Kaupapataka

Agenda

|

Te Rā Hui:

Meeting date:

|

Monday, 18 July 2022

|

|

Te Wā:

Time:

|

1.00pm

|

|

Te Wāhi:

Venue:

|

Council Chamber

Ground Floor

Civic Administration

Building

Lyndon Road East

Hastings

|

|

Te Hoapā:

Contact:

|

Democracy

and Governance Services

P: 06 871 5000

| E: democracy@hdc.govt.nz

|

|

Te Āpiha Matua:

Responsible Officer:

|

Group Manager: Corporate - Bruce Allan

|

Risk and Assurance Subcommittee

– Terms of Reference

Fields of Activity

The Risk and Assurance Committee is

responsible for assisting Council in its general overview of financial

management, risk management and internal control systems that provide;

·

Effective management of potential risks,

opportunities and adverse effects.

·

Reasonable assurance as to the integrity and

reliability of the financial reporting of Council.

·

Monitoring of Council’s requirements under

the Treasury Policy.

·

Monitoring of Councils Strategic Risk Framework.

Membership

• Membership

(7 including 4 Councillors).

• Independent

Chair appointed by Council.

• Deputy

Chair appointed by Council.

• 3

external independent members appointed by Council.

Quorum – 4 members

Delegated Powers

Authority to consider and

make recommendations on all matters detailed in the Fields of Activity and such

other matters referred to it by Council.

Kaupapataka

Agenda

|

Mematanga:

Membership:

|

Koromatua

Chair: Jon Nichols – External Independent

Appointee

Nga Kai Kaunihera

Councillors: Simon Nixon (Deputy Chair), Alwyn Corban,

Tania Kerr, and Geraldine Travers

Heretaunga Takoto Noa Māori Standing Committee appointee

: Robin Hape

External Independent Appointee: Jaun Park

Mayor Sandra Hazlehurst

|

|

Tokamatua:

Quorum:

|

4 members

|

|

Kaihokoe mo te Apiha

Officer Responsible:

|

Group Manager: Corporate

– Bruce Allan

|

|

Te Rōpū Manapori me te Kāwanatanga

Democracy & Governance Services:

|

Christine Hilton (Extn 5633)

|

Te Rārangi Take

Order of Business

|

1.0

|

Apologies

– Ngā

Whakapāhatanga

At the

close of the agenda no apologies had been received.

At the

close of the agenda no requests for leave of absence had been received.

|

|

|

2.0

|

Conflict

of Interest –

He Ngākau Kōnatunatu

Members need to be vigilant to stand aside from

decision-making when a conflict arises between their role as a Member of the

Council and any private or other external interest they might have.

This note is provided as a reminder to Members to scan the agenda and assess

their own private interests and identify where they may have a pecuniary or

other conflict of interest, or where there may be perceptions of conflict of

interest.

If a Member feels they do have a conflict of interest,

they should publicly declare that at the start of the relevant item of

business and withdraw from participating in the meeting. If a Member

thinks they may have a conflict of interest, they can seek advice from the

General Counsel or the Manager: Democracy and Governance (preferably before

the meeting).

It is noted that while Members can seek advice and

discuss these matters, the final decision as to whether a conflict exists

rests with the member.

|

|

|

3.0

|

Confirmation

of Minutes –

Te Whakamana i Ngā Miniti

Minutes of the

Risk and Assurance Committee Meeting held Monday 11 April 2022.

(Previously circulated)

|

|

|

4.0

|

GM

Corporate Update Report

|

7

|

|

5.0

|

Review

of Emerging Risks on Council's Strategic Goals

|

11

|

|

6.0

|

Risk

Assurance Update

|

19

|

|

7.0

|

GM

Assets Update Report

|

39

|

|

8.0

|

Health

and Safety Report: COVID-19 Response Update

|

41

|

|

9.0

|

Annual

Report 2022 Update

|

43

|

|

10.0

|

Treasury

Activity and Funding Update

|

47

|

|

11.0

|

Minor Items

– Ngā Take

Iti

|

|

|

12.0

|

Urgent

Items –

Ngā Take Whakahihiri

|

|

|

13.0

|

Recommendation

to Exclude the Public from Items 14, 15 and 16

|

53

|

|

14.0

|

Contractor

Health & Safety Performance Report

|

|

|

15.0

|

Flaxmere

Waterworld Roof Fire Incident - Summary of Findings

|

|

|

16.0

|

Regional

Aquatic Facility at the Mitre 10 Sports Park - Potential impacts on Hastings

District Council Aquatics Facilities

|

|

Hastings

District Council: Risk and Assurance Committee Meeting

Te Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Bruce Allan, Group

Manager: Corporate

|

|

Te Take:

Subject:

|

GM Corporate Update

Report

|

1.0 Purpose and summary - Te Kaupapa Me Te Whakarāpopototanga

1.1 Please note that

COVID has had an impact on staff preparing this agenda and as such some of the

reports are a little lighter on detail than expected. This detail will be

covered through verbal updates by staff at the meeting.

Internal Audit

Contract

1.2 The Internal Audit

contract with Crowe is at the end of its contracted terms following three years

with two one-year rights of renewals which have been utilised. Napier City

Council have lead the procurement process on behalf of the five Hawke’s

Bay councils. Officers may be able to provide the Committee with the outcome of

that procurement process at the meeting should it be sufficiently completed.

Cyber Security

1.3 Council continues to

implement both hard and soft controls to improve its security posture.

Recent Milestones

· Cybersecurity training completed by 81% of staff and

80% of Councillors. GMs and Mayor following up with anyone who has not

completed it.

· New backup and recovery infrastructure implemented

providing a plethora of recovery options.

· New next generation firewalls implemented replacing

five-year-old firewalls.

· Cybersecurity Incident Management System implemented.

This includes:

o A quick guide & full security incident management

guide

o Cybersecurity incident management policy

o Standard operating procedures for nine different

cybersecurity incident types / check lists

o Incident management plan

o Communication Strategy & Contacts list

· Project “Sandpit” scheduled for August

2022 to test Council’s incident management plan and restoration of

enterprise system (Technology 1 Finance)

· Received ALGIM 2021 Cybersecurity award.

Centre of Internet Security (CIS) controls - Officers

continue to work through the 281 CIS controls.

Insurance

1.4 AON have been engaged

by the five Hawke’s Bay councils to assess the potential Material Damage

(MD) loss due to the impact of seismic events on property assets owned by

member councils of the Group. This work will provide a high-level assessment of

potential MD losses to the HB Councils’ property assets due to earthquake

damage. The Group’s property portfolio predominantly includes buildings

(e.g., admin and civic buildings, community facilities etc.) and above-ground 3

Waters infrastructure assets (e.g., pumping stations, reservoirs etc.). The

analysis will focus on worst-case scenarios that could cause wide-spread damage

across the Hawke’s Bay region.

1.5 It is expected that

this loss modelling will inform Council’s decision making in terms of

setting loss limits rather than the current approach of having all assets

insured.

1.6 Officers are also

reviewing the current asset schedule, identifying assets that would not be

replaced if they were to be damaged or destroyed. Assets in this category and

identified to date include:

1.7 Public Liability (PL)

& Professional Indemnity (PI) - London has applied a 23.8% increase due to

a deterioration in claims for the sector (those with claims do have a higher

increase), increasing the premiums to $143,883. PL & PI cover is provided

through Marsh.

|

2.0 Recommendations -

Ngā Tūtohunga

That the Risk

and Assurance Committee receive the report titled GM Corporate Update Report

dated 18 July 2022.

|

Attachments:

There are no attachments for this report.

Hastings

District Council: Risk and Assurance Committee Meeting

Te Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Regan Smith, Risk and

Corporate Services Manager

Steffi Bird, Risk

Assurance Advisor

|

|

Te Take:

Subject:

|

Review of Emerging Risks

on Council's Strategic Goals

|

1.0 Purpose and summary - Te Kaupapa Me Te Whakarāpopototanga

1.1 The purpose of this

report is to provide further context to the emerging risks reported at the Risk

and Assurance Committee meeting on 14 February 2022. This information is

provided to enable the Committee to fulfil its role of supporting Council to

effectively manage risk.

