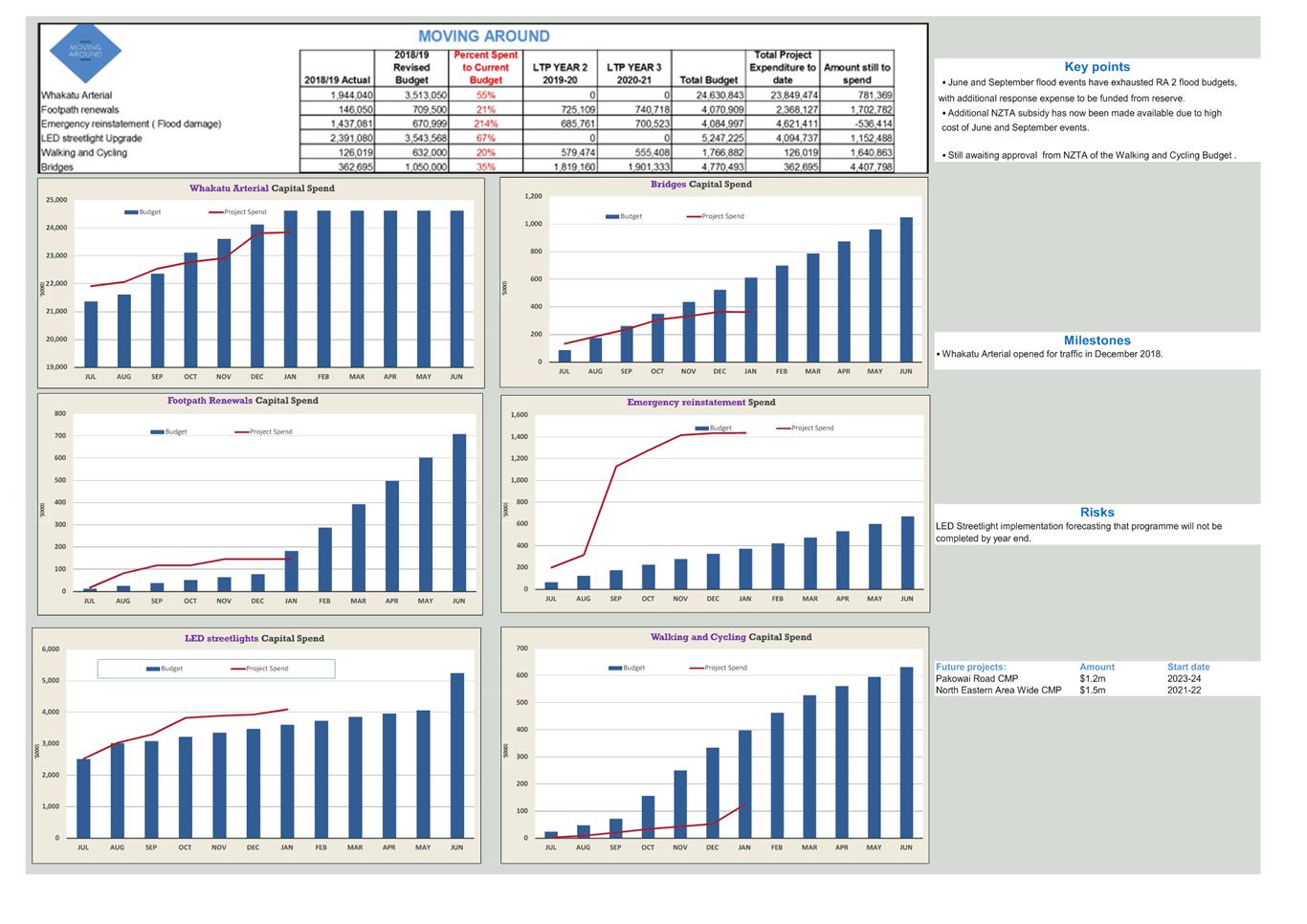

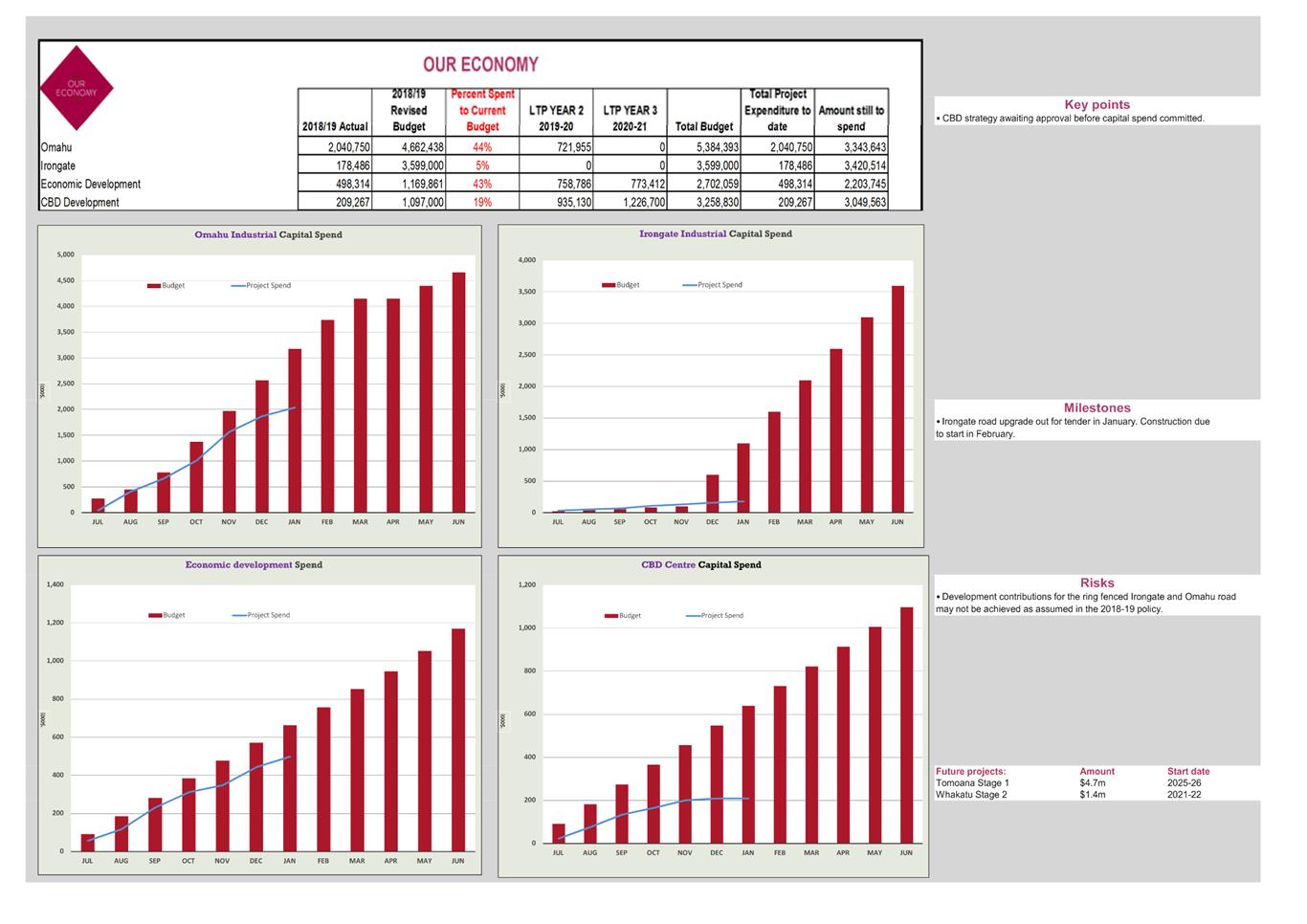

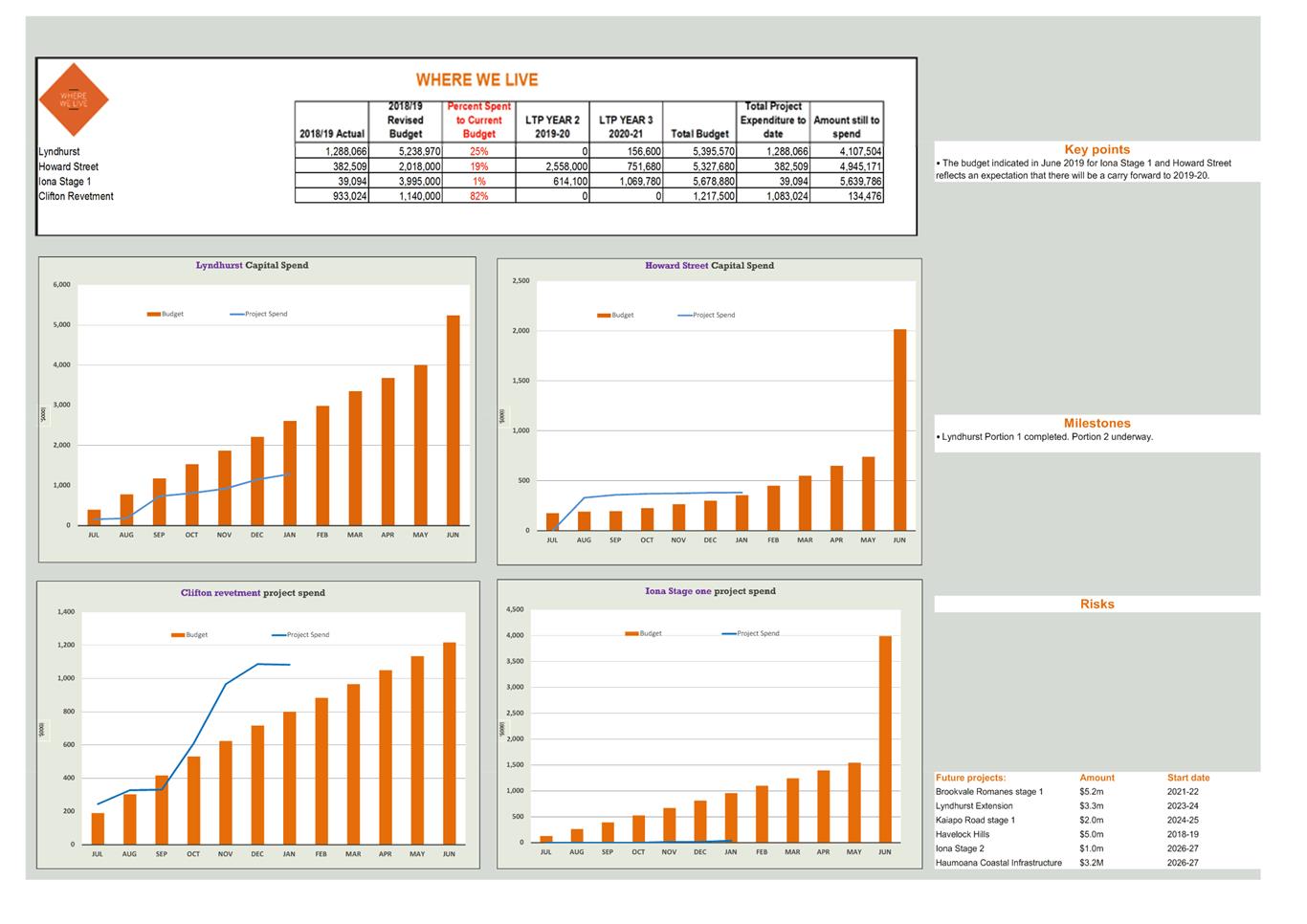

1.0 INTRODUCTION

1.1 Attached

as Attachment 1 is the monthly financial report year to date January

2019.