1.2 Based on this

information the Committee may wish to advise Council on additional steps that

can be taken to navigate the volatility in the current operating environment in

order to successfully deliver strategic outcomes.

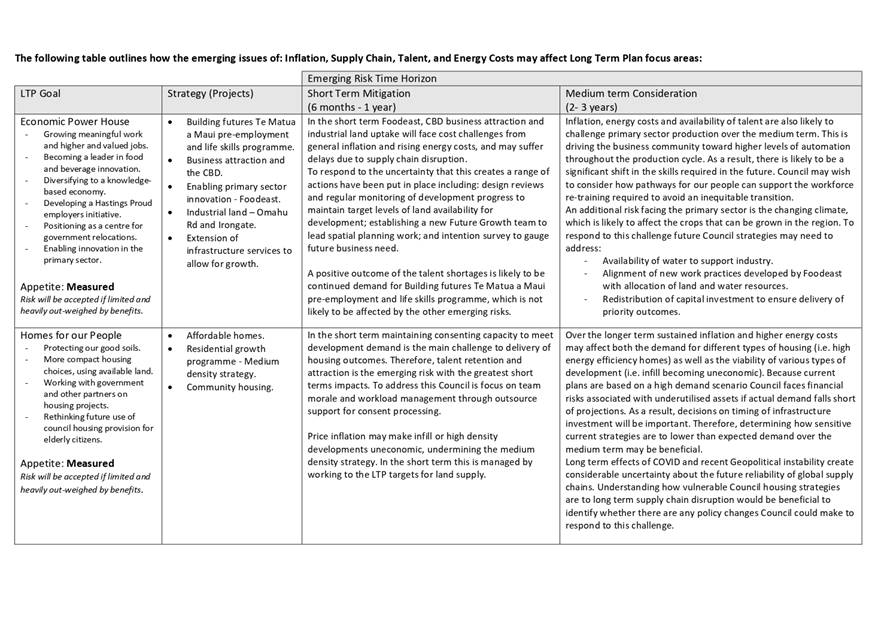

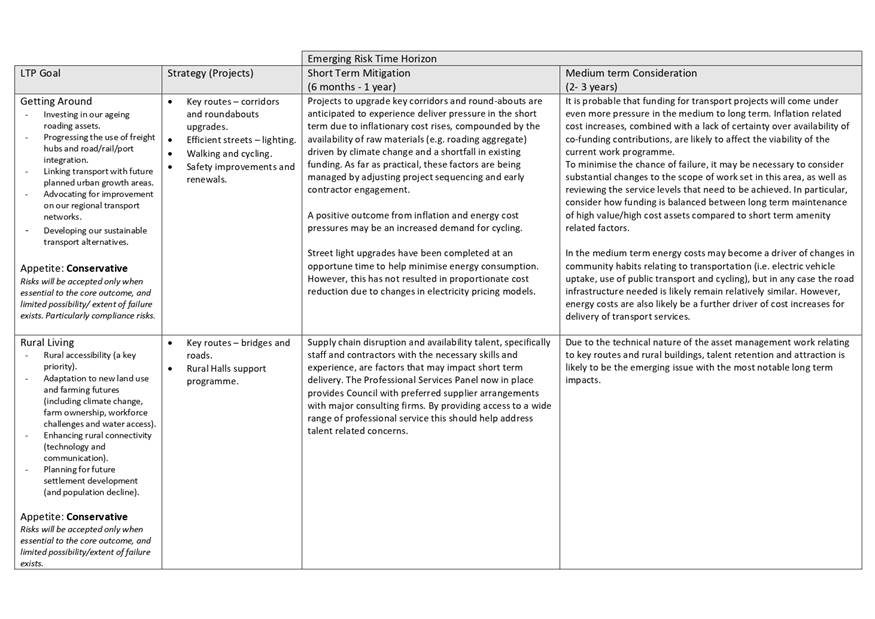

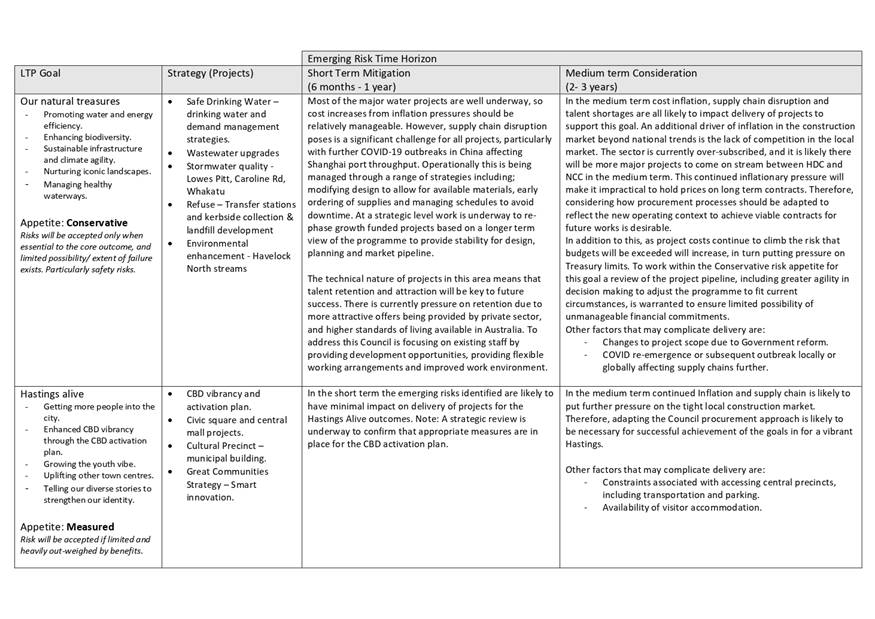

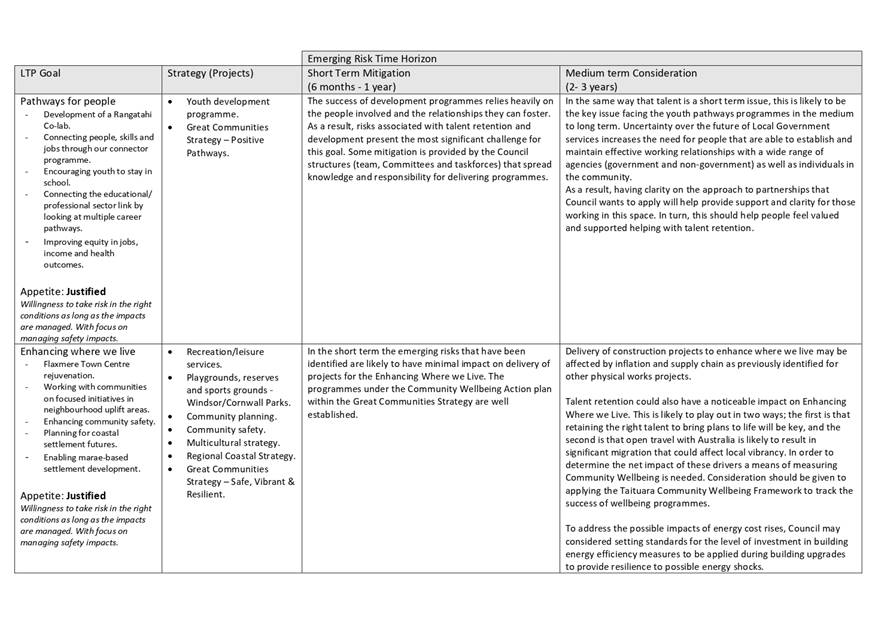

2.0 Emerging Risk Profile

2.1 The following four

emerging risks were previously identified as relevant to Council’s

strategic objectives:

· Inflation.

· Supply

chain disruption.

· Talent

attraction and retention.

· Energy

costs.

2.2 To assess the effect that

these emerging risks may have on Council’s Long Term Plan goals,

interviews were held with the relevant project owners. These discussions were

focused on two time horizons: A short term view covering current management

actions to respond to the emerging issues; and a medium term view that provides

a context for future strategic decision making.

2.3 By assessing the

effect of these emerging risks on Council’s strategy, it may be possible to

assess if the variation would be within Council’s risk appetite, and whether

Council should consider changes to the current projects to achieve strategic

goals.

2.4 The attached table (Attachment

1) lists a summary of the possible short and medium term effects of the

emerging risks on the current Long Term Plan focus areas. The key points from

this summary are:

Short term issues:

· Increased

management monitoring of key performance indicators to enable plans to be

adjusted as needed.

· Investment

in training & development of staff and provision of flexible working

arrangements to support talent retention and attraction.

· Early

contractor engagement, programme sequencing and product substitution to address

construction project impacts.

Medium term

issues:

· Undertaking

analysis to determine the sensitivity of existing policies to unexpected future

conditions (i.e. much lower than expected growth).

· Considering

there is a general trend toward higher cost for delivery of projects, it will

be important to critically review and prioritise projects to ensure key outcomes

are delivered while maintaining a sustainable project and financial workload.

This may also include reviewing service levels, including deciding on the

relative balance between core maintenance vs general amenity.

· Due

to the demand in the construction sector and constraints in supply chains,

consideration should be given to adapting procurement practices to enable more

innovation in the approach to contracting. In addition, reviewing delegations

to ensure the organisation has sufficient agility to adjust work programmes to

respond to immediate market conditions would be desirable.

· Developing

a strategy that leverages the capability of Foodeast to address potentially

significant changes in land and water use, as well as the need to up-skill the

workforce to match the greater level of automation in food production that is

likely in the next few years.

3.0 Climate Adaptation Risk

3.1 The following update

is provided on the basis that Failure of Climate Adaptation is currently the

top risk on Council’s strategic risk register.

3.2 The Government has

recently released two key policy documents that set the direction for the

response to climate change. Those documents are the National Adaptation Plan

and the Emissions Reduction Plan.

3.3 National Adaptation

Plan

3.4 The Government’s

first National Adaptation Plan (NAP) acknowledges that there are locked in

impacts of climate, regardless of any mitigating actions, and proposes actions

to help New Zealand adapt to these irreversible impacts. The NAP prioritises

actions for the next six years with the following vision, purpose and goals:

3.5 Vision: Our

people, places and systems are resilient and able to adapt to the effects of

unavoidable climate change in a fair, low-cost and ordered manner.

3.6 Purpose: To

enable New Zealanders to prepare for and adapt to the impacts of climate

change.

3.7 Goals:

3.7.1 Reduce

vulnerability to the impacts of climate change.

3.7.2 Enhance adaptive

capacity and consider climate change in decisions at all levels.

3.7.3 Strengthen

resilience to climate change.

3.8 HDC staff consider the

following risks to be a priority in regards to the draft NAP: water quantity

and quality (Strategic Risk #3), natural disaster resilience

(particularly land use planning) (Strategic Risk #1), ability to fund/financial

sustainability (Strategic Risk #9), drought, erosion and sea level rise

(HDC has significant assets in low-lying areas), extreme rainfall events, fuel

prices and other externalities, and the resources (human and financial)

required to adapt to Government policies.

3.9 The deadline for

submissions on the NAP closed on 3rd June. After reviewing the

situation Hastings District Council did not make an independent submission, but

was supportive of the Hawke’s Bay Regional Council views.

3.10 Emissions Reduction Plan

3.11 In addition to the NAP, the Government

released New Zealand’s first National Emissions Reduction Plan (ERP) during

May, which sets out how New Zealand will meet the Government’s first

emissions budget.

3.12 Key actions from the Emissions

Reduction Plan which have an impact on Local Government include:

· Transparency

and management of climate risks.

· Low-emissions

and resilient housing, and urban development.

· Financing

for infrastructure to support low-emission urban environments.

· Development

of a circular economy and bio-economy strategy.

· Improvements

and initiatives to increase the use of cycling (including e-bikes), walking,

electric vehicles and zero- or no-emission freight options.

· Improvements

in the Building and Construction sector to accelerate low-emissions buildings.

· Improvements

to both household and commercial waste management.

3.13 The actions within the ERP will require

Council to effect change in three distinct arenas:

3.13.1 Operating

Model: The way Council undertakes its activities will need to transition to a

low‑emissions profile (e.g. building energy efficiency and low/zero

emission transport). A carbon assessment of Council activities is underway to

develop a transition plan.

3.13.2 Core

Services Delivery: Many of the initiatives in the ERP will involve Council

giving effect to Government policy through statutory processes to drive a

change in community behaviour (e.g. land use planning and transportation system

changes). To be successful, Council will need to make the goals of the NAP and

actions from the ERP key deliverables of core Council services such as;

Environmental Planning, Resource Consenting, Building Consenting, Waste

Management, Transportation.

3.13.3 Community

Leadership: In order to achieve an orderly and equitable transition Council

will need to play a proactive leadership role to adapt to the changes affecting

our district and region. In this capacity, partnership with Maori/Iwi, local

and central Government agencies and community groups will be important, as will

be general community education.

3.14 To ensure HDC can respond effectively

to the actions within the ERP, an internal working group is being established.

The intention is to form a group of key representatives from the teams that are

impacted by the actions within the Plan.

|

4.0 Recommendations -

Ngā Tūtohunga

That the Risk

and Assurance Committee receive the report titled Review of Emerging Risks on

Council's Strategic Goals dated 18 July 2022.

|

Attachments:

|

1⇩

|

Impact of Emerging Risks on Council Objectives June 2022

|

PMD-9-3-22-50

|

|

|

Item 5 Review

of Emerging Risks on Council's Strategic Goals

|

|

Impact of

Emerging Risks on Council Objectives June 2022

|

Attachment 1

|

Hastings

District Council: Risk and Assurance Committee Meeting

Te Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Steffi Bird, Risk

Assurance Advisor

Elmien Steyn, Emergency

Readiness & Business Continuity Advisor

|

|

Te Take:

Subject:

|

Risk Assurance Update

|

1.0 Executive Summary

– Te Kaupapa Me Te

Whakarāpopototanga

1.1 This

report provides the Committee with an update on key risk assurance updates

since the last meeting, including:

· Approved

changes to the Tier 2 Enterprise risks

· Approved

Assurance Review Plan for 2022-2025

· Final

audit reports for Records Management and Community Grants Management from

Hastings District Council’s independent auditor, Crowe

· A

summary of actions from recent event and exercise debriefs

1.2 Tier 2 Enterprise

Risk Register Changes

· Through

a planned review, there has been a change to one of the risks managed by the

HDC Management Team.