1.2 The

report provides Council with a direct link back to the Long Term Plan. The

strategic framework of the 2018-28 Long Term Plan has 6 broad areas of focus

and this new report is designed to link back to those 6 areas of focus which

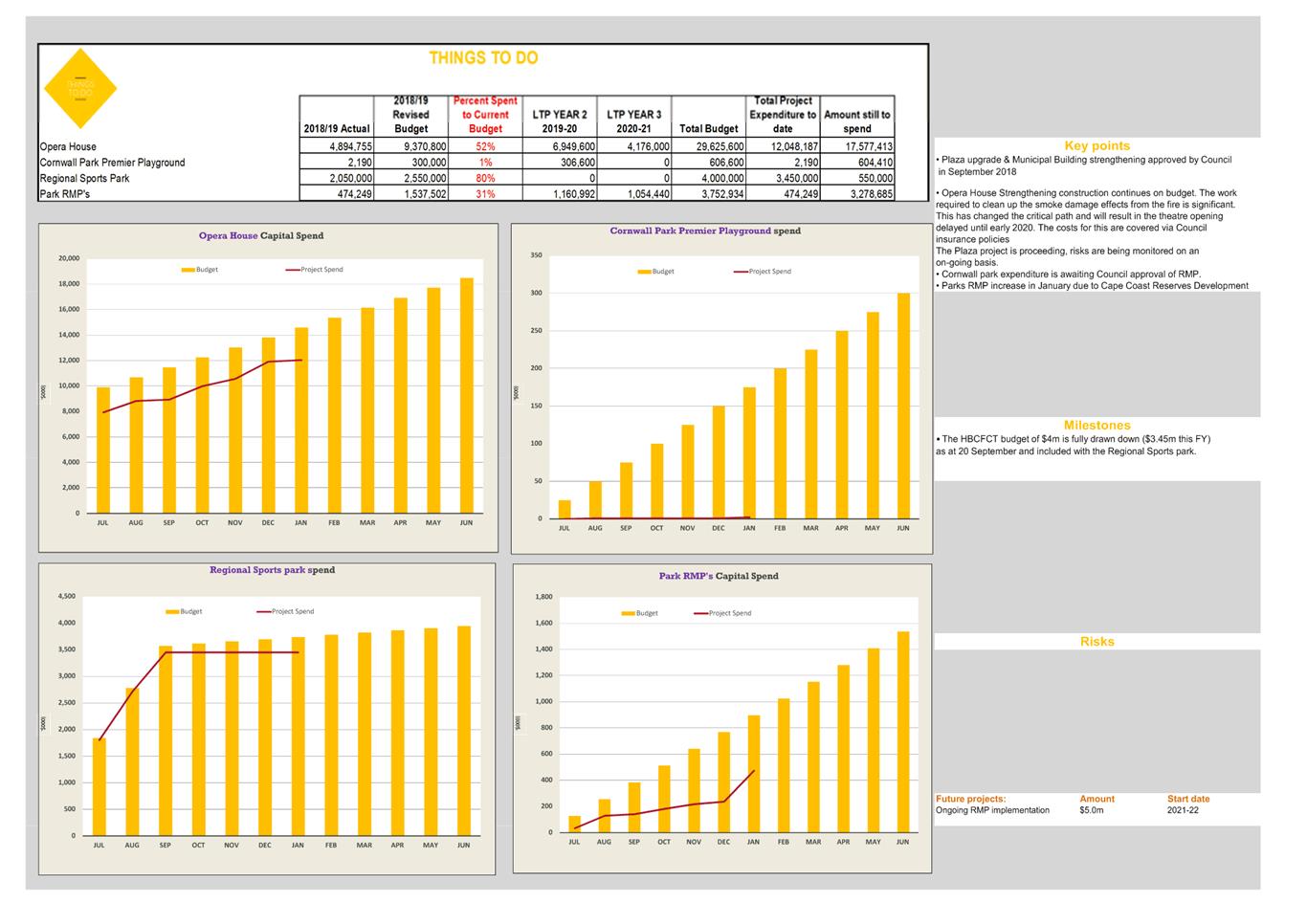

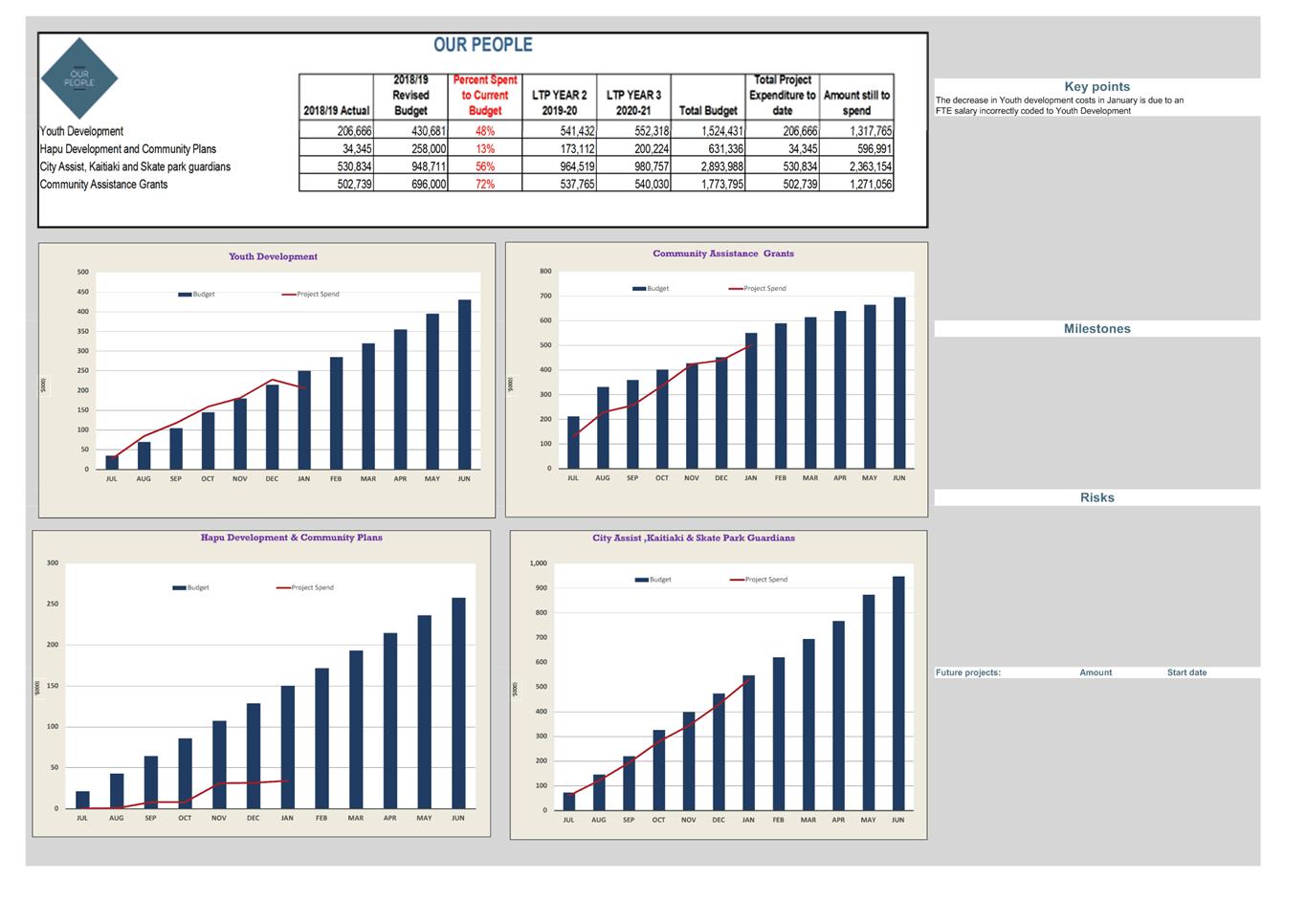

are:

1. Our Environment

2. Moving Around

3. Our Economy

4. Where we Live

5. Things to Do

6. Our People

1.3 The

one page report on each area of focus concentrates on a programme of work

rather than individual projects with each graph focussing on the current year

expenditure. Included in the right hand column are some high level commentary.