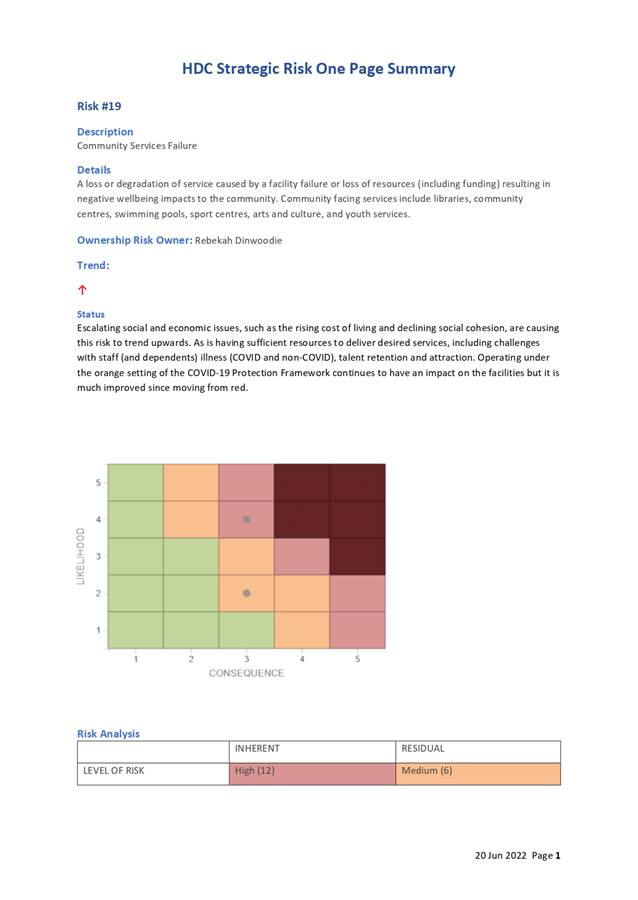

· Previously

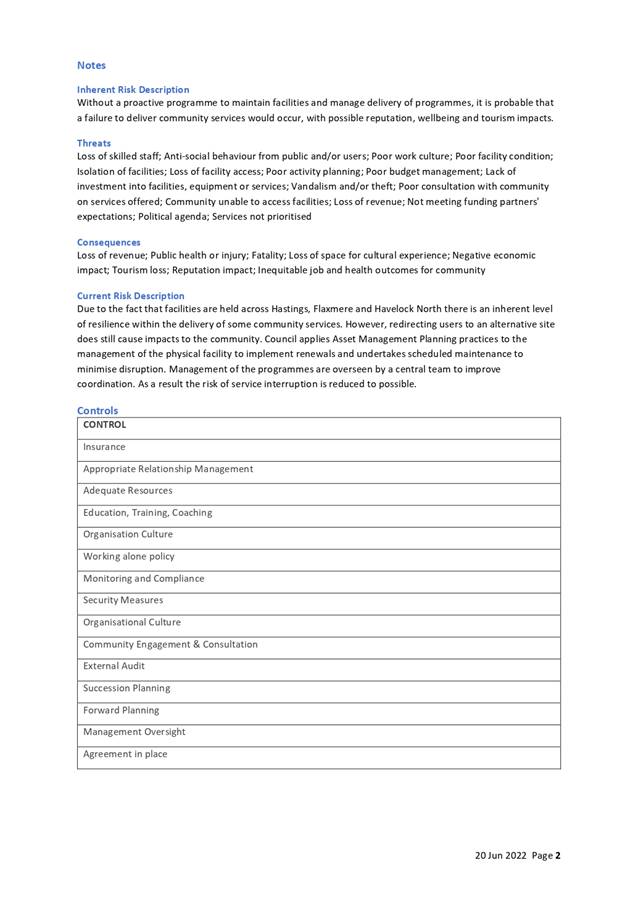

called ‘Facility Failure’, risk #19 has been reshaped to

‘Community Service Failure’ through a series of work between the

Risk Assurance Team and the Risk Owner, Group Manager: Community Wellbeing and

Services.

· The

risk profile now reflects the risk event (or tipping point) being a failure to

deliver services to the community, and failure of the facility is one of the

threats that could lead to this event.

· The

changes have been approved by the Lead Team and the new risk summary is

provided to the Committee for awareness (Attachment 1).

· This

risk is one of the enterprise risks which aggregates into the Tier 1 Strategic

Risk, ‘Significant Operational Service Failure’ owned by Council.

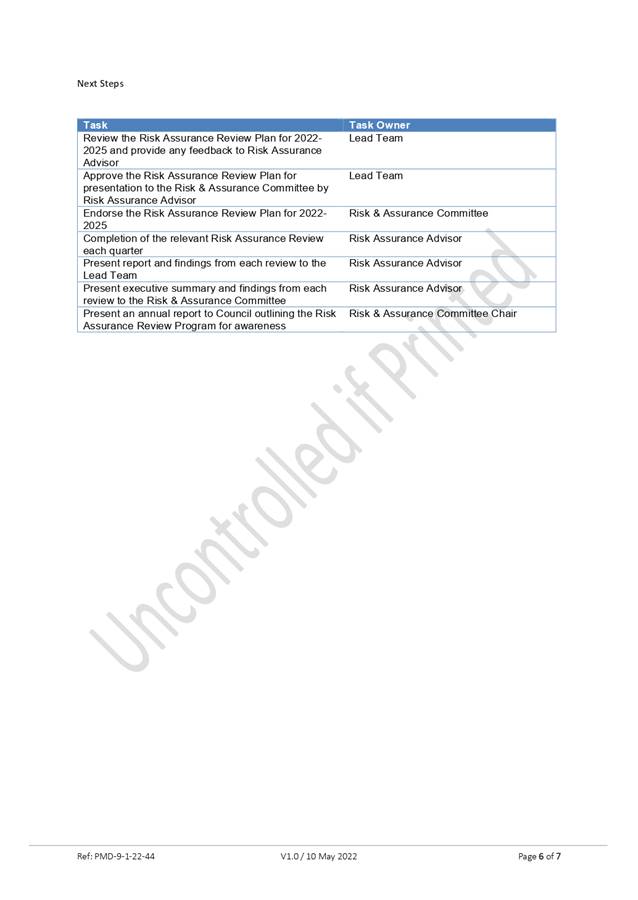

1.3 Assurance Review

Plan 2022-25

· The

Assurance Review Plan 2022-2025 (Attachment 2) has been developed by the

Risk Assurance Advisor and approved by the Lead Team.

· Based

on prior discussion, the review plan is focused on providing assurance over the

Tier 2 Enterprise risks.

· The

below reviews have been prioritised for completion. These will be undertaken by

the Risk Assurance function and an executive report provided back to the

Committee at completion:

o Environmental,

Social & Governance Review

o Fraud

& Corruption Incidents

o Man-made/natural

disaster

1.4 Records Management

& Community Grants Management Audit Report (undertaken by Crowe)

· Crowe,

HDC’s externally appointed, internal auditor, have undertaken Records

Management and Community Grants Management audits for HDC.

· The

Community Grants Management audit was based upon good practice guidance

from the Office of the Auditor General which resulted in three findings (one

rated low, and two rated moderate) and three subsequent recommendations.

|

Recommendation

|

Rating

|

|

As per the

OAG’s guide, the Council should ensure clear policies and procedures

are in place for identifying the purpose and criteria of the grants that the

Council will fund and the procedures that will be followed in ensuring the

council’s policy aims are effectively met.

Additionally, there

should be clear policies and procedures in place to ensure that public

information on the availability of funds and processes for applying are

appropriately made available.

|

Moderate

|

|

As per the

OAG’s guideline the council should perform regular reporting,

monitoring and other checks to ensure compliance with the conditions of the

grant and assess whether future grant is to be released. There should also be

procedures in place enforcing penalties where conditions are not met.

Additionally, any

monitoring done for the purposes of publishing outcome information on the

website should also be tracked in Smarty Grants forming part of the acquittal

information.

|

Low

|

|

For transparency

purposes, when grant funding is awarded, including the Community Events

Grants, it should be ensured that the decision-making processes are

documented and retained. Where required, it should also be ensured that

decisions are made publicly available. The documentation should include (but

not be limited to):

• the full list of applicants

• details of the grants awarded

(including justification and amounts, if required)

• the individuals making the

decisions

• any conflicts of interest identified

and the steps taken to manage those conflicts.

|

Moderate

|

· The

Records Management Standard issued by Archives New Zealand was used as the

basis for the audit on HDC’s Records Management policies and

procedures. The audit resulted in eight findings against the Standard’s

20 requirements (one process improvement, two rated low, and five rated

medium), with seven recommendations.

|

Recommendation

|

Rating

|

|

It is recommended that the Council reviews the

Records Management Policy and related strategies and plans to ensure it

remains up to date.

It should be ensured that review dates for

policies are adhered to or that reviews are undertaken whenever significant

system changes or upgrades are implemented to ensure the policies remain

valid.

|

Low

|

|

Consideration could be given as to whether

the Project HPRM Requirements document used by 3 Waters could be implemented

wider across the major contracting departments to ensure all documents

required in HPRM are captured.

|

Process Improvement

|

|

The steps already identified to be

completed as part of the Draft Digital Preservation Strategy. Completion of

these steps will allow for the requirements for documents of high risk, high

value or both to be met.

|

Moderate

|

|

Departmental level operating procedures

should be documented to ensure all staff are aware of the information

management requirements and their responsibilities for information

management.

It should be ensured that these procedures

provide sufficient detail to ensure all staff are aware of the type of

information that should be retained, for how long and how it should be

disposed.

These details should include department

specific requirements as well as council-wide requirements (for example

emails giving advice or making decisions should be retained as opposed to

general emails which may not need to be kept).

The Executive Sponsor should ensure that

appropriate procedures have been documented across all departments that

manage records in systems other than HPRM.

|

Moderate

|

|

The Council should implement a process to

regularly assess or audit its information and records management practices to

demonstrate that its business rules, procedures and systems are operating

routinely. This could be performed in a form of a self-assessment, described

in 1.8.

Each department should be accountable to

ensure relevant policies and procedures are in place capturing the relevant

records management requirement.

The Executive Sponsor should be responsible

for overseeing these assurance activities and ensuring they take place.

|

Moderate

|

|

We note that the Draft Digital Preservation

Strategy includes the following goals:

· Infrastructure,

tools, standard policies and procedures for managing HDC's digital

information will be in place. HDC will promote the use of open format files

where practicable.

· Action plans for

managing and preserving digital information will be in place to assist HDC in

complying with the Archives New Zealand Information and Records Management

Standard 2016 and the Public Records Act 2005.

· Systems,

environments, tools and resources will be in place to ensure that digital

information as an asset is created, captured, accessible, has integrity and

is authentic throughout its lifecycle.

It should be ensured that the strategy

includes consideration of the data held on network drives and Microsoft Teams

files.

|

Moderate

|

· Final

reports have been discussed with the respective management of each area audited

and management actions agreed. Completion of actions is underway and will be

monitored to completion.

· An

executive summary of each of the final audit reports has been provided for the

Committee (Attachments 3 & 4).

1.5 Summary of Event

& Exercise Debrief Actions

· An

overview is provided to the Committee on the learnings identified from real

time responses, as well as from the business continuity exercises held between

August 2021 and March 2022, including:

o The

COVID-19 Delta variant outbreak lock down of 17 August to 7 September 2021;

o The

22 to 24 March 2022 rain event;

o Ex-Tropical

Cyclone Fili of 11 to 13 April 2022;

o COVID-19

Delta outbreak with the LT: Operation Falcon, 4 August 2021 (exercise);

o Active

shooter incident at Toitoi: Operation Cedric, 18 November 2021 (exercise);

o Tsunami

response for campgrounds (Evers-Swindell Reserve, Haumoana Domain & Clifton

Road Reserve): Operation Lilo, 4 March 2022 (exercise);

o Tsunami

response for the Clive Wastewater Treatment Plant: Operation Outfall, 10 March

2022 (exercise); and

o Tsunami

response at the Clive War Memorial Pool: Operation Freestyle, 11 March 2022

(exercise).

· Below

is an account of the key recommendations that were identified and a summary of

the actions still open:

|

EVENTS

|

|

TOTAL

|

CLOSED

|

OPEN

|

|

35

|

22

|

13

|

|

EXERCISES

|

|

TOTAL

|

CLOSED

|

OPEN

|

|

30

|

9

|

21

|

|

2.0 Recommendations -

Ngā Tūtohunga

That the Risk

and Assurance Committee receive the report titled Risk Assurance Update dated

18 July 2022.

|

Attachments:

|

1⇩

|

Strategic Risk Summary - Community Service Failure

|

PMD-9-3-22-53

|

|

|

2⇩

|

HDC Assurance Review Plan 2022-2025

|

PMD-9-3-22-55

|

|

|

3⇩

|

Audit Report for HDC Community Grants Management (Crowe)

|

PMD-9-3-22-56

|

|

|

4⇩

|

Audit Report for HDC Records Management (Crowe)

|

PMD-9-3-22-57

|

|

|

Item 6 Risk

Assurance Update

|

|

Strategic

Risk Summary - Community Service Failure

|

Attachment 1

|

|

Item 6 Risk Assurance

Update

|

|

HDC

Assurance Review Plan 2022-2025

|

Attachment 2

|

|

Item 6 Risk Assurance

Update

|

|

Audit

Report for HDC Community Grants Management (Crowe)

|

Attachment 3

|

|

Item 6 Risk Assurance

Update

|

|

Audit

Report for HDC Records Management (Crowe)

|

Attachment 4

|

Hastings

District Council: Risk and Assurance Committee Meeting

Te Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Craig Thew, Group

Manager: Asset Management

|

|

Te Take:

Subject:

|

GM Assets Update Report

|

1.0 Purpose and summary - Te Kaupapa Me Te Whakarāpopototanga

1.1 The Group Manager:

Assets update report will be presented as a verbal update for this meeting due

to a COVID inflicted interruption that has prevented a written report being

prepared.

1.2 The Group Manager:

Assets will also provide an update to the Committee on 3 Waters Reform.

|

2.0 Recommendations -

Ngā Tūtohunga

That the Risk

and Assurance Committee receive the report titled GM Assets Update Report

dated 18 July 2022.

|

Attachments:

There are no attachments for this report.

Hastings

District Council: Risk and Assurance Committee Meeting

Te Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Jennie Kuzman, Health

and Safety Manager

Bronwyn Bayliss, Group

Manager: People and Capability

|

|

Te Take:

Subject:

|

Health and Safety

Report: COVID-19 Response Update

|

1.0 Executive Summary

– Te Kaupapa Me Te

Whakarāpopototanga

1.1 The purpose of this

report is to provide an update to the Risk and Assurance Committee in regards

to the management of Health and Safety risks within Council.

1.2 This report provides

an update on Council’s COVID-19 Response.

|

2.0 Recommendations -

Ngā Tūtohunga

That the Risk

and Assurance Committee receive the report titled Health and Safety Report:

COVID-19 Response Update dated 18 July 2022.

|

3.0 Background – Te Horopaki

3.1 The

purpose of this report is to provide information to the Committee in regards to

the management of Health and Safety risks within Council.

3.2 This

issue arises due to the Health and Safety at Work Act 2015 and the requirement

of that legislation for Elected Members to exercise due diligence to ensure

that Council complies with its Health and Safety duties and obligations.

4.0 Discussion – Te Matapakitanga

4.1 COVID-19

response update

4.2 As

previously reported to the Committee at the February and April 2022 meetings,

the established COVID-19 Response team has been supporting the organisation

through its business continuity response and planning for any COVID-19. This

approach continues to work well and is providing a joined up organisation-wide

approach to managing the constantly changing environment.

4.3 Given

the fast moving and constantly changing environment that we are operating in a

verbal update will be provided to the Committee at the meeting, based on the

most up-to-date information at that time.

Attachments:

There are no attachments for this report.

Hastings

District Council: Risk and Assurance Committee Meeting

Te Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Jess Noiseux, Financial

Improvement Analyst

Aaron Wilson, Financial

Controller

|

|

Te Take:

Subject:

|

Annual Report 2022

Update

|

1.0 Purpose and summary - Te Kaupapa Me Te Whakarāpopototanga

1.1 The purpose of this

report is to update the Risk and Assurance Committee about progress being made

on year-end issues.

1.2 This report concludes

by recommending that the report be received.

2022 Annual Report

1.3 Staff have completed

the annual year end timetable for the 2022 year end. The timetable is inclusive

of all the processes and requirements of the production of the Annual report

and requires a high degree of coordination across Council. Normally the Local

Government Act stipulates that the Annual Report must be adopted by Council by

31st October each year. However the impact of Covid-19 resulted in

the Annual Reporting and Audit Time Frames Extensions Legislation Act 2021

which pushes the adoption date out to 31 December 2022.