It is important to note that the scale of each programme of work varies

significantly and this needs to be considered when analysing the impact of any

programme spend against budget.

|

2.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Chief Financial Officer titled “Monthly

Financial Report - January 2019” dated 21/02/2019

be received.

|

Attachments:

|

1

|

Financial Summary

|

FIN-09-3-19-307

|

|

|

Financial Summary

|

Attachment 1

|

|

Financial Summary

|

Attachment 1

|

|

Financial Summary

|

Attachment 1

|

|

Financial Summary

|

Attachment 1

|

|

Financial Summary

|

Attachment 1

|

|

Financial Summary

|

Attachment 1

|

|

Financial Summary

|

Attachment 1

|

REPORT TO: Council

MEETING DATE: Thursday 21

February 2019

FROM: Health and Safety Manager

Jennie

Kuzman

SUBJECT: Health

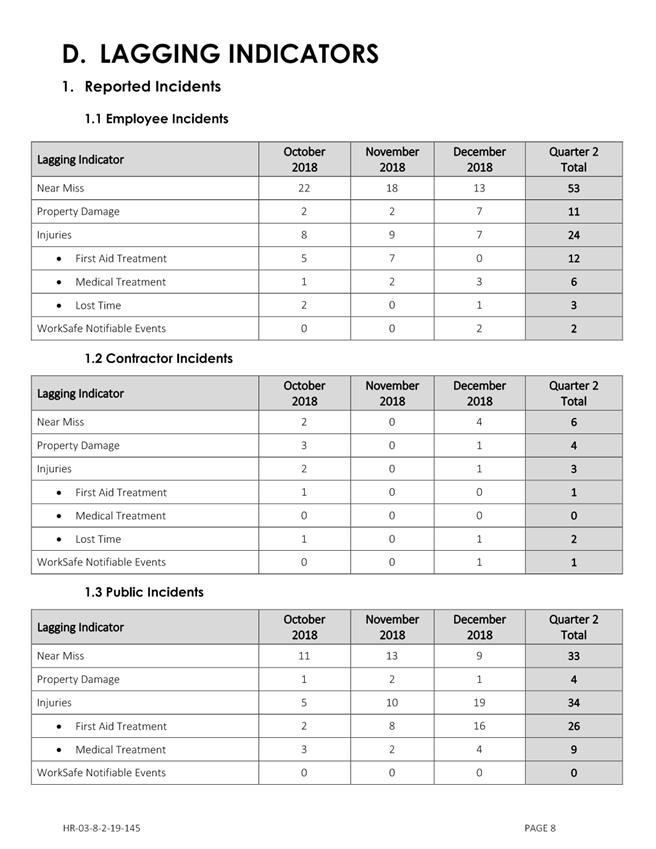

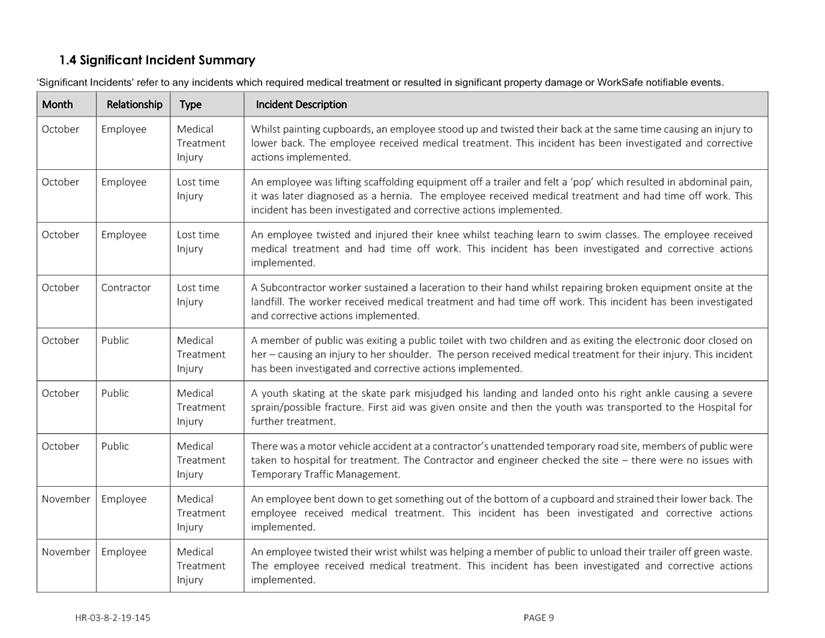

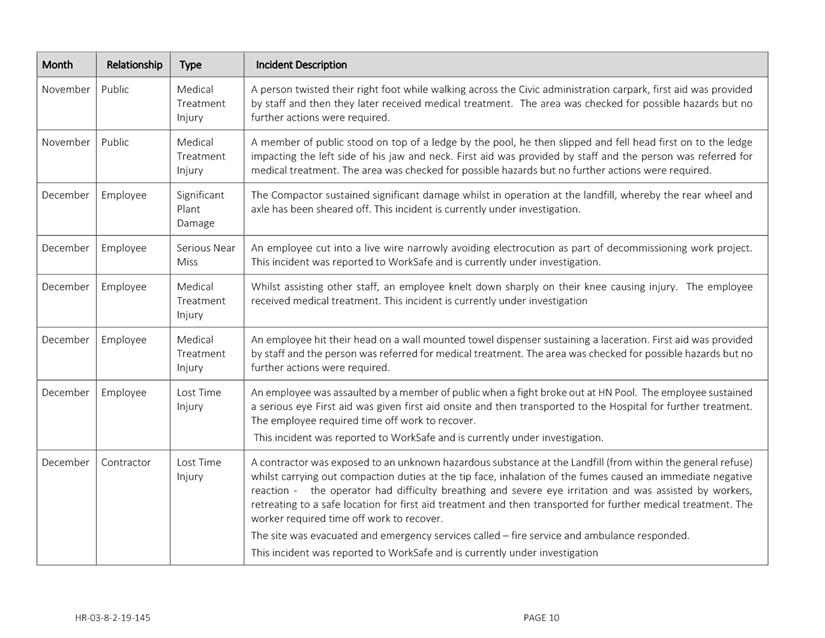

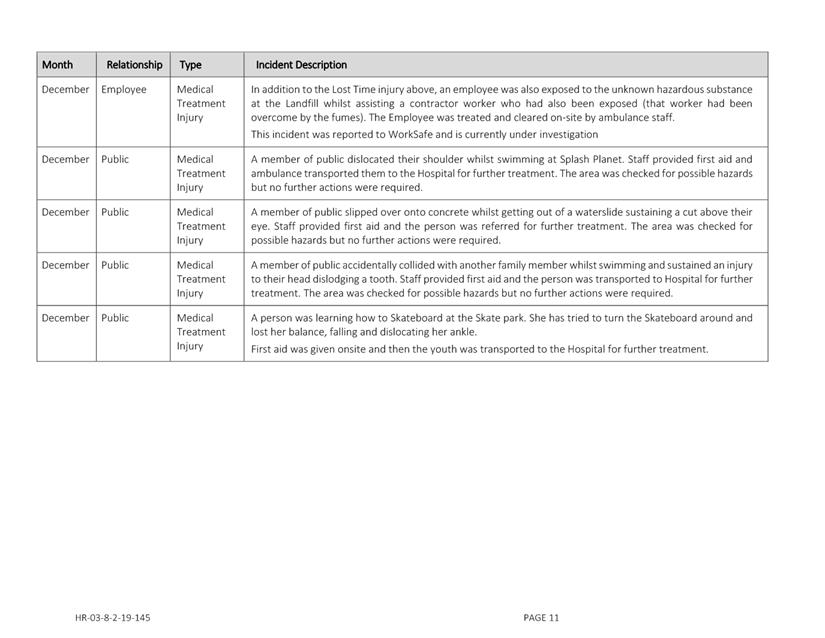

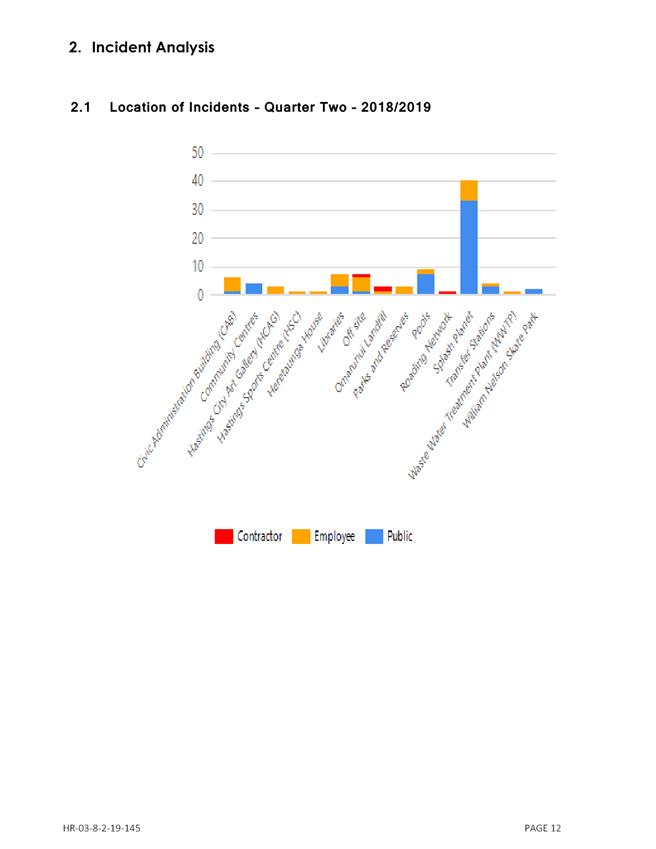

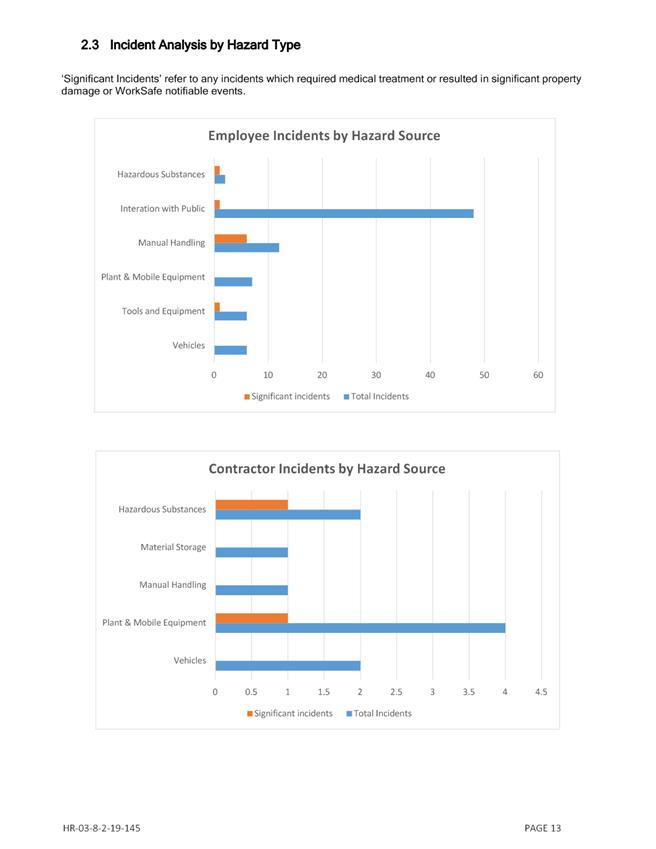

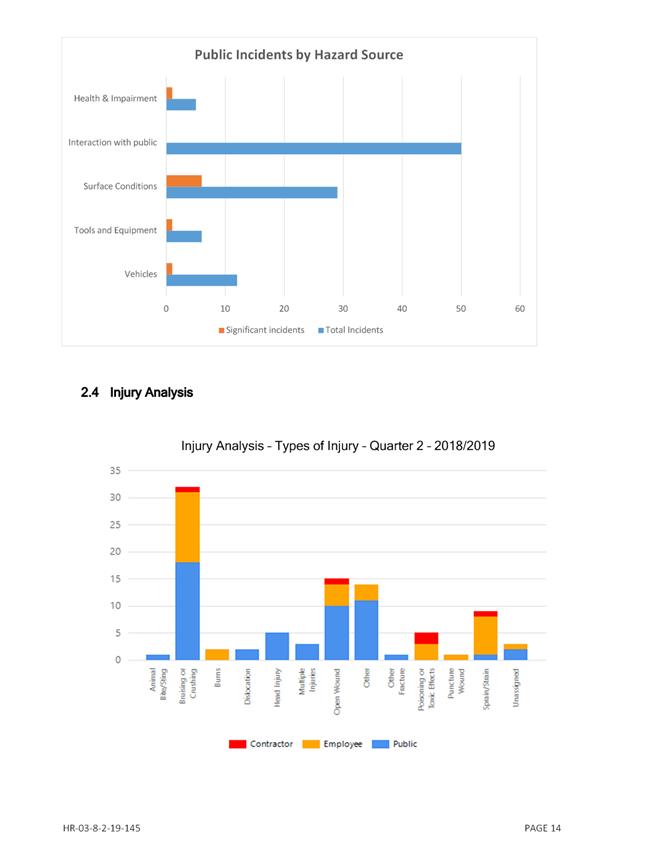

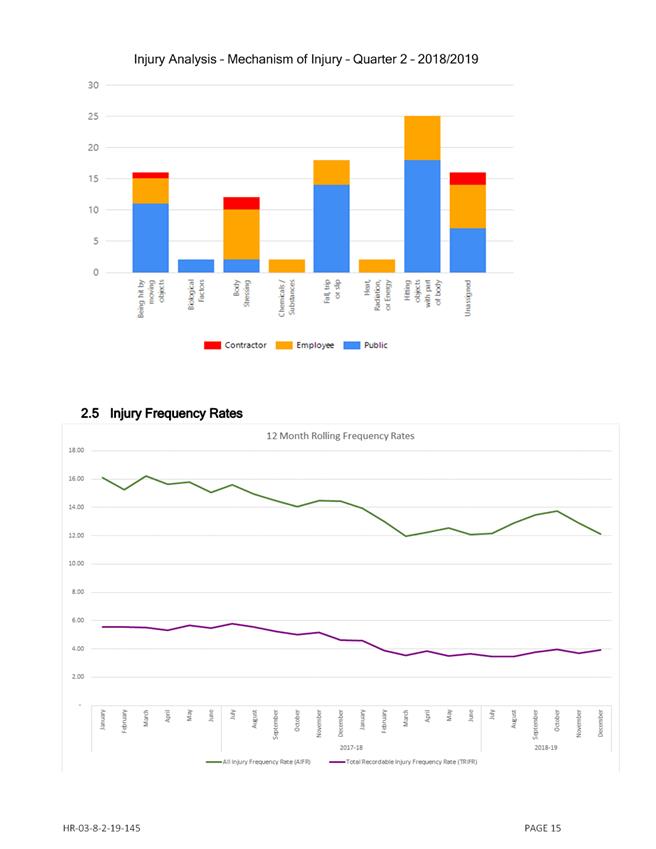

& Safety Quarterly Report

1.0 SUMMARY

1.1 The

purpose of this report is to inform and update Council

about Health and Safety at Hastings District Council.