1.4 To meet publishing

deadlines in time for the Christmas shut down period, this year the date set

for Council approval is 8th December. Other key dates for the audit

process are:

· Draft

financial statements available for Audit 23rd

September

· Full

Annual report available for Audit 23rd

September

· Summary

Annual Report available for Audit 23rd

September

· Final

Audit begins – audit on-site 31st

October

1.5 As was advised in the

GM Corporate’s update in April, Audit NZ have communicated that they will

not be able to complete the HDC 2022 Annual Report in time for the outgoing

Council to adopt the audited accounts before the election. The key dates

outlined above are reflective of Officers commitment to provide the completed

unaudited Annual Report for outgoing Councillors to endorse prior to the

election. The incoming Council will then be required to formally adopt the

audited 2022 Annual Report once they have been officially sworn in.

1.6 There are minor

amendments to the Public Benefit Entity (PBE) reporting standard PBE IPSAS 2 Cash

Flow Statement that Officers have assessed will result in added disclosures

required in the 2021/22 Annual Report. PBE IPSAS 40 PBE Combinations

also comes into effect, however Officers have assessed that this standard has

no impact on the presentation of Council’s financial statements.

1.7 Officers have chosen

to early adopt PBE IPSAS 41 Financial Instruments in line with our

accounting policy statement in the Long Term Plan 2021-31. The early adoption

of this accounting standard impacts on classification of financial assets and

how impairment on these financial assets is calculated. Council do not have

complex financial assets and the impact of this standard does not materially

affect the 2021/22 Annual Report.

1.8 Last year Council

received a qualified audit opinion over the activity groups’ statement

due to issues in two separate performance measures:

· Incomplete

information about the number of complaints Council received related to 3 waters

complaints. This was an issue across a number of councils in both the 2021 and

2020 financial years, partly due to the ambiguity in some of the guidance from

the Department of Internal Affairs (DIA) and how this was interpreted. In

August 2020, Council implemented a number of changes to resolve the issues

identified by Audit. However, Council is also reliant on Palmerston North City

Council’s system and processes for recording complaints received after

hours and limitations in this process resulted in another qualification in the

2021 Annual Report.

· Insufficient data

to reliably measure real water loss from the Council’s networked water

reticulation system. Council do not have sufficient water meters installed on

residential connection to report a statistically reliable water loss

percentage. Officers have been exploring using a different measurement

methodology (minimum nightly flow) that is allowable under the DIA framework.

If this method proves reliable and accurate, Council should be able to report a

reliable water loss percentage in the 2022 Annual Report.

1.9 Every year there are

revaluation of various classes of assets that are performed on a rotational

basis on a set schedule. This year it is the three water assets (water supply,

sewerage and wastewater) that will be revalued. These valuations are being

completed and are as at 30th June 2022.

2022 Audit Plan

1.10 In May Audit NZ provided their

finalised Audit Plan for the year. The Audit Plan outlines audit logistics,

specific areas of focus for Audit NZ and areas of potential risk for the

Council. A copy of the finalised plan is attached as Attachment 1. The

areas that Audit have identified in their Audit Plan as being areas of focus

are:

· Reporting on

mandatory performance measures;

· Revaluation of

three waters;

· Fair value

assessment of other asset classes (land and buildings, roading, and parks);

· Capital do-ability

and carry forward of projects;

· Accounting for

central government funding;

· Impact of three

waters reform;

· Configuration and

customisation costs for Software-as-a-service (SaaS);

· Covid-19 impact;

and

· Adoption of PBE

FRS 48 Service performance reporting.

Interim audit

1.11 Audit NZ were onsite during May and

June and have completed their interim audit. Due to the timing of this,

Officers have yet to receive an interim Management Report in time for inclusion

in this report. Audit have yet to provide a memo for this meeting advising of

key findings from their interim audit. A copy of this memo will be circulated

once it is received. Any recommendations or updates will be included and

reported on by Audit NZ during the final year-end audit process.

Covid-19 implications

1.12 We do not expect that year-end

reporting will need to articulate the impact of Covid-19 in a significant way

this year. Officers will work with Audit NZ to ensure disclosure (if any) is

sufficient for reporting purposes.

|

2.0 Recommendations -

Ngā Tūtohunga

That the Risk

and Assurance Committee receive the report titled Annual Report 2022 Update

dated 18 July 2022.

|

Attachments:

|

1⇨

|

Financial Management - Audit Plan for 2022 from Audit NZ

|

FIN-07-01-22-469

|

Under Separate Cover

|

Te

Hui o Te Kaunihera ā-Rohe o Heretaunga

Hastings

District Council: Risk and Assurance Committee Meeting

Te

Rārangi Take

Report to Risk and Assurance Committee

|

Nā:

From:

|

Aaron Wilson, Financial

Controller

|

|

Te Take:

Subject:

|

Treasury Activity and

Funding Update

|

1.0 Executive Summary – Te Kaupapa Me Te

Whakarāpopototanga

1.1 The

purpose of this report is to update the Risk and Assurance Committee on

treasury activity and funding issues.

1.2 Since

the last update in on the 11th April, Council has had one forward

start contract become “live” in replacing maturing debt of

$23m. In addition Council has in June 2022 borrowed $32m additional funds

to prefund 2022/23 capital expenditure and in July 2022 has entered into

another forward start contract for $21m for debt maturing in April 2023.