1.2 The

report provides information to enable Elected Members to undertake due

diligence, by providing leading and lagging statistical information in relation

to Health and Safety for the second quarter of the 2018/2019 financial year

(covering the period 1 October to 31 December 2018).

1.3 This

quarterly report also incorporates the monthly report information for the

period 1-31 December 2018.

2.0 BACKGROUND

2.1 The

Health and Safety at Work Act 2015 (HSWA) requires HSWA Officers (Elected

members and the Chief Executive) to exercise due diligence by taking reasonable

steps to understand the organisation’s operations and Health and Safety

risks, and to ensure that they are managed so that Council meets its legal

obligations.

3.0 CURRENT

SITUATION

3.1 The

attached report for the second quarter of the 2018/2019 financial year (Attachment

1) provides information on leading and lagging statistical information in

relation to health and safety reporting for the period of 1 October to 31

December 2018. Detailed commentary has been provided within the attached report

in relation to Health and Safety performance for the second quarter of the

2018/2019 financial year.

3.2 As

discussed within the attachment, the format of the quarterly reports going

forward will be changed to accommodate the changes in personnel and risk

profile with the movement of Maintenance Group staff to Recreational Services

and to accommodate the organisational Health and Safety objectives.

3.3 The Health

& Safety quarterly report for the third quarter of the 2018/2019 will be

provided in the updated format to Council for the meeting being held on 2nd May

2019.

3.4 At

the Council meeting held on 31 January 2019, Elected members enquired as to the

number of visitors/public accessing Council facilities, the following table is

a summary of visitor numbers for the second quarter of the 2018/2019 financial

year.

|

Council

Facility

|

Number

of visitors for the period 1 October to 31 December 2018

|

|

Camberley

Community Centre

|

3,930

|

|

Clive

Pool

|

9,768

|

|

Flaxmere

Community Centre

|

approx. 10,000

|

|

Flaxmere

Waterworld

|

9,770

|

|

Frimley

Pool

|

4,844

|

|

Hastings

City Art Gallery

|

3,529

|

|

Hastings

District Libraries:

· Flaxmere

· Hastings

· Havelock North

|

30,299

81,760

28,938

|

|

Hastings

Sports Centre

|

13,200

|

|

Havelock

North Village Pool

|

6,587

|

|

Splash

Planet

|

39,459

|

3.5 Additionally,

at the same Council meeting, elected members enquired as to Council’s