1.3 The

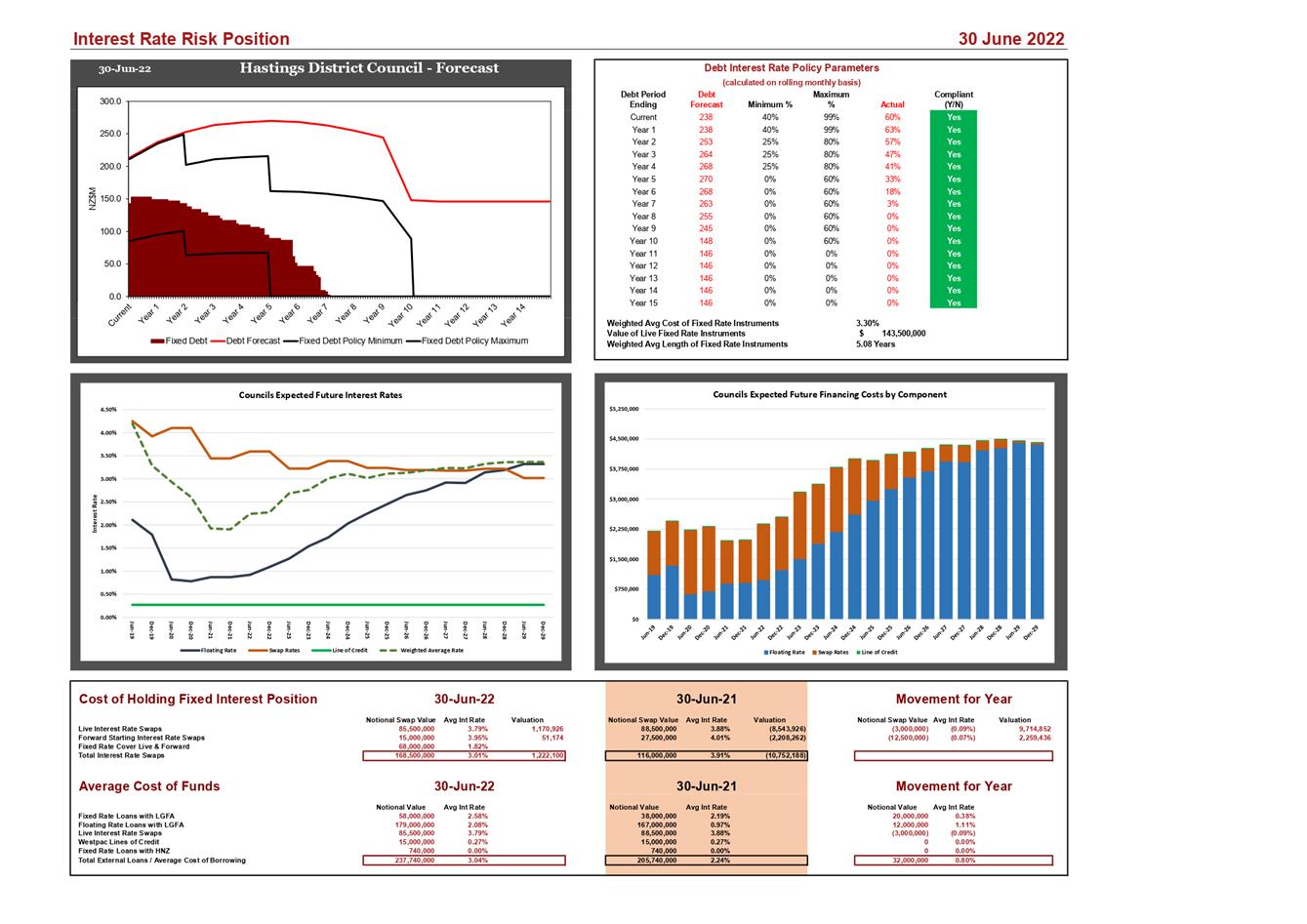

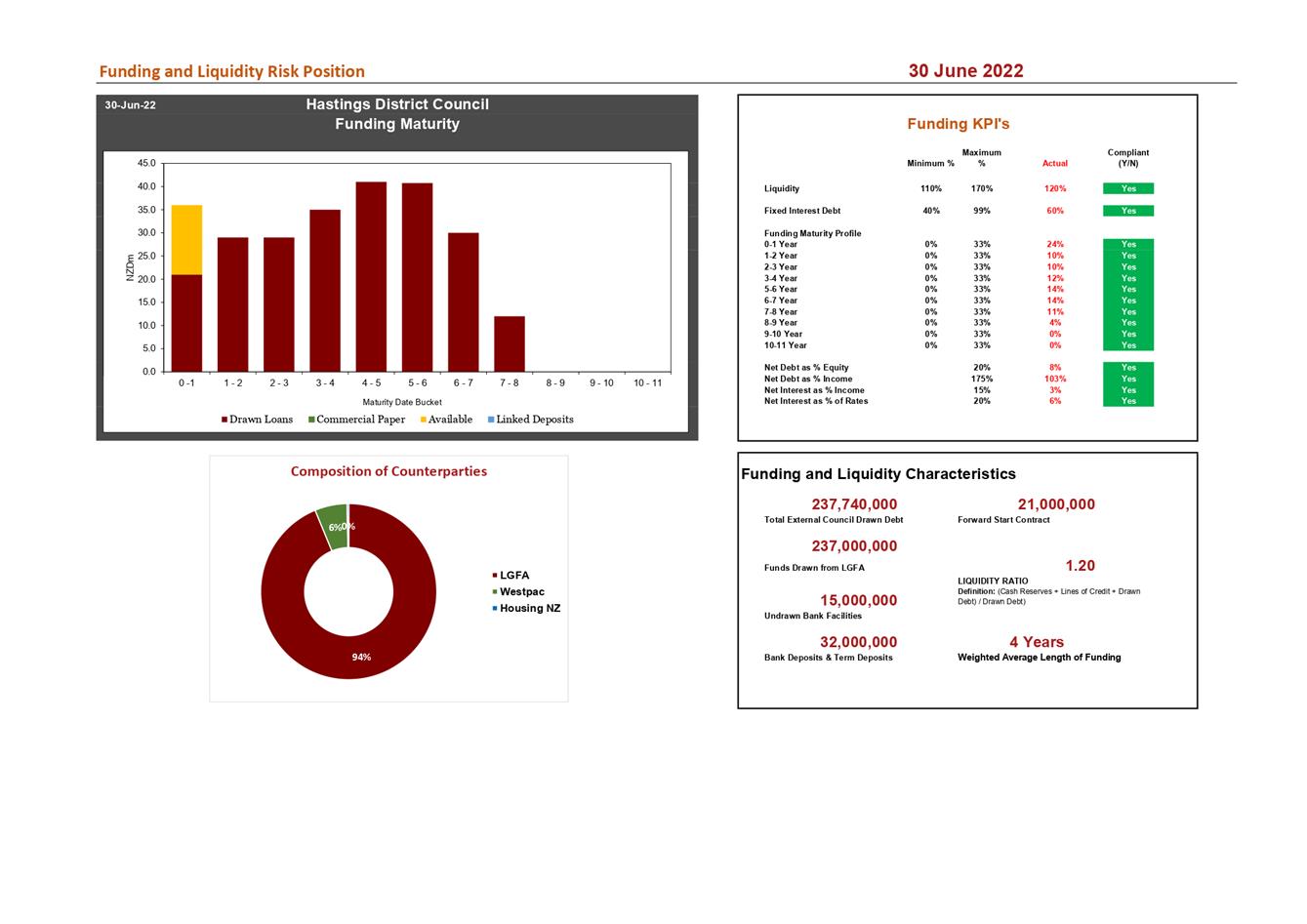

Council’s current total external debt is $237m as at 30th June 2022.

Offsetting this is $32m of bank deposits, giving a net external debt position

of $205m.

1.4 Council

is currently compliant with its Treasury Management Policy.

The Reserve Bank of

New Zealand (RBNZ) raised its Official Cash Rate (OCR) to 2.0% at its last

review in May 2022.

|

2.0 Recommendations - Ngā Tūtohunga

A) That

the Risk and Assurance Committee receive the report titled Treasury Activity

and Funding Update dated 18 July 2022.

B) That

the Committee endorse the recommended changes to the Treasury Policy as

reviewed by council officers and outlined in the report in A) above.

|

3.0 Background – Te Horopaki

3.1 The

Hastings District Council has a Treasury Policy which is a summarised version

of the Treasury Management Policy and forms part of the 2021-2031 Long Term

Plan. Under these policy documents, responsibility for monitoring treasury

activity is delegated to the Risk and Assurance Committee.

3.2 Council

is provided with independent treasury advice by Miles O’Connor of Bancorp

Treasury Services and receives daily and monthly updates on market conditions.

3.3 Under

the Treasury Policy, formal reporting to Council occurs quarterly and regular

more in-depth treasury reporting is provided for the Risk and Assurance

Committee.

4.0 Discussion – Te Matapakitanga

4.1 Council’s

debt portfolio is managed within macro limits set out in the Treasury Policy.

It is recognised that from time to time Council may fall out of policy due to

timing issues. The Treasury Policy allows for officers to take the necessary

steps to move Council’s funding profile back within policy in the event

that a timing issue causes a policy breach.

4.2 Council’s

current total external debt is $237.7m as at 30th June 2022 ($205.7m as at 31st

March 2022). Offsetting this are $32m of bank deposits ($16.6m as at 31st March

2022), giving a net external debt position of $205m. This is supported by the

Treasury Position 30th June 2022 Report (Attachment 1).

4.3 Council

has bank deposits totalling $32m which is to fund a significant capital spend

budget.

4.4 Standard

and Poors Global (S&P) Update – S&P conduct an annual ratings

review on Council’s Outlook based on a set of five metrics. These

metrics are, Economy, Financial Management, and Budgetary performance,

Liquidity, and Debt burden.

4.5 An

in-depth financial analysis of S&P’s metrics has been completed by

officers in order to better understand what was required in order to maintain

Council’s rating from the prior year of AA

stable. As a consequence liquidity was identified as an

area that officers could affect by ensuring a higher level of prefunding both

for capital spend and repayment of maturing debt.

4.6 In

tandem with this analysis, officers forecasted cash flows needed in light of

the large capital spend underway in Council. In consultation with Bancorp

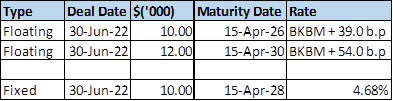

treasury advisors, Council borrowed $32m, with a mix of fixed and floating and

over different maturities. This is itemised in the table below:

4.7 In

light of Council’s current cash flows being able to meet its funding

requirements, it is not expected that Council will engage in any further

borrowing apart from just before year end ensuring Council maintains an ability

to fund budgeted capital spend in the new financial year and meet Standard and

Poors liquidity requirements.

4.8 The

mix of floating and fixed debt borrowed was in order to achieve two outcomes,

firstly in terms of the fixed debt, to ensure that Council remained compliant

with Treasury Policy parameters in terms of cover, secondly, the floating

portion was to enable Council to continue to suppress and lower the cost of

funds wherever possible in light of policy and market considerations.

4.9 In

addition to this, officers engaged in a forward start contract for $21m that

will become “live” the day before the maturing debt for the same

amount comes due in April 2023. Of this $21m, $10m was a fixed interest rate

bond, when it comes into effect in April 2023 it will increase the percentage

of fixed interest rate cover that Council has, pushing Council towards the

mid-point range of policy.

4.10 It

should also be noted on the Treasury position dashboard, Council’s cost

of funds is now at 3.04%, which is a slight rise from the low of 2.76%.

4.11 As

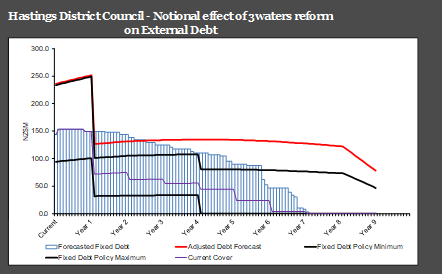

was requested at the previous Risk and Audit Committee meeting, officers have

created a graph that forecasts the future level of debt cover that would be in

place if the water reform was to take place and 50% of Council debt due to

water was to be taken over by the new water entity.

Graph: Forecast

4.12 The

light blue block shows the forecasted cover based on what will be happening

over the next 5 -15 months. The purple line shows the amount of cover that

would be still in place should Council’s debt and some of the hedging

cover be transferred to the new water entity. The two black lines are the

maximum and minimum debt cover parameters as required by the treasury policy.

These can be seen to be shifting down dramatically as the debt falls.

4.13 Officers

are comfortable with the level of cover currently in place in relation to the

level of debt held. There are a number of reasons for being cautious around

committing Council to additional swap cover at this time. However, having

said this in order to maintain compliance with the treasury policy officers

have continued to fix debt prudently.

4.14 In

May 2022 the Reserve bank has again raised the official cash Rate (OCR) to

2%.

5.0 Next steps – Te Anga Whakamua

5.1 Council

officers will continue to work with Bancorp Treasury Services to keep

Council’s financing costs to a minimum, maintaining adequate liquidity,

while maintaining compliance with Council’s Treasury Policy.

Attachments:

|

1⇩

|

Financial Management - Treasury - Investment reporting -

Funding and Interest Rate Risk 30th June 2022

|

FIN-15-01-22-27

|

|

|

Summary of

Considerations - He Whakarāpopoto Whakaarohanga

|

|

Fit

with purpose of Local Government - E noho hāngai pū ai ki te Rangatōpū-ā-Rohe

The Council is required to give effect to the purpose of

local government as set out in section 10 of the Local Government Act 2002.

That purpose is to enable democratic local decision-making and action by (and

on behalf of) communities, and to promote the social, economic,

environmental, and cultural wellbeing of communities in the present and for

the future.

Link to the Council’s

Community Outcomes –

Ngā Hononga ki Ngā Putanga ā-Hapori

This proposal promotes the economic

wellbeing of communities in the present and for the future.

|

|

Māori

Impact Statement -

Te Tauākī Kaupapa Māori

There are no known impacts for Tangata

Whenua.:

|

|

Sustainability

- Te

Toitūtanga

This report promotes sustainable financing costs ensuring

the economic wellbeing of communities in the present and for the future.

|

|

Financial

considerations -

Ngā Whakaarohanga Ahumoni

This report will ensure that

financing costs are kept within Council’s existing budgets.

|

|

Significance

and Engagement -

Te Hiranga me te Tūhonotanga

This decision/report has been assessed under the Council's

Significance and Engagement Policy as being of minor significance.

|

|

Consultation

– internal and/or external - Whakawhiti Whakaaro-ā-roto / ā-waho

There has been no external engagement:

|

|

Risks

The purpose of this report and the Treasury Policies it

refers to, assist officers to manage Council’s treasury risk.

|

REWARD – Te Utu

|

RISK – Te Tūraru

|

|

To assist officers to manage Council’s Treasury

risk; Finances, Reputation.

|

Cashflows and finance costs; Finances, Service Delivery,

Reputation.

|

|

|

Rural

Community Board –

Te Poari Tuawhenua-ā-Hapori

There are no implications for the Rural

Community Board:

|

|

Item 10 Treasury

Activity and Funding Update

|

|

Financial

Management - Treasury - Investment reporting - Funding and Interest Rate Risk

30th June 2022

|

Attachment 1

|

HASTINGS DISTRICT COUNCIL

Risk and Assurance Committee

MEETING

Monday, 18 July 2022

RECOMMENDATION TO EXCLUDE THE PUBLIC

SECTION 48, LOCAL GOVERNMENT OFFICIAL INFORMATION AND

MEETINGS ACT 1987

THAT the public now be excluded from the following part of

the meeting, namely:

14 Contractor

Health & Safety Performance Report

15 Flaxmere

Waterworld Roof Fire Incident - Summary of Findings

16 Regional

Aquatic Facility at the Mitre 10 Sports Park - Potential impacts on Hastings

District Council Aquatics Facilities

The general subject of the matter to be considered while the

public is excluded, the reason for passing this Resolution in relation to the

matter and the specific grounds under Section 48 (1) of the Local Government

Official Information and Meetings Act 1987 for the passing of this Resolution

is as follows:

|

GENERAL SUBJECT OF EACH

MATTER TO BE CONSIDERED

|

REASON FOR PASSING

THIS RESOLUTION IN RELATION TO EACH MATTER, AND

PARTICULAR INTERESTS

PROTECTED

|

GROUND(S) UNDER

SECTION 48(1) FOR THE PASSING OF EACH RESOLUTION

|

|

|

|

|

|

14 Contractor

Health & Safety Performance Report

|

Section 7 (2) (b) (ii)

The withholding of the

information is necessary to protect information where the making available of

the information would be likely to unreasonably prejudice the commercial

position of the person who supplied or who is the subject of the information.

The report contains

sensitive information relating to third parties.

|

Section 48(1)(a)(i)

Where the Local Authority is

named or specified in the First Schedule to this Act under Section 6 or 7

(except Section 7(2)(f)(i)) of this Act.

|

|

15 Flaxmere

Waterworld Roof Fire Incident - Summary of Findings

|

Section 7 (2) (b) (ii)

The withholding of the

information is necessary to protect information where the making available of

the information would be likely to unreasonably prejudice the commercial

position of the person who supplied or who is the subject of the information.

This report contains

sensistive Information relating to third parties.

|

Section 48(1)(a)(i)

Where the Local Authority is

named or specified in the First Schedule to this Act under Section 6 or 7

(except Section 7(2)(f)(i)) of this Act.

|

|

16 Regional

Aquatic Facility at the Mitre 10 Sports Park - Potential impacts on Hastings

District Council Aquatics Facilities

|

Section 7 (2) (h)

The withholding of the

information is necessary to enable the local authority to carry out, without

prejudice or disadvantage, commercial activities.

Protect Commercial

activities.

|

Section 48(1)(a)(i)

Where the Local Authority is

named or specified in the First Schedule to this Act under Section 6 or 7 (except

Section 7(2)(f)(i)) of this Act.

|