critical Health and Safety risks and the control measures in place to mitigate

those risks. A copy of the report provided to the Risk and Audit subcommittee

on 5th November 2018 regarding these has been made available to elected members

on the Hub.

4.0 SIGNIFICANCE

AND ENGAGEMENT

4.1 This

Report does not trigger Council’s Significance and Engagement Policy and

no consultation is required.

|

5.0 RECOMMENDATIONS

AND REASONS

A) That

the report of the Health and Safety Manager titled “Health

& Safety Quarterly Report” dated 21/02/2019 be

received.

|

Attachments:

|

1

|

Human Resources (NO PERSONAL INFORMATION) - Health

and Safety - Injury Reporting & Recording - Information - Health and

Safety Manager's Health and Safety Report to Council - Quarter 2 2018/2019

|

HR-03-8-2-19-145

|

|

|

Human Resources (NO PERSONAL

INFORMATION) - Health and Safety - Injury Reporting & Recording -

Information - Health and Safety Manager's Health and Safety Report to Council

- Quarter 2 2018/2019

|

Attachment 1

|

|

Human Resources (NO PERSONAL

INFORMATION) - Health and Safety - Injury Reporting & Recording -

Information - Health and Safety Manager's Health and Safety Report to Council

- Quarter 2 2018/2019

|

Attachment 1

|

|

Human Resources (NO PERSONAL

INFORMATION) - Health and Safety - Injury Reporting & Recording